2016 Proxy Statement

Notice of Annual Meeting of Stockholders

Wednesday, May 4, 2016

1:30 p.m., Pacific time

Pier 1, Bay 1

San Francisco, California

The date of this proxy statement is March 23, 2016.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934 (Amendment No.)

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |||

| x | Definitive Proxy Statement | |||

| ¨ | Definitive Additional Materials | |||

| ¨ | Soliciting Material Pursuant to Rule 14a-12 | |||

Prologis, Inc. | ||||

| (Name of Registrant as Specified In Its Charter) | ||||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

2016 Proxy Statement

Notice of Annual Meeting of Stockholders

Wednesday, May 4, 2016

1:30 p.m., Pacific time

Pier 1, Bay 1

San Francisco, California

The date of this proxy statement is March 23, 2016.

|

2016 Proxy Statement

|

Pier 1, Bay 1

San Francisco, California 94111

March 23, 2016

Dear Stockholder,

You are invited to attend our Annual Meeting of Stockholders on May 4, 2016, at our corporate headquarters in San Francisco, California. This proxy statement contains information about our company and our 2016 annual meeting proposals and process. Your vote is important to us, and we ask that you vote in accordance with our board’s recommendations.

Over the past year, we have made tremendous progress with our strategic priorities. We saw 19 percent growth year-over-year in core funds from operations per diluted share, and ended 2015 with a record-breaking occupancy level of 96.9 percent. In addition, we increased rents by an average of 13 percent.

I am proud of what our experienced and dedicated teams across the globe have accomplished and look forward to the year ahead. Thank you for your continued support and interest.

Sincerely,

HAMID R. MOGHADAM

Chairman and Chief Executive Officer

|

||||

|

2016 Proxy Statement

|

NOTICE OF 2016 ANNUAL MEETING OF STOCKHOLDERS

March 23, 2016

To our Stockholders:

I invite you to attend the 2016 annual meeting of stockholders of Prologis, Inc.:

1:30 p.m., May 4, 2016

Prologis Corporate Headquarters

Pier 1, Bay 1

San Francisco, California 94111

Items of business. The following items of business will be conducted at our 2016 annual meeting of stockholders:

| 1. | To elect ten directors to our board of directors to serve until the next annual meeting of stockholders and until their successors are duly elected and qualified; |

| 2. | Advisory vote to approve the company’s executive compensation for 2015; |

| 3. | To ratify the appointment of KPMG LLP as our independent registered public accounting firm for the year 2016; and |

| 4. | To consider any other matters that may properly come before the meeting and at any adjournments or postponements of the meeting. |

Record Date. If you are a holder of shares of our common stock at the close of business on March 9, 2016, you are entitled to receive this notice and to vote at the annual meeting and any adjournment(s) or postponement(s) of the annual meeting.

How to Vote. You can vote your shares by proxy through the Internet, by telephone, or by mail using the instructions on the proxy card. Any proxy may be revoked in the manner described in the accompanying proxy statement at any time prior to its exercise at the annual meeting.

Meeting Attendance. If you plan to attend the meeting in person, you must bring proof of current ownership of our common stock to be admitted to and to attend the 2016 annual meeting.

Proxy Materials. On or about March 24, 2016, we intend to distribute to our stockholders:

| (i) | either in printed form by mail or electronically by e-mail, a Notice of Annual Meeting and Internet Availability of Proxy Materials containing instructions on: (a) how to electronically access our 2016 Proxy Statement and 2015 Annual Report to Stockholders, which includes our 2015 Annual Report on Form 10-K; (b) how to vote; and (c) how to request printed proxy materials (if desired) and |

| (ii) | if requested or required, printed proxy materials, which will include our 2016 Proxy Statement, our 2015 Annual Report on Form 10-K, and a proxy card. |

Proxy materials, including the 2016 Proxy Statement and the 2015 Annual Report to Stockholders, are available at www.proxyvote.com.

On behalf of the Board of Directors,

EDWARD S. NEKRITZ

Chief Legal Officer, General Counsel, and Secretary

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting of Stockholders to be held on May 4, 2016. This proxy statement and accompanying form of proxy are first being made available to you on or about March 23, 2016.

|

|

||||

|

2016 Proxy Statement

|

PROXY STATEMENT: TABLE OF CONTENTS

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 4 | ||||

| 5 | ||||

| Board of Directors, Board Committees and Corporate Governance |

6 | |||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 13 | ||||

| 13 | ||||

| 14 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 22 | ||||

| 26 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 44 | ||||

| 45 | ||||

| 49 | ||||

| Outstanding Equity Awards at Fiscal Year-End (December 31, 2015) |

54 | |||

| 56 | ||||

| 58 | ||||

| 61 | ||||

| Advisory Vote to Approve the Company’s Executive Compensation for 2015 (Proposal 2) |

65 | |||

| 65 | ||||

| 66 | ||||

| 68 | ||||

| Information Relating to Our Stockholders, Directors and Executive Officers: Security Ownership |

70 | |||

| 73 | ||||

| 74 | ||||

| 74 | ||||

| 74 | ||||

| Ratification of the Appointment of Independent Registered Public Accounting Firm (Proposal 3) |

75 | |||

| 76 | ||||

| 76 | ||||

| Appendix A: Definitions and Reconciliations of GAAP and Non-GAAP Financial Measures |

A-1 | |||

|

|

i

| |||

|

2016 Proxy Statement

|

Our business is unique to our industry and presents a key strategic advantage. Our global operations span 20 countries on four continents, and we have a $23.1 billion strategic capital business and a development platform with $3.8 billion of construction in progress. These highly integrated components of our business give us the ability to provide our customers with modern, high-quality logistics facilities in the most vibrant centers of trade around the world.

Our global operations and our strategic capital and development businesses function in tandem to provide unparalleled customer service. We are a global company with a strong local presence and specialized teams on the ground in all of the markets in which we do business. Our exemplary customer service differentiates us from our competitors. Our commitment to excellence in customer service is a strategic advantage. We are global because our customers are global. To operate on a global level, we need a strategic capital business that gives us access to third party capital in global regions, which allows us to grow and enhance our returns while mitigating currency risk. Our development business provides the modern logistics space that our customers need in strategic global locations.

Prologis Business Model(1)

| OPERATIONS

Generate annual NOI by maintaining high occupancy rates and increasing rents

|

STRATEGIC CAPITAL

Access third-party capital to grow our business and earn recurring fees and promotes

|

DEVELOPMENT

Create value from development starts annually

|

||||||||||||||

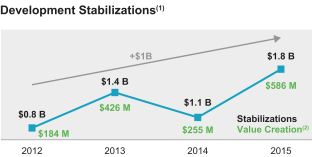

| We have an irreplaceable portfolio of high-quality logistics facilities that serves premier brands across the globe. In 2015, we: | Durable fee stream with more than 90% from perpetual or long-life co-investment ventures.(2) In 2015, we:

|

Development contributes to significant earnings growth as projects lease up and generate NOI. In 2015, we:

|

||||||||||||||

| u Delivered $2.9 billion of annualized net operating income (“NOI”) reflecting a year-over-year increase of 15%

u Ended the fourth quarter with record occupancy of 96.9%

|

u Grew our third-party assets under management by 19% to $23.1 billion(3)

u Increased our fee and promote revenue from our eleven co-investment ventures by 16% to approximately $150 million

|

u Started $2.2 billion of development projects with an estimated value creation of $466.3 million

u Stabilized a total estimated investment of $1.8 billion of development projects with an estimated gross margin(4) of 31.8%, creating $586 million in value

|

||||||||||||||

| (1) | Information in this table relates to our owned and managed portfolio of real estate. |

| (2) | Strategic capital ventures (also referred to as co-investment ventures) are real estate ventures in which we co-invest with third party partners. We manage nine private funds and two non-U.S. publicly traded vehicles, of which we own 15%-66%. |

| (3) | Includes fair market value of strategic capital ventures and estimated investment capacity. |

| (4) | Margins on completed developments shows generally how much value is created by the development of properties (net of expenses) in relation to estimated costs to buy land and develop and lease the properties. Stabilized developments are generally properties that are completed or substantially leased. Please see Appendix A for further detail. |

|

|

1

| |||

|

2016 Proxy Statement

|

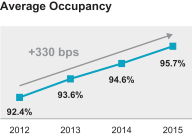

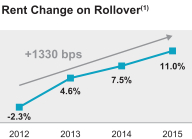

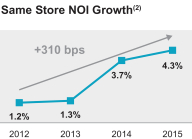

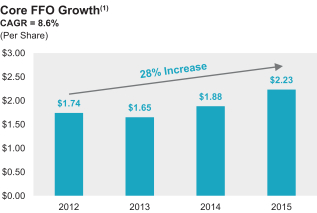

Our business plan is working. Some highlights of our strong operational performance and dividend growth are shown in the graphs below.

