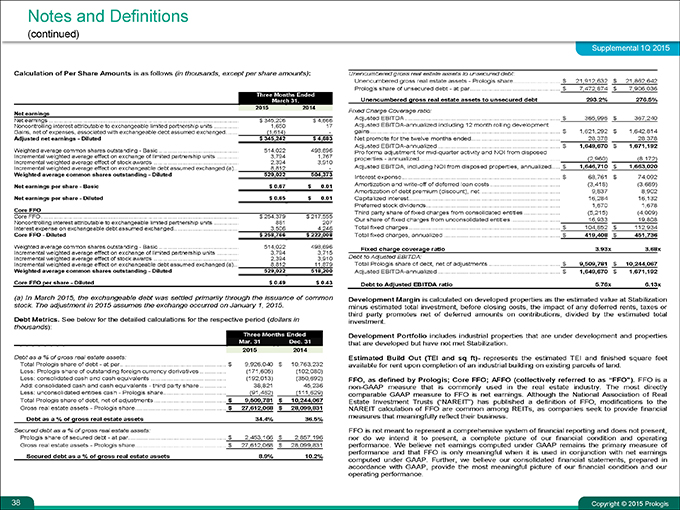

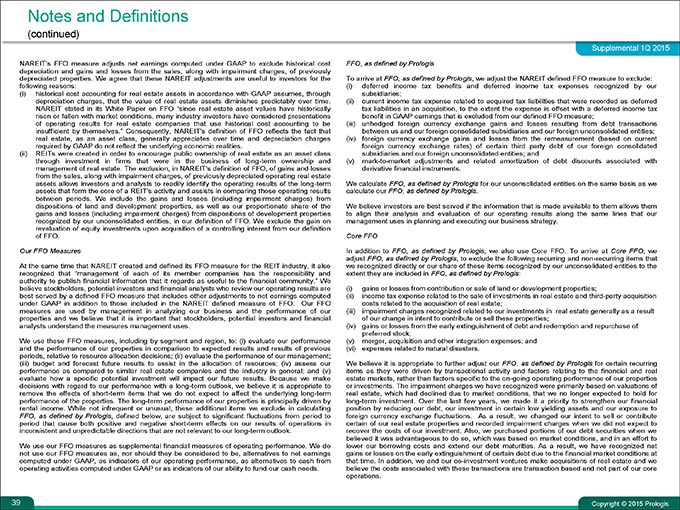

|

|

FIRST QUARTER 2015

Earnings Release and Supplemental Information

UNAUDITED

|

|

Table of Contents

Supplemental 1Q 2015

Prologis Park Prague D1 West DC4, Prague, Czech Republic

Prologis Park Osaka 5, Osaka, Japan

Stapleton Business Center North, Denver, Colorado, USA

Cover: Prologis Park Tres Rios, Mexico City, Mexico

Overview

Press Release 1

Highlights

Company Profile 4

Company Performance 5

Operating Performance 7

Guidance 8

Financial Information

Consolidated Balance Sheets 9

Pro-rata Balance Sheet Information 10

Consolidated Statements of Operations 11

Reconciliation of Net Earnings (Loss) to FFO 12

Pro-rata Operating Information and Reconciliation to FFO 13

EBITDA Reconciliation 14

Strategic Capital

Summary and Financial Highlights 15

Operating and Balance Sheet Information 16

Operations Overview

Operating Metrics 17

Operating Portfolio 19

Customer Information 22

Capital Deployment

Overview 23

Value Creation from Development Stabilization 24

Development Starts 25

Development Portfolio 26

Third Party Building Acquisitions 27

Dispositions and Contributions 28

Land Portfolio 29

Capitalization

Overview 31

Debt Summary 32

Debt Covenants and Other Metrics 33

Net Asset Value

Components 34

Notes and Definitions (A) 36

(A) Terms used throughout document are defined in the Notes and Definitions

Copyright © 2015 Prologis

Copyright ©

2015 Prologis

1

–

Core Funds From Operations Per Share Grew 14 Percent Year-Over-Year –

–

Rent Change on Rollovers Increased 9.7 Percent –

–

Stabilized $358.2 Million of Development with Estimated Margin of 35.5 Percent – –

Increases Mid-Point of 2015 Core FFO Guidance, excluding KTR Capital Partners transaction

–

SAN FRANCISCO (April 19, 2015) – Prologis, Inc. (NYSE: PLD), the global leader

in industrial real estate, today reported results for the first quarter 2015.

Core funds from operations (Core FFO) per diluted share was $0.49 for the

first quarter compared with $0.43 for the same period in 2014.

“We had an excellent start to the year and we continue to deliver growth

across our three lines of business,” said Hamid R. Moghadam, chairman and

CEO, Prologis. “Generally, market conditions are in great shape, and the scale,

quality and diversification of our global platform, combined with solid

execution by teams throughout the world, are driving strong financial

results.”