|

|

|

| (1) | Rent Change on Rollover is generally the change in rent upon lease renewal. |

| (2) | Same store NOI is a non-GAAP financial measure based on a population of properties consistent from period to period, thereby eliminating the effects of changes in the composition of the portfolio. Same store NOI is defined in Appendix A. |

|

|

| (1) | Core Funds from Operation (“Core FFO”) is a non-GAAP financial measure. Core FFO is defined in Appendix A. A compound annual growth rate, or CAGR, is a measure of the annual growth rate of an investment over a specified period of time. |

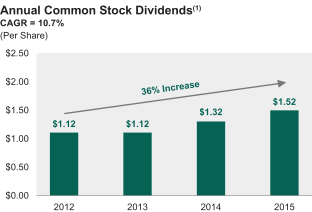

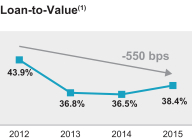

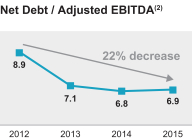

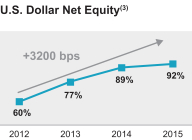

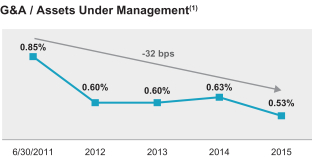

We have delivered long-term growth both on a relative and absolute basis. Our weighted annualized FFO and dividend growth from 2012 to 2015 was 2.1 percentage points and 5.2 percentage points, respectively, higher than that of the U.S. public industrial real estate investment trust (“REIT”) index we use in determining our long-term annual equity awards (East Group Properties, First Industrial, DCT Industrial and Duke Realty). Our Core FFO has grown by 28% and our common stock dividends by 36% since 2012, while we were substantially deleveraging our balance sheet. For further detail, please see “Compensation Discussion and Analysis—Prologis Business Model and Strategic Priorities.”

Our compensation program supports our business model and provides incentives to achieve strong TSR performance. Our annual bonus program rewards successful execution of our strategic priorities. Long-term incentive (“LTI”) equity awards represent a significant component of annual compensation and are completely formulaic based on relative 3-year TSR. Our outperformance compensation plans complete the total pay opportunity for our NEOs but only when exceptional levels of performance are reached.

Our compensation program is working. Compensation is heavily aligned with relative TSR performance. Our operational performance in 2015 was strong, so our bonuses (measured by operational metrics) were above target. However, our 3-year TSR underperformed, so our NEOs received only 50% of target value for their annual LTI equity awards in accordance with the established formula. Also, there was no payout under our outperformance compensation plans in 2015. Our core compensation program (annual base salary, annual bonus and annual long-term incentives) is heavily weighted to align with relative TSR performance, which resulted in a decrease in overall compensation from 2014 despite our strong operational performance.

|

|

2

| |||

|

2016 Proxy Statement

|

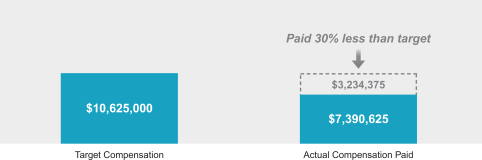

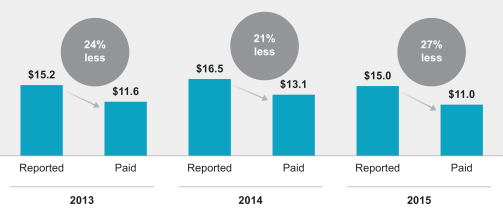

CEO target core compensation vs. core compensation paid for 2015 performance year

CEO core compensation was 30% less than target. As our core compensation program is heavily weighted to align with relative TSR performance, total core compensation paid to our chief executive officer (“CEO”) for the 2015 performance year was 30% less than target.

2015 CEO Target Total Core Compensation vs. 2015 Actual Core Compensation Paid*

| * | Base salary is prorated reflecting salary increases effective June 2015. Actual Compensation Paid includes annual base salary, annual bonus, and annual LTI equity awards for the 2015 performance year and does not include “Other Compensation,” bonus exchange premium amounts, and POP participation point amounts (not yet earned) from the Summary Compensation Table. No awards were paid under our outperformance compensation plans in 2015. |

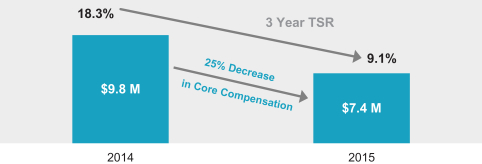

CEO core compensation alignment with TSR

CEO core compensation correlates with relative 3-year TSR. The following graph illustrates the directional relationship between CEO core compensation and company TSR. As a result of lower relative annualized 3-year TSR, our CEO’s core compensation decreased by 25% from the 2014 performance year to the 2015 performance year.

Correlation of CEO Core Compensation and 3-year TSR

For further detail, please see “Compensation Discussion and Analysis—2015 Compensation Highlights.”

|

|

3

| |||

|

2016 Proxy Statement

|

2015 CORPORATE RESPONSIBILITY AND GOVERNANCE HIGHLIGHTS

We continue to take a leadership role in corporate responsibility and governance. We have been named the top REIT in corporate governance by Green Street Advisors for thirteen consecutive years and one of the Global 100 Most Sustainable Corporations in the World by Corporate Knights for eight consecutive years. We were also awarded GRESB’s green star, their highest designation, for outstanding performance in environmental stewardship, social responsibility, and governance.

The following are some key highlights of our corporate responsibility and governance programs:

| Director

|

u 90% of our Board of Directors (“Board”) is independent: All directors, other than our chairman, are independent

u No related-party transactions

| |

| Director

|

u Annual Board evaluation process involving Board, Board committee and individual director assessments: Administered by the chair of our Board Governance and Nomination Committee (the “Governance Committee”) and our lead independent director, with a third party evaluation every other year

u Age/tenure policy: 72 years maximum age limit. Impact of tenure on director independence is evaluated through our extensive annual Board evaluation process

u Directors have diverse skills and broad relevant experience

| |

| Board

|

u Lead independent director role with significant authority and responsibilities

u Chairman and CEO policy gives Board flexibility to determine best candidate for position

| |

| Strong Stockholder Rights |

u Irrevocably opted out of Maryland staggered board provisions: All directors elected annually

u Majority vote is the standard in uncontested director elections

u No stockholder rights plan (“Poison Pill”)

| |

| Corporate responsibility and sustainability |

u Listed in CR Magazine’s Top 10 Industry Sector Best Corporate Citizens for the Financial/Insurance/Real Estate sector

u Received sustainable building certifications (including LEED, BREEAM, CASBEE, DGNB and HQE certifications) for buildings totalling 67 million square feet across 171 projects in 14 countries

u Over 141 megawatts in solar energy capacity over global portfolio

u Released corporate responsibility report using GRI G4-CRESS framework

u Donated $1.5 million to non-profit organizations and interim use of approximately 900,000 square feet of distribution space and sponsored over 9,000 hours of employee volunteer time to various organizations

| |

Stockholder Outreach

During 2015, we conducted significant stockholder outreach to the owners of over 65% of our common stock. During this outreach, our lead independent director and the Chair of the Compensation Committee (the “Compensation Committee”) of the Board met with our stockholders to discuss our unique business plan and our compensation and governance programs.

Our stockholders appreciated hearing about our business and how our compensation program supports our business plan. They also appreciated the changes we made to our annual LTI equity awards to make the process 100% formulaic and transparent.

Our stockholders suggested that we include discussions in CD&A regarding our business, how our compensation program is working and how our compensation correlates with our performance. They also suggested that we make CD&A more reader-friendly. As a result, we have enhanced disclosure in CD&A in response to these suggestions.

|

|

4

| |||

|

2016 Proxy Statement

|

PROPOSALS SUBMITTED TO VOTE AT THE 2016 ANNUAL MEETING

We are asking our stockholders of record on March 9, 2016 to vote on the following matters at our 2016 annual meeting of stockholders to be held on May 4, 2016. Please see the section entitled “Additional Information” for details on how to vote.

|

Proposal

|

Board

| |

| Proposal 1: Election of Directors

u At the annual meeting you will be asked to elect to the board the ten persons nominated by the Board. The directors will be elected to one-year terms and will hold office until the 2017 annual meeting and until their successors are duly elected and qualified.

u Vote Required: You may vote for, vote against, or abstain from voting for any of the director nominees. Assuming a quorum is present, to elect a particular director nominee, the number of votes cast “For” a director nominee must exceed the number of such votes cast “Against” the director nominee. Abstentions and broker non-votes, if any, will have no effect on the outcome of the election. A more detailed description of these majority voting procedures is provided below under “Majority Voting.”

|

For | |

| Proposal 2: Advisory Vote to Approve the Company’s Executive Compensation for 2015

u At the annual meeting you will be asked to approve a resolution on the company’s executive compensation for 2015 as reported in this proxy statement.

u Vote Required: You may vote for, vote against, or abstain from voting to approve the resolution on the company’s executive compensation for 2015. Assuming a quorum is present, to be approved by the stockholders, the proposal must receive the affirmative vote of a majority of the shares of common stock present in person or by proxy at the annual meeting. Abstentions and broker non-votes, if any, are considered shares present in person or by proxy and thus will have the same effect as votes cast “Against” the proposal.

|

For | |

| Proposal 3: Ratification of the Appointment of Independent Registered Public Accounting Firm

u At the annual meeting you will be asked to ratify the appointment of KPMG LLP by the Audit Committee (the “Audit Committee”) of the Board as the company’s independent registered public accounting firm for the year 2016.

u Vote Required: You may vote for, vote against, or abstain from voting on ratifying the appointment of KPMG LLP as our independent registered public accounting firm for the year 2016. Assuming a quorum is present, to be approved by the stockholders, the proposal must receive the affirmative vote of a majority of the shares of common stock present in person or by proxy at the annual meeting. Abstentions and broker non-votes, if any, are considered shares present in person or by proxy and thus will have the same effect as votes cast “Against” the proposal.

|

For | |

Abstentions and broker non-votes are counted for purposes of determining whether a quorum is reached.

References in this proxy statement to “we,” “us,” “our,” the “company,” and “Prologis” refer to Prologis, Inc. and its subsidiaries, unless the context otherwise requires.

This summary highlights information contained in this proxy statement. This summary does not contain all the information you should consider and you should read the entire proxy statement before voting. For more complete information regarding our 2015 performance, please review our Annual Report on Form 10-K for the year ended December 31, 2015. All company operational information in this proxy statement is as of December 31, 2015, unless otherwise noted. See Appendix A for definitions and discussion of non-GAAP measures and reconciliations to GAAP measures and for additional detail regarding definitions of terms as generally explained in the proxy statement.

|

|

5

| |||

|

2016 Proxy Statement

|

BOARD OF DIRECTORS, BOARD COMMITTEES AND CORPORATE GOVERNANCE

ELECTION OF DIRECTORS (PROPOSAL 1)

The Board currently consists of ten directors, all of whom are standing to be elected to the Board at the 2016 annual meeting of stockholders to hold office until the 2017 annual meeting and until their successors are duly elected and qualified.

The Board has affirmatively determined that all of the director nominees, other than Hamid Moghadam, are independent directors in accordance with New York Stock Exchange (“NYSE”) rules, our governance guidelines, and our bylaws.

Our bylaws provide for a majority voting standard for the election of directors. See “Additional Information—Majority Voting” below for further detail.

We do not know of any reason why any nominee would be unable or unwilling to serve as a director, if elected. However, if a nominee becomes unable to serve or will not serve, proxies may be voted for the election of such other person nominated by the Board as a substitute or the Board may reduce the number of directors. Each of the director nominees has consented to be named in this proxy statement and to serve as a director if elected. Information about each director nominee’s share ownership is presented below under “Security Ownership.” Certain of the director nominees previously served on the board of ProLogis (the “Trust”). In June 2011, AMB Property Corporation (“AMB”) and the Trust completed a merger transaction (the “Merger”) and, effective with the Merger, our name was changed from AMB to Prologis, Inc.

The shares represented by the proxies received will be voted for the election of each of the ten nominees named below, unless you indicate in the proxy that your vote should be cast against any or all of the director nominees or that you abstain from voting. Each nominee elected as a director will continue in office until his or her successor has been duly elected and qualified, or until the earliest of his or her resignation, retirement, or death. The ten nominees for election to the Board at the 2016 annual meeting, all proposed by the Board, are listed below with brief biographies.

The Board unanimously recommends that the stockholders vote FOR the election of each nominee.

Director Qualifications, Skills, and Experience

Each of the director nominees was chosen to serve on the Board based on his or her qualifications, skills, and experience, as discussed in their biographies, and how those characteristics supplement the resources and talent on the Board and serve the current needs of the Board and the company. For information regarding our business, its strategy and goals, please see “Compensation Discussion and Analysis.”

In making its nominations, the Governance Committee also assessed each director nominee along a number of key characteristics, including integrity, experience, accountability, judgment, courage to voice opinions, supportiveness in working with others and willingness to commit the time needed to satisfy the requirements of Board and committee membership. While the Governance Committee does not have a formal policy regarding diversity, the committee considers diversity in gender, ethnic background, geographic origin, and professional experience in assessing director nominees.

|

|

6

| |||

|

2016 Proxy Statement

|

Board Qualifications

In addition to other attributes, the slate of director nominees possess qualifications in the following areas:

| H.

|

G.

|

C.

|

L.

|

J.M.

|

I.

|

D.

|

J.

|

C.

|

W.

| |||||||||||

| Real estate/logistics (development, investment and/or management) | ü | ü | ü | ü | ü | ü | ||||||||||||||

| CEO/executive management |

ü | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||||

| Strategic planning |

ü | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||||

| Finance/accounting |

ü | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||||

| Global operations |

ü | ü | ü | ü | ü | ü | ||||||||||||||

| Risk management |

ü | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||||

Board Evaluations and Process for Selecting Directors

In the annual Board evaluation process, the Governance Committee evaluates current members of the Board in light of needs of the Board and the company. In addition, during the course of the year, the committee discusses Board succession and reviews potential candidates. The committee may also retain a third party to assist in identifying potential nominees, although it has not done so in the past.

Our annual Board evaluation process involves assessments at the Board, Board committee and individual director levels. These annual evaluations are conducted by the chair of the Governance Committee and our lead independent director and, every other year, by an independent third party. Through this process, the Board determines the best candidates for the chairs of the Board and Board committees and Board and committee membership based on current company and Board needs.