STRONG OPERATING PERFORMANCE RESULTING FROM FOCUSED

INVESTMENT STRATEGY

Prologis ended the quarter with 95.9 percent occupancy in its operating

portfolio, an increase of 140 basis points over the same period in 2014. In the

first quarter, the company leased 39.2 million square feet (3.6 million square

meters) in its combined operating and development portfolios, which includes

3.9 million square feet (0.4 million square meters) of properties under

development. Tenant retention was 86.3 percent.

Rent change on rollovers was positive, with GAAP rental rates on signed

leases increasing 9.7 percent. In the U.S., GAAP rental rates on signed leases

increased 15.1 percent.

During the first quarter, same store NOI for the owned and managed portfolio

increased 3.5 percent on a GAAP basis and 3.9 percent on an adjusted cash

basis. On a Prologis’ share basis, same store NOI increased 3.7 percent on a

GAAP basis and 4.2 percent on an adjusted cash basis.

PROFITABLE CAPITAL DEPLOYMENT

During the first quarter, Prologis invested $421.0 million ($278.6 million

Prologis’ share) at attractive yields.

Value Creation

The company generated $264.2 million ($259.3 million Prologis’ share) of

estimated value creation during the quarter. This includes $127.2 million ($122.3

million Prologis’ share) of estimated value creation from $358.2 million ($331.0

million Prologis’ share) of development stabilizations at an estimated

development margin of 35.5 percent and $137.0 million (of which 100% is

Prologis’ share) of value creation recognized through its value-added conversion

program.

“During the quarter we monetized one of our significant value-added conversion

projects, said Moghadam. While these projects are episodic, they

produce meaningful gains and NAV appreciation as we convert some of our infill

industrial properties higher and better use. Through the first quarter of 2015, we

have averaged approximately $50 million annually in gains from our value-add

efforts over the last nine years.”

Development Starts

The company started $280.1 million ($218.4 million Prologis share) of new

developments with an estimated weighted average yield upon stabilization of 7.1

percent and an estimated development margin of 20.5 percent. Build-to-suits

represented 16.5 percent of development starts in the first quarter.

At quarter end, the book value of the company’s land bank totaled $1.8 billion

with an estimated build-out potential of $11.1 billion.

Acquisitions

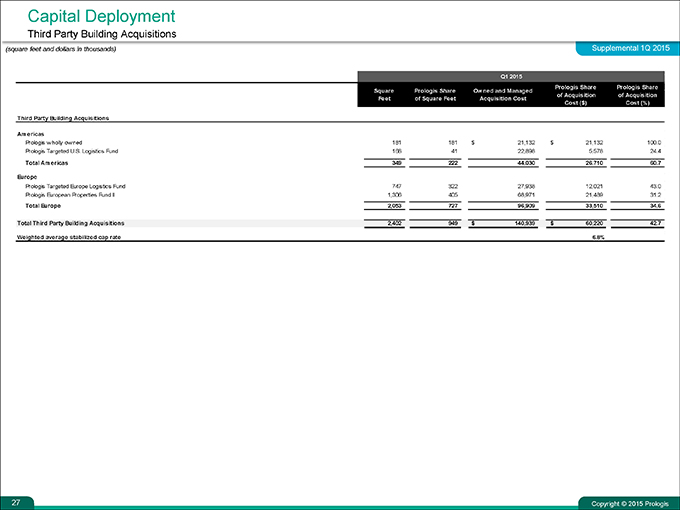

Prologis acquired $140.9 million ($60.2 million Prologis’ share) of buildings with

a stabilized capitalization rate on Prologis’ share of 6.8

percent. Dispositions and Contributions

Prologis completed $464.7 million ($461.6 million Prologis’ share) of third-party

building dispositions, primarily through its value-added conversion program, and

contributions to its co-investment ventures of $29.6 million ($20.4 million

Prologis’ share). Prologis’ share of dispositions and contributions had a

stabilized capitalization rate of 3.6 percent.

Prologis Announces First Quarter 2015 Earnings Results |

Copyright ©

2015 Prologis

2

CAPITAL MARKETS ACTIVITY INSULATES EARNINGS AND NAV FROM MOVEMENTS

IN FOREIGN CURRENCIES

Prologis completed $405.2 million of capital markets activity in the quarter and

increased its U.S. dollar net equity exposure to 91 percent.

“I am very pleased with our financial position, our balance sheet and credit

metrics are as strong as they have ever been,” said Tom Olinger, chief financial

officer, Prologis. “Additionally, we have effectively hedged the impact of foreign

currency movements on our estimated 2015 Core FFO, insulating our earnings

and net asset value.”