Our governance guidelines provide that directors will not be nominated or appointed to the Board if they are, or would be, 72 years or older at the time of the election or appointment. Term limits on directors’ service have not been instituted.

|

|

7

| |||

|

2016 Proxy Statement

|

|

Hamid R. Moghadam

Chairman of the Board since January 2000; Director since November 1997

u Board Committees: Executive

u Other public directorships: None

Mr. Moghadam, 59, has been our chief executive officer since the end of December 2012 and was our co-chief executive officer from June 2011 to December 2012. He is the co-founder of AMB Property Corporation and was AMB’s chief executive officer from November 1997 (from the time of AMB’s initial public offering) to June 2011 when AMB merged with the Trust.

Other relevant qualifications. Mr. Moghadam is a Trustee of Stanford University and served on the Executive Committee of the Board of Directors of the Urban Land Institute. Mr. Moghadam holds Bachelor’s and Master’s degrees in engineering from the Massachusetts Institute of Technology and a Master of Business Administration from the Graduate School of Business at Stanford University.

| |

|

Irving F. Lyons III

Lead Independent Director since June 2011 (prior to the Merger served as a trustee of the Trust from September 2009 to June 2011 and from March 1996 to May 2006)

u Board Committees: Executive

u Other public directorships: Equinix, Inc. and Essex Property Trust, Inc.

Mr. Lyons, 66, has been a principal with Lyons Asset Management, a private equity firm, since January 2005. In 2004, Mr. Lyons retired from the Trust where he had served as chief investment officer from 1997 until his retirement. He joined the Trust in 1993 and served as president from 1999 to 2001 and vice chairman from 2001 to 2004. Mr. Lyons is a member of the boards of Equinix, Inc., a global data center operator, and Essex Property Trust, Inc., a real estate investment trust investing in apartment communities. Mr. Lyons previously served as chairman of the board of BRE Properties, Inc.

Other relevant qualifications. Mr. Lyons joined the Trust when King & Lyons, an industrial real estate management and development company, was acquired by the Trust in 1993. Mr. Lyons had been the managing general partner in that firm since its inception in 1979 and was one of its principals at the time of the acquisition. Mr. Lyons holds a Master in Business Administration from Stanford University and a Bachelor of Science in industrial engineering and operations research from the University of California at Berkeley.

|

|

|

8

| |||

|

2016 Proxy Statement

|

|

George L. Fotiades

Director since June 2011 (prior to the Merger served as a trustee of the Trust from December 2001 to June 2011)

u Board Committees: Compensation (Chair)

u Other public directorships: AptarGroup, Inc. and Cantel Medical Corp.

Mr. Fotiades, 62, has been a partner at Diamond Castle Holdings, a private equity investment firm, since April 2007. Mr. Fotiades was chairman of Catalent Pharma Solutions, Inc., a provider of advanced technologies for pharmaceutical, biotechnology, and consumer health companies, from June 2007 to February 2010. Mr. Fotiades is a member of the board of AptarGroup, Inc., a global dispensing systems company, and is vice chairman of the board of Cantel Medical Corp., a provider of infection prevention and control products. He previously served on the board of Alberto-Culver Company, a consumer products company specializing in hair and skin care products.

Other relevant qualifications. Mr. Fotiades was previously the president and chief operating officer of Cardinal Health, Inc. and also served as president and chief executive officer of Cardinal’s Pharmaceutical Technologies and Services segment. Mr. Fotiades also served as president of Warner-Lambert’s consumer healthcare business, as well as in other senior positions at Bristol-Myers Squibb, Wyeth, and Procter & Gamble. Mr. Fotiades holds a Master of Management from The Kellogg School of Management at Northwestern University and a Bachelor of Arts from Amherst College.

| |

|

Christine N. Garvey

Director since June 2011 (prior to the Merger served as a trustee of the Trust from September 2005 to June 2011)

u Board Committees: Audit, Governance

u Other public directorships: HCP, Inc., Toll Brothers, Inc., and MUFG Americas Holding Corporation

Ms. Garvey, 70, retired from Deutsche Bank AG, a global investment bank, in May 2004, where she served as global head of corporate real estate services at Deutsche Bank AG London from May 2001 until her retirement. She was a consultant to Deutsche Bank AG from 2004 to 2006. Ms. Garvey is a member of the boards of HCP, Inc., a real estate investment trust investing in health care real estate, Toll Brothers, Inc., a luxury home builder, and MUFG Americas Holding Corporation, whose principal subsidiary is MUFG Union Bank, N.A. Ms. Garvey was previously a member of the board of MPG Office Trust, Inc., a real estate investment trust investing in office properties.

Other relevant qualifications. Ms. Garvey was previously vice president, worldwide real estate and workplace resources for Cisco Systems, Inc. and also held several positions with Bank of America, including group executive vice president and head of national commercial real estate services. Ms. Garvey was a member of the board of Catellus Development Corporation prior to its merger with the Trust in 2005 and was also on the board of Hilton Hotels Corporation, a global hospitality company. Ms. Garvey holds a Juris Doctor degree from Suffolk University Law School and a Bachelor of Arts, magna cum laude, from Immaculate Heart College in Los Angeles.

|

|

|

9

| |||

|

2016 Proxy Statement

|

|

Lydia H. Kennard

Director since August 2004

u Board Committees: Governance (Chair)

u Other public directorships: Freeport-McMoRan Copper & Gold Inc.

Ms. Kennard, 61, is the founder and chief executive officer of KDG Construction Consulting, a provider of project and construction management services, a principal of Airport Property Ventures, LLC, an aviation focused real estate operating and development company, and a principal with 3801-3825 N. Mission Rd, LA, LLC, a single-purpose real estate entity. Ms. Kennard is a member of the board of Freeport-McMoRan Copper & Gold Inc., a natural resource company. Ms. Kennard was previously a member of the board of URS Corporation, a provider of engineering, construction, and technical services, and Intermec, Inc., an automated identification and data collection company.

Other relevant qualifications. Ms. Kennard served as executive director of Los Angeles World Airports, a system of airports comprising Los Angeles International, Palmdale Regional, and Van Nuys General Aviation Airports from 1999 to 2003 and again from 2005 to 2007. From 1994 to 1999, she served as the system’s deputy executive for design and construction. She has also previously served on the board of Indymac Bancorp, Inc., a thrift/mortgage bank holding company. Ms. Kennard holds a Juris Doctor degree from Harvard University, a Master’s degree in city planning from Massachusetts Institute of Technology, and a Bachelor of Science in urban planning and management from Stanford University.

| |

|

J. Michael Losh

Director since January 2003

u Board Committees: Audit (Chair)

u Other public directorships: AON Corporation, Masco Corporation, and H.B. Fuller Company

Mr. Losh, 69, was interim chief financial officer of Cardinal Health, Inc., a health care products and services company, from July 2004 to May 2005 and served on its board from 1996 until September 2009. Mr. Losh is a member of the boards of AON Corporation, a global provider of risk management services, insurance and re-insurance, and human resource consulting and outsourcing, Masco Corporation, a home improvement and building products company, and H.B. Fuller Company, a global formulator, manufacturer, and marketer of chemical products. Mr. Losh previously served on the boards of TRW Automotive Holdings Inc., a global automotive supply company and CareFusion Corporation, a global medical technology company.

Other relevant qualifications. Mr. Losh spent 36 years with General Motors Corporation, an automobile manufacturer, most recently as executive vice president and chief financial officer from July 1994 to August 2000 and as chairman of GMAC, General Motors’ financial services group, from July 1994 to April 1999. Mr. Losh holds a Master in Business Administration from Harvard University and a Bachelor of Science in mechanical engineering from Kettering University.

|

|

|

10

| |||

|

2016 Proxy Statement

|

|

David P. O’Connor

Director since January 2015

u Board Committees: Compensation

u Other public directorships: Regency Centers, Inc. and Paramount Group, Inc.