NET EARNINGS

Net earnings per diluted share was $0.65 for the first quarter compared with

$0.01 for the same period in 2014.

GUIDANCE NARROWED AND MIDPOINT RAISED FOR 2015

Guidance for 2015 does not include any impact from the KTR Capital Partners

transaction

Prologis narrowed its 2015 Core FFO guidance range to $2.07 to $2.13 per diluted

share from $2.04 to $2.12 per diluted share representing 12 percent growth at the

midpoint compared with full year 2014. The company expects to recognize net

earnings, for GAAP purposes, of $0.98 to $1.04 per share. This assumes (on an

owned and managed basis):

Year-end occupancy between 95.5 and 96.5 percent

GAAP same store NOI growth between 3.75 and 4.50 percent

Development stabilizations between $1.7 and $1.9 billion

Development starts between $2.3 and $2.6 billion

Building acquisitions between $1.0 and $1.5 billion

Contributions to co-investment ventures between $1.3 and $1.8 billion

Third-party dispositions between $2.1 billion and 2.5 billion

Strategic capital revenue between $195 and $205 million

Net G&A between $235 and $245 million

The Core FFO and earnings guidance reflected above excludes any potential

future gains (losses) recognized from real estate transactions. In reconciling

from net earnings to Core FFO, Prologis makes certain adjustments including

but not limited to real estate depreciation and amortization expenses, gains

(losses) recognized from real estate transactions and early extinguishment of

debt or redemption of preferred stock, impairment charges, deferred taxes

and unrealized gains or losses on foreign currency or derivative activity.

The difference between the company's Core FFO and net earnings guidance for 2015

relates predominantly to real estate depreciation and realized gains or losses on real

estate transactions.

NEW WEBCAST & CONFERENCE CALL INFORMATION

Prologis will host a live webcast and conference call with senior management to

discuss first quarter results, current market conditions and future outlook on April

20, at 8 a.m. U.S. Eastern time. Interested parties are encouraged to access the

webcast by clicking on the Investor Events and Presentations section on the

opening page of the Prologis Investor Relations website

(http://ir.prologis.com). Interested parties also can

participate via conference call by dialing +1 877 256 7020 (toll-free from the

U.S. and Canada) or +1 973 409 9692 (from all other countries) and entering conference

code 48765488. A telephonic replay will be available April 20-May 20 at +1

855 859 2056 (from the U.S. and Canada) or +1 404 537 3406 (from all other countries)

using conference code 48765488. The webcast replay will be posted when available in

the "Events & Presentations" section of Investor Relations on the Prologis

website. ABOUT PROLOGIS

Prologis, Inc., is the global leader in industrial real estate. As of March 31, 2015,

Prologis owned or had investments in, on a wholly owned basis or through

co-investment ventures, properties and development projects expected to total

approximately 594 million square feet (55 million square meters) in 21 countries.

The company leases modern distribution facilities to more than 4,700 customers,

including third-party logistics providers, transportation companies, retailers and

manufacturers.

FORWARD-LOOKING STATEMENTS

The statements in this document that are not historical facts are forward-looking

statements within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

These forward-looking statements are based on current expectations, estimates and

projections about the industry and markets in which Prologis operates,

management’s beliefs and assumptions made by management. Such statements

involve uncertainties that could significantly impact Prologis’ financial results. Words

such as “expects,” “anticipates,” “intends,”

“plans,” “believes,” “seeks,” “estimates,”

|

Copyright ©

2015 Prologis

3

variations of such words and similar expressions are intended to identify such

forward-looking statements, which generally are not historical in nature. All

statements that address operating performance, events or developments that we

expect or anticipate will occur in the future — including statements relating to rent

and occupancy growth, development activity and changes in sales or contribution

volume of properties, disposition activity, general conditions in the geographic

areas where we operate, our debt and financial position, our ability to form new

co-investment ventures and the availability of capital in existing or new co-

investment ventures — are forward-looking statements. These statements are not

guarantees of future performance and involve certain risks, uncertainties and

assumptions that are difficult to predict. Although we believe the expectations

reflected in any forward-looking statements are based on reasonable assumptions,

we can give no assurance that our expectations will be attained and therefore,

actual outcomes and results may differ materially from what is expressed or

forecasted in such forward-looking statements. Some of the factors that may affect

outcomes and results include, but are not limited to: (i) national, international,

regional and local economic climates, (ii) changes in financial markets, interest

rates and foreign currency exchange rates, (iii) increased or unanticipated

competition for our properties, (iv) risks associated with acquisitions, dispositions

and development of properties, (v) maintenance of real estate investment trust

(“REIT”) status and tax structuring, (vi) availability of financing and capital, the

levels of debt that we maintain and our credit ratings, (vii) risks related to our

investments in our co-investment ventures and funds, including our ability to

establish new co-investment ventures and funds, (viii) risks of doing business

internationally, including currency risks, (ix) environmental uncertainties, including

risks of natural disasters, and (x) those additional factors discussed in reports filed

with the Securities and Exchange Commission by Prologis under the heading “Risk

Factors.” Prologis undertakes no duty to update any forward-looking statements

appearing in this document.