Mr. O’Connor, 51, is a private investor and managing partner of High Rise Capital Partners, LLC, a real estate investment firm. He was the co-founder and senior managing partner of High Rise Capital Management LP, a real estate securities hedge fund manager that operated from 2001 to 2011. Mr. O’Connor is a member of the boards of Regency Centers, Inc., a publicly traded real estate investment trust specializing in shopping centers, and Paramount Group, Inc., a publicly traded real estate investment and management company specializing in office buildings. He previously served on the board of Songbird Estates plc, the former majority owner of Canary Wharf in London, UK.

Other relevant qualifications. Mr. O’Connor was previously a principal, co-portfolio manager, and investment committee member of European Investors, Inc., a large dedicated real estate investment trust investor, from 1994 to 2000. Mr. O’Connor received a Master of Science in real estate from New York University and holds a Bachelor of Science degree from the Carroll School of Management at Boston College.

| |

|

Jeffrey L. Skelton

Director since November 1997

u Board Committees: Governance, Executive (Chair)

u Other public directorships: None

Mr. Skelton, 66, retired in 2009 as president and chief executive officer of Symphony Asset Management, a subsidiary of Nuveen Investments, Inc., an investment management firm. After his retirement in 2009 and until 2013, Mr. Skelton was a co-founder and managing partner of Resultant Capital Partners, an investment management firm.

Other relevant qualifications. Prior to founding Symphony Asset Management in 1994, Mr. Skelton was with Wells Fargo Nikko Investment Advisors from 1984 to 1993, where he served in a variety of capacities, including chief research officer, vice chairman, co-chief investment officer, and chief executive officer of Wells Fargo Nikko Investment Advisors Limited in London. Previously, Mr. Skelton was also an assistant professor of finance at the University of California at Berkeley, Walter A. Haas School of Business. Mr. Skelton holds a Ph.D. in mathematical economics and finance and a Master of Business Administration from the University of Chicago.

|

|

|

11

| |||

|

2016 Proxy Statement

|

|

Carl B. Webb

Director since August 2007

u Board Committees: Audit

u Other public directorships: Hilltop Holdings Inc.

Mr. Webb, 66, is currently the co-managing member of Ford Financial Fund II, L.P. a private equity firm focusing on equity investments in financial services, a position he has held since February 2012. In April 2015, Ford Financial Fund II, L.P. purchased a controlling interest in Mechanics Bank, a California-based banking institution, and Mr. Webb has served as chairman of the Mechanics Bank board since that time. From June 2008 until December 2012, Mr. Webb was a senior partner of Ford Management, L.P., a private equity firm that owned substantially all of Pacific Capital Bancorp. Mr. Webb was the chief executive officer and a board member of Pacific Capital Bancorp and chairman and chief executive officer of Pacific Capital Bank, N.A. from August 2010 until December 2012 when these companies were merged with UnionBanCal Corporation. Mr. Webb has also served as a consultant to Hunter’s Glen/Ford, Ltd., a private investment partnership, since November 2002. Additionally, Mr. Webb is a member of the board of Hilltop Holdings Inc., a publicly traded financial services holding company.

Other relevant qualifications. Mr. Webb previously served on the boards of Plum Creek Timber Company, M & F Worldwide Corp., and Triad Financial SM LLC, where he was co-chairman from July 2007 to October 2009 and served as interim president and chief executive officer from August 2005 to June 2007. Since 1983, Mr. Webb held executive positions at banking institutions, including Golden State Bancorp, Inc. and its subsidiary, California Federal Bank, FSB, First Madison Bank, FSB, First Gibraltar Bank, FSB, and First National Bank at Lubbock. Mr. Webb holds a Bachelor of Business Administration from West Texas A&M University and a graduate banking degree from Southwestern Graduate School of Banking at Southern Methodist University.

| |

|

William D. Zollars

Director since June 2011 (prior to the Merger served as a trustee of the Trust from December 2001 to May 2010)

u Board Committees: Governance, Compensation

u Other public directorships: Cerner Corporation and CIGNA Corporation

Mr. Zollars, 68, retired from YRC Worldwide, Inc., a global transportation service provider, in July 2011 where he served as chairman, president, and chief executive officer from 1999 until his retirement. He was president of Yellow Transportation, Inc. from 1996 to 1999. Mr. Zollars is a member of the boards of Cerner Corporation, a supplier of healthcare information technology solutions, healthcare devices, and related services, and CIGNA Corporation, a global health service organization.

Other relevant qualifications. Mr. Zollars was previously a senior vice president of Ryder Integrated Logistics, a division of Ryder System, Inc. and he spent 24 years in various executive positions, including eight years in international locations, at Eastman Kodak. Mr. Zollars holds a Bachelor of Arts in economics from the University of Minnesota.

|

|

|

12

| |||

|

2016 Proxy Statement

|

We require that a majority of the Board be independent in accordance with NYSE rules. To determine whether a director is independent, the Board must affirmatively determine that there is no direct or indirect material relationship between the company and the director.

90% of the Board is independent. The Board has determined that all of our directors, other than our chairman, Mr. Moghadam, are independent. The Board reached this determination after considering all relevant facts and circumstances, reviewing director questionnaires and considering transactions and relationships, if any, between us, our affiliates, our executive officers and their affiliates, and each of the directors, members of each director’s immediate family, and each director’s affiliates.

Audit, Compensation, and Governance Committees are 100% independent. The Board has also determined that all members of the Audit, Compensation, and Governance Committees of the Board are independent in accordance with NYSE and Securities and Exchange Commission (“SEC”) rules.

Our governance guidelines do not specify a leadership structure for the Board, allowing the Board the flexibility to choose the best option for the company as circumstances warrant. The Board believes that strong independent leadership ensures effective oversight over the company. Such independent oversight is maintained through:

| u | our lead independent director; |

| u | our independent directors (90% are independent under NYSE rules); |

| u | the Audit, Compensation, and Governance Committees, which are all comprised entirely of independent directors; |

| u | annual review of the Board leadership structure and effectiveness of oversight through the Board evaluation process; and |

| u | strong adherence to our governance guidelines. |

All of our independent directors have the ability to provide input for meeting agendas and are encouraged to raise topics for discussion by the Board. In addition, the Board and each Board committee has complete and open access to any member of management and the authority to retain independent legal, financial and other advisors as they deem appropriate without consulting or obtaining the approval of any member of management. The Board also holds regularly scheduled executive sessions of only independent directors in order to promote free and open discussion among the independent directors.

Chairman and CEO assessment

Our chairman and CEO and our lead independent director act together in a system of checks and balances, providing both strong oversight and operational insight. Our CEO, Mr. Moghadam, serves as chairman of the Board. The lead independent director role is focused on ensuring independent oversight of the company. Mr. Moghadam’s roles as both CEO and chairman enable him to act as a bridge between management and the Board, ensuring that the Board understands the business when making its decisions.

Mr. Moghadam has the breadth of experience to execute our unique business plan and provide special insight to the Board. Very few have experience running a public company with extensive global operations and substantial strategic capital and development businesses. Mr. Moghadam co-founded the company and has served on the Board since the company’s initial public offering in November 1997. As one of our founders, Mr. Moghadam has extensive knowledge and expertise in the real estate and REIT industries, as well as history and knowledge of our company.

|

|

13

| |||

|

2016 Proxy Statement

|

Considering all of these factors, the Board believes that a structure that combines the roles of CEO and chairman, along with an independent lead director, independent chairs for each of the Board committees, and independent non-employee directors, provides the best leadership for the company at this time and places the company in a competitive position to provide long-term value to our stockholders.

Lead independent director

If the offices of chairman and CEO are held by the same person, the independent members of the Board will annually elect an independent director to serve in a lead capacity. The lead independent director is generally expected to serve for more than one year. Mr. Lyons has been selected as the lead independent director by our Governance Committee and the independent members of our Board and has served in that capacity for 5 years.

The lead independent director coordinates the activities of the other independent directors, and performs such other duties and responsibilities as the Board may determine.

The specific responsibilities of the lead independent director are currently as follows:

|

Executive Sessions/Committee

|

u Presides at all meetings of the Board at which the chairman is not present, including executive sessions of the independent directors (generally held at every regular board meeting)

u Attends meetings of the various Board committees regularly

| |

|

Meetings of Independent Directors

|

u Has the authority to call meetings of the independent directors

| |

| Board Evaluations | u Oversees, with the chair of the Governance Committee, annual evaluations of the Board, Board committees, and individual directors, including an evaluation of the chairman’s effectiveness as both chairman and CEO

| |

| Liaison with Chairman and CEO

|

u Serves as liaison between the independent directors and the chairman

u Meets regularly between Board meetings with the chairman and CEO

| |

| Board Processes and Information

|

u Ensures the quality, quantity, appropriateness and timeliness of information provided to the Board and provides input to create meeting agendas

u Ensures that feedback is properly communicated to Board and chairman

u Ensures the institution of proper Board processes, including the number, frequency, and scheduling of Board meetings and sufficient time for discussion of all agenda items

| |

| Retention of Outside Advisors and Consultants

|

u Has authority to retain outside advisors and consultants who report directly to the Board

| |

| Communications with

|

u Responds to stockholder inquiries when appropriate, following consultation with the chairman and CEO

u Communicates with stockholders when appropriate, following consultation with the chairman and CEO

| |

Pursuant to the Maryland General Corporation Law and our bylaws, our business, property, and affairs are managed under the direction of the Board. Members of the Board are kept informed of our business through our executive management team.

The four standing committees of the Board are: Audit, Governance, Compensation, and Executive Committee (the “Executive Committee”). The Board has determined that each member of the Audit, Governance, and Compensation Committees is an independent director in accordance with NYSE rules.

Membership information for our Board committees is presented below. The current membership has been in effect since April 2015, at which time Mr. O’Connor replaced Mr. Webb on the Compensation Committee.

|

|

14

| |||

|

2016 Proxy Statement

|

Each committee has a charter which generally states the purpose of the committee and outlines the committee’s structure and responsibilities. The committees, other than the Executive Committee, must review the adequacy of their charter on an annual basis.

|

Board Committees

|

| Audit Committee

Members: J. Michael Losh* (Chair), Christine Garvey*, and Carl Webb*

Number of Meetings in 2015: 8

u Oversees the financial accounting and reporting processes of the company

u Responsible for the appointment, compensation, and oversight of our public accountants

u Monitors: (i) the integrity of our financial statements; (ii) our compliance with legal and regulatory requirements; (iii) our public accountant’s qualifications and independence; and (iv) the performance of our internal audit function and public accountants

u Oversees financial and cybersecurity risks relating to the company

* Designated by the Board as an “audit committee financial expert” in accordance with SEC regulations. Meets the independence, experience, and financial literacy requirements of the NYSE and Section 10A of the Securities Exchange Act of 1934, as amended.

|

|

Compensation Committee

Members: George Fotiades (Chair), David O’Connor, and William Zollars

Number of Meetings in 2015: 4

u Discharges the Board’s responsibilities relating to compensation of directors and executives and to produce an annual report on executive compensation for inclusion in the proxy statement

u Approves and evaluates our director and officer compensation plans, policies, and programs

u Reviews and recommends to the Board corporate goals and objectives relative to the compensation of our CEO

u Evaluates our CEO’s performance in light of corporate goals and objectives, and setting the CEO’s compensation level based on this evaluation, including incentive and equity-based compensation plans

u Sets the amount and form of compensation for the executive officers who report to the CEO

u Makes recommendations to the Board (including recommendations for non-employee directors) on general compensation practices, including incentive and equity-based compensation plans, and adopting, administering, and making awards under annual and long-term incentive compensation and equity-based compensation plans, including any amendments to the awards under any such plans, and reviewing and monitoring awards under such plans

u Reviews and approves any new employment agreements, change in control agreements, and severance or similar termination payments proposed to be made to the CEO or any other executive officer of the company

u Confirms that relevant reports are made to the Board or in periodic filings as required by governing rules and regulations of the SEC and NYSE

u Reviews and discusses with management CD&A and determines whether to recommend its inclusion in the proxy statement to the Board

u Participates in succession planning for key executives

u Focuses on risks relating to remuneration of our officers and employees and administers our equity compensation plans, our nonqualified deferred compensation arrangements, and our 401(k) plan

|

|

|

15

| |||

|

2016 Proxy Statement

|

|

Board Governance and Nomination Committee

Members: Lydia Kennard (Chair), Christine Garvey, Jeffrey Skelton, and William Zollars

Number of Meetings in 2015: 2

u Reviews and makes recommendations to the Board on Board organization and succession matters

u Assists the full Board in evaluating the effectiveness of the Board and its committees

u Reviews and makes recommendations for committee appointments to the Board

u Identifies individuals qualified to become Board members consistent with any criteria approved by the Board and proposes to the Board a slate of nominees for election to the Board

u Assesses and makes recommendations to the Board on corporate governance matters

u Develops and recommends to the Board a set of corporate governance principles applicable to the company

u Assists the Board in reviewing and approving the company’s activities, goals, and policies concerning environmental stewardship and social responsibility matters

u Reviews the adequacy of our governance guidelines on an annual basis and focuses on reputational and corporate governance risks

|

|

Executive Committee

Members: Jeffrey Skelton (Chair), Irving Lyons III, and Hamid Moghadam

Number of Meetings in 2015: 0

u Acts only if action by the Board is required, the Board is unavailable, and the matter to be acted on is time-sensitive

u Has all of the powers and authority of the Board, subject to such limitations as the Board, the committee’s charter, and/or applicable law, rules, and regulations may from time to time impose

|

Other Governance Matters

Board’s role in risk oversight

The Board has the primary responsibility for overseeing risk management of the company, and our management team provides the Board with a regular report highlighting their risk assessments and recommendations. Oversight for certain specific risks falls under the responsibilities of our Board committees.

| u | The Audit Committee focuses on financial and cybersecurity risks relating to the company. |

| u | The Compensation Committee focuses on risks relating to remuneration of our officers and employees. |

| u | The Governance Committee focuses on reputational and corporate governance risks relating to the company. |

These committees regularly advise the full Board of their risk oversight activities. In addition, the Audit Committee and our full Board regularly hold discussions with our risk management group and other members of management regarding the risks that may affect the company, including those risks identified by an internal risk measurement tool that management uses to monitor risks associated with our real estate assets, such as levels of occupancy, non-income producing assets, leverage levels, foreign currency exposure, and other factors.

CEO and management succession planning

The Board is responsible for ensuring that we have a high-performing management team in place. The Board, with the assistance of the Compensation Committee, regularly conducts a detailed review of management development and succession planning activities to ensure that top management positions, including the CEO position, can be filled without undue interruption.

|

|

16

| |||

|

2016 Proxy Statement

|

Communications with directors

We appreciate your input. You can communicate with any of the directors, individually or as a group, by writing to them in care of Edward S. Nekritz, Secretary, Prologis, Inc., Pier 1, Bay 1, San Francisco, California 94111. Such communications will be reviewed and forwarded to the appropriate director. Each communication intended for the Board and received by the secretary that is related to the operation of the company and is not otherwise commercial in nature will be forwarded to the specified party following its clearance through normal security procedures. The directors will be advised of any communications that were excluded through normal security procedures and they will be made available to any director who wishes to review them.

Director attendance

The Board held seven meetings in 2015, including telephonic meetings, and all of the directors attended 75% or more of the aggregate number of Board and applicable committee meetings on which he or she served during 2015 (held during the periods they served). Each director standing for election in 2016 is expected to attend the annual meeting of stockholders, either in person or telephonically, absent cause, and eight directors attended the annual meeting last year, in person or telephonically.

Director compensation

Please see “Director Compensation Matters” and the table entitled “Directors Compensation for Fiscal Year 2015.”

Stock ownership guidelines and prohibition on hedging/pledging

Our directors must comply with our stock ownership guidelines which require the director to maintain an ownership level in our common stock equal to five times the annual cash retainer ($500,000 as of December 31, 2015). Shares included as owned by directors for purposes of the guidelines include common stock owned, vested or unvested equity awards (restricted stock, restricted stock units, shares, and share units deferred under the terms of the Director Deferred Fee Plan or the applicable non-qualified deferred compensation plan, deferred share units, and dividend equivalent units) and operating partnership or other partnership units exchangeable or redeemable for common stock. Until such time as the guidelines are met, we will require directors to retain and hold 50% of any net shares of our common stock issued to our directors under our equity compensation plans.

Additionally, our insider trading policy prohibits our directors and employees from hedging the economic risk of ownership of our common stock and from pledging shares of our common stock.

All of our directors are currently in compliance with the stock ownership guidelines and the prohibition on hedging and pledging our common stock.

Independent compensation consultant

The Compensation Committee directly engages an outside compensation consulting firm, Frederic W. Cook & Co., Inc. (“FW Cook”) to assist the committee in assessing our compensation programs for our Board, our CEO and other members of executive management. FW Cook, has been engaged by the committee since June 2011 and reports directly to the Compensation Committee. FW Cook receives no compensation from the company other than for its work in advising the Compensation Committee and maintains no other economic relationships with the company. FW Cook interacts directly with members of our management only on matters under the Compensation Committee’s oversight.

FW Cook conducted a comprehensive competitive review of the compensation program for our executive officers and our non-employee directors in 2015, which was used by the Compensation Committee to assist it in making compensation recommendations to the Board. Our CEO makes separate recommendations to the Compensation Committee concerning the form and amount of the compensation of our executive officers (excluding his own compensation). FW Cook has also assisted the Compensation Committee in evaluating the design of certain outperformance compensation plans implemented in 2012.

During its December 2015 meeting, the Compensation Committee considered the independence of FW Cook in light of the rules regarding compensation committee advisor independence mandated under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”). The Compensation Committee reviewed factors, facts, and circumstances

|

|

17

| |||

|

2016 Proxy Statement

|

regarding compensation consultant independence, including a letter from FW Cook addressing FW Cook’s and their consulting team’s independent status with respect to the following factors: (i) other services provided to us by FW Cook; (ii) fees we pay to FW Cook as a percentage of their total revenues; (iii) FW Cook’s policies and procedures that are designed to prevent conflicts of interest; (iv) any business or personal relationship between FW Cook or members of their consulting team that serves the Compensation Committee and a member of the Compensation Committee; (v) any shares of our stock owned by FW Cook or members of their consulting team that serves the Compensation Committee; and (vi) any business or personal relationships between our executive officers and FW Cook or members of their consulting team that serves the Compensation Committee. After discussing these factors, facts, and circumstances, the Compensation Committee affirmed the independent status of FW Cook and concluded that there are no conflicts of interest with respect to FW Cook.

Compensation Committee interlocks and insider participation

No member of the Compensation Committee: (i) was, during the year ended December 31, 2015, or had previously been, an officer or employee of the company or (ii) had any material interest in a transaction with the company or a business relationship with, or any indebtedness to, the company. No interlocking relationships existed during the year ended December 31, 2015, between any member of the Board or the Compensation Committee and an executive officer of the company.

Code of Ethics and Business Conduct and Governance Guidelines

The Board has adopted a code of ethics and business conduct that applies to all employees and directors. The Board has formalized policies, procedures, and standards of corporate governance that are reflected in our Governance Guidelines.

Our Code of Ethics and Business Conduct outlines in great detail the key principles of ethical conduct expected of our employees, officers, and directors, including matters related to conflicts of interest, use of company resources, fair dealing, and financial reporting and disclosure. The code establishes formal procedures for reporting illegal or unethical behavior to the company’s internal ethics committee. These procedures permit employees to report any concerns, including concerns about the company’s accounting, internal accounting controls, or auditing matters, on a confidential or anonymous basis if desired. Employees may contact the ethics committee by e-mail, in writing, by web-based report, or by calling a toll-free telephone number. Any significant concerns are reported to the Audit Committee in accordance with the code.

Simultaneous Board service

Our governance guidelines require that, if a director serves on three or more public company boards simultaneously, including our Board, a determination is made by our Board as to whether such simultaneous service impairs the ability of such member to effectively serve the company. Messrs. Fotiades, Losh, Lyons, O’Connor and Zollars and Ms. Garvey currently serve on at least three public company boards, including our Board. In each case, our Board has determined that such simultaneous board service does not impair the Board member’s ability to be an effective member of our Board. None of our directors currently serve on more than four public company boards (including our Board).

Certain relationships and related party transactions

We do not have any related party transactions to report under relevant SEC rules and regulations. According to our Articles of Incorporation, the Board may authorize any agreement or other transaction with any party even though one or more of our directors or officers may be a party to such an agreement or is an officer, director, stockholder, member, or partner of the other party if: (i) the existence of the relationship is disclosed or known to the Board, and the contract or transaction is authorized, approved, or ratified by the affirmative vote of not less than a majority of the disinterested directors, even if they constitute less than a quorum of the Board; (ii) the existence is disclosed to the stockholders entitled to vote, and the contract or transaction is authorized, approved, or ratified by a majority of the votes cast by the stockholders entitled to vote (excluding shares owned by any interested director or officer or the organization in which such person is a director or has a material financial interest); or (iii) the contract or transaction is fair and reasonable to the company.

We recognize that transactions between us and related parties can present potential or actual conflicts of interest and create the appearance that our decisions are based on considerations other than the company’s best interests and the best interests of our stockholders. Related parties may include our directors, executives, significant stockholders, and immediate family members and affiliates of such persons. Accordingly, several provisions of our code of ethics and business conduct are

|

|

18

| |||

|

2016 Proxy Statement

|

intended to help us avoid the conflicts and other issues that may arise in transactions between us and related parties, prescribing that:

| u | employees will not engage in conduct or activity that may raise questions as to the company’s honesty, impartiality, or reputation or otherwise cause embarrassment to the company; |

| u | employees shall not hold financial interests that conflict with, or leave the appearance of conflicting with, the performance of their assigned duties; |

| u | employees shall act impartially and not give undue preferential treatment to any private organization or individual; and |

| u | employees should avoid actual conflicts or the appearance of conflicts of interest. |

These provisions of our code of ethics and business conduct may be amended, modified, or waived by the Board or the Governance Committee, subject to the disclosure requirements and other provisions of the rules and regulations of the SEC and the NYSE.

No waivers of our code of ethics and business conduct were granted in 2015.

Although we do not have detailed written procedures concerning the waiver of the application of our code of ethics and business conduct or the review and approval of transactions with directors or their affiliates, our directors would consider all relevant facts and circumstances in considering any such waiver or review and approval.

|

|

19

| |||

|

2016 Proxy Statement

|

CERTAIN INFORMATION WITH RESPECT TO OUR EXECUTIVE OFFICERS

Biographical summaries of the experience of our executive officers as of December 31, 2015, other than Mr. Moghadam, are presented below. Information for Mr. Moghadam is included above under “Board of Directors, Board Committees and Corporate Governance—Election of Directors (Proposal 1).”

Thomas S. Olinger: Chief Financial Officer

Mr. Olinger, 49, has been our chief financial officer since May 2012 and was our chief integration officer from June 2011 to May 2012. Mr. Olinger was the chief financial officer of AMB from March 2007 to June 2011. Prior to joining AMB in February 2007, Mr. Olinger was the vice president and corporate controller at Oracle Corporation, an enterprise software company and provider of computer hardware products and services. Prior to his employment with Oracle, Mr. Olinger was an accountant and partner at Arthur Andersen LLP, where he served as the lead partner on our account from 1999 to 2002. Since January 2011, Mr. Olinger has served as a director of American Assets Trust, a real estate investment trust investing in retail, office, and residential properties. Mr. Olinger holds a Bachelor of Science degree in finance from the Kelley School of Business at Indiana University.

Eugene F. Reilly: CEO, The Americas

Mr. Reilly, 54, has been CEO, the Americas, since the Merger in June 2011 and he served as president, the Americas, as well as a number of other executive positions, at AMB from October 2003 until the Merger in June 2011. Mr. Reilly serves on the technical committee of FIBRA Prologis, a publicly traded Mexican REIT that is sponsored and managed by the company. Prior to joining AMB in October 2003, Mr. Reilly was chief investment officer of Cabot Properties, Inc., a private equity industrial real estate firm of which he was also a founding partner. From August 2009 until December 2015, Mr. Reilly served as a director of Strategic Hotels and Resorts, an owner and asset manager of high-end hotels and resorts. Mr. Reilly holds an A.B. degree in economics from Harvard College.

Edward S. Nekritz: Chief Legal Officer, General Counsel, and Secretary

Mr. Nekritz, 50, has been our chief legal officer, general counsel, and secretary since the Merger in June 2011. Mr. Nekritz was general counsel of the Trust from December 1998 to June 2011, secretary of the Trust from March 1999 to June 2011, and the Trust’s head of global strategic risk management from March 2009 to June 2011. Mr. Nekritz serves on the technical committee of FIBRA Prologis. Prior to joining the Trust in September 1995, Mr. Nekritz was an attorney with Mayer, Brown & Platt (now Mayer Brown LLP). Mr. Nekritz holds a Juris Doctor degree from the University of Chicago Law School and an A.B. degree in government from Harvard College.

Gary E. Anderson: CEO, Europe and Asia

Mr. Anderson, 50 has been our CEO, Europe and Asia, since the Merger in June 2011. Mr. Anderson held various positions with the Trust from August 1994 to June 2011, including head of the Trust’s global operations and fund business from March 2009 to June 2011 and president, Europe and Asia, from November 2006 to March 2009. Prior to joining the Trust, Mr. Anderson held various positions with Security Capital Group Incorporated, a diversified real estate investment company. Mr. Anderson holds a Master of Business Administration in finance and real estate from the Anderson Graduate School of Management at the University of California at Los Angeles and a Bachelor of Arts in marketing from Washington State University.

Michael S. Curless: Chief Investment Officer

Mr. Curless, 52, has been our chief investment officer since the Merger in June 2011. Mr. Curless was chief investment officer of the Trust from September 2010 to June 2011, and he was with the Trust in various capacities from August 1995 through February 2000. Mr. Curless was president and a principal at Lauth, a privately held national construction and development firm, from March 2000 until rejoining the Trust in September 2010. Prior thereto, he was a marketing director with the Trammell Crow Company. Mr. Curless holds a Master of Business Administration in finance and marketing and a Bachelor of Science in finance from the Kelley School of Business at Indiana University.

|

|

20

| |||

|

2016 Proxy Statement

|

EXECUTIVE COMPENSATION MATTERS

COMPENSATION DISCUSSION AND ANALYSIS

Summary of Compensation Discussion and Analysis

The Compensation Committee is committed to provide compensation opportunities that drive our business plan to create long-term value for our stockholders. It is of fundamental importance to us that our compensation program aligns the interests of our named executive officers (the “NEOs”) with the interests of our stockholders.

Prologis NEOs

Hamid Moghadam, Chief Executive Officer

Thomas Olinger, Chief Financial Officer

Eugene Reilly, CEO, the Americas

Edward Nekritz, Chief Legal Officer and General Counsel

Gary Anderson, CEO, Europe and Asia

Michael Curless, Chief Investment Officer

Key points of Compensation Discussion and Analysis

| 1. | Our business model is unique among REITs. As our customers become more and more global, we fill a niche as a logistics real estate company that meets the distribution center needs of our customers on four continents. The combination of our global reach, significant development platform (with $3.8 billion of construction in progress) and size and scope of our strategic capital business (accounting for 39.5% of our total assets under management) put us in a unique category among REITs. Our business model provides us with the capital and scale in global regions to meet our customers’ evolving logistics real estate requirements. |

| 2. | Our business model is creating long-term value. We are delivering on our strategic priorities and had record-breaking operational performance in 2015. Achievement of our strategic priorities positions us to take advantage of opportunities through the entire economic cycle. |

| 3. | Our compensation program supports our business model and provides incentives to achieve strong TSR performance. Our annual bonus program rewards successful execution of our strategic priorities. Long-term incentive equity awards represent a significant component of annual compensation and are completely formulaic based on relative 3-year TSR. Our outperformance compensation plans complete the total pay opportunity for our NEOs but only when exceptional levels of performance are reached. |

| 4. | Our compensation program is working. Compensation is heavily aligned with relative TSR performance. Our operational performance in 2015 was strong, so our NEOs’ bonuses (measured by operational metrics) were above target. However, our 3-year TSR underperformed, so our NEOs received only 50% of target value for their annual LTI equity awards in accordance with the established formula. Also, there was no payout under our outperformance compensation plans in 2015. Our core compensation program (annual base salary, annual bonus, and annual long-term incentives) is heavily weighted to align with relative TSR performance, which resulted in a decrease in overall compensation from 2014 despite our strong operational performance. |

All company operational information in CD&A is as of December 31, 2015, unless otherwise noted. See Appendix A for definitions and discussion of non-GAAP measurements and reconciliations to GAAP measures and for additional detail regarding definitions of terms as generally explained in CD&A.

|

|

21

| |||

|

2016 Proxy Statement

|

Prologis Business Model and Strategic Priorities

Our business is unique in the REIT industry

Our global operations and strategic capital and development businesses make us unique. The formidable combination of our global reach, strategic capital business and development platform places us in a unique category that sets us apart from other REITs. Our global operations in 20 countries, our $23.1 billion strategic capital business and our $3.8 billion development program are essential to our business model. These highly integrated components of our business give us the ability to provide high-quality logistics facilities in strategic locations that our customers need globally.

Our global operations and our strategic capital and development businesses function in tandem to provide unparalleled customer service. We provide a level of customer service to our global customers that differentiates us from our competitors. Our focus on customer service as a strategic advantage shapes our business model. We are global because our customers are global. To operate on a global level, we need a strategic capital business that gives us access to third party capital in global regions, which allows us to grow and enhance our returns while mitigating currency risk. Our development business provides the modern logistics space that our customers need in strategic global locations.

Prologis Business Model(1)

| OPERATIONS

Generate annual NOI by maintaining high occupancy rates and increasing rents

|

STRATEGIC CAPITAL

Access third-party capital to grow our business and earn recurring fees and promotes

|

DEVELOPMENT

Create value from development starts annually

|

||||||||||||||

| We have an irreplaceable portfolio of high-quality logistics facilities that serves premier brands across the globe. In 2015, we: | Durable fee stream with more than 90% from perpetual or long-life co-investment ventures.(2) In 2015, we:

|

Development contributes to significant earnings growth as projects lease up and generate NOI. In 2015, we:

|

||||||||||||||

| u Delivered $2.9 billion of annualized net operating income (“NOI”) reflecting a year-over-year increase of 15%

u Ended the fourth quarter with record occupancy of 96.9%

|

u Grew our third-party assets under management by 19% to $23.1 billion(3)

u Increased our fee and promote revenue from our eleven co-investment ventures by 16% to approximately $150 million

|

u Started $2.2 billion of development projects with an estimated value creation of $466.3 million

u Stabilized a total estimated investment of $1.8 billion of development projects with an estimated gross margin(4) of 31.8%, creating $586 million in value

|

||||||||||||||