MEDIA CONTACTS

Tracy Ward, Tel: +1 415 733 9565, tward@prologis.com, San

Francisco Nina Beizai, Tel: +1 415 733 9493,

nbeizai@prologis.com, San Francisco

|

|

|

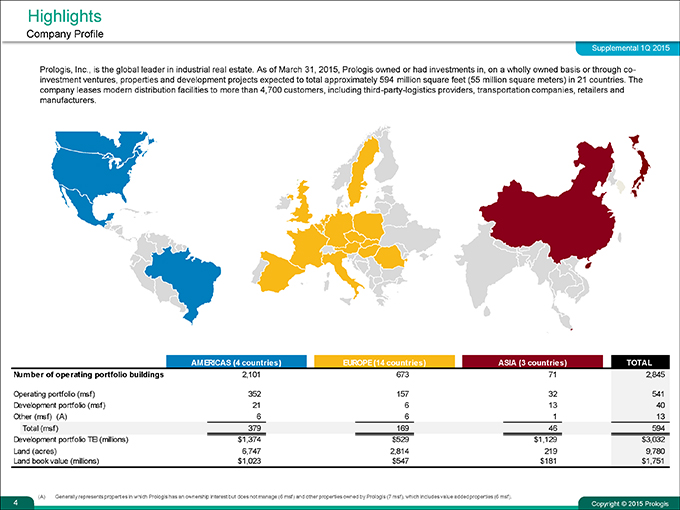

Highlights

Company Profile

Supplemental 1Q 2015

Prologis, Inc., is the global leader in industrial real estate. As of March 31, 2015, Prologis owned or had investments in, on a wholly owned basis or through co-investment ventures, properties and development projects expected to total approximately 594 million square feet (55 million square meters) in 21 countries. The company leases modern distribution facilities to more than 4,700 customers, including third-party-logistics providers, transportation companies, retailers and manufacturers.

AMERICAS (4 countries) EUROPE (14 countries) ASIA (3 countries) TOTAL

Number of operating portfolio buildings 2,101 673 71 2,845

Operating portfolio (msf) 352 157 32 541

Development portfolio (msf) 21 6 13 40

Other (msf) (A) 6 6 1 13

Total (msf) 379 169 46 594

Development portfolio TEI (millions) $1,374 $529 $1,129 $3,032

Land (acres) 6,747 2,814 219 9,780

Land book value (millions) $1,023 $547 $181 $1,751

(A) Generally represents properties in which Prologis has an ownership interest but does not manage (6 msf) and other properties owned by Prologis (7 msf), which includes value added properties (6 msf).

Copyright © 2015 Prologis

4

|

|

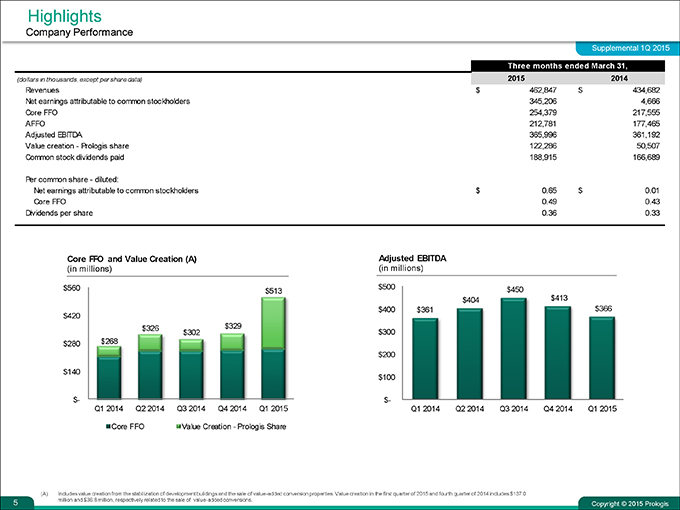

Highlights

Company Performance

Supplemental 1Q 2015

Three months ended March 31,

(dollars in thousands, except per share data) 2015 2014

Revenues $ 462,847 $ 434,682

Net earnings attributable to common stockholders 345,206 4,666

Core FFO 254,379 217,555

AFFO 212,781 177,465

Adjusted EBITDA 365,996 361,192

Value creation—Prologis share 122,286 50,507

Common stock dividends paid 188,915 166,689

Per common share—diluted:

Net earnings attributable to common stockholders $ 0.65 $ 0.01

Core FFO 0.49 0.43

Dividends per share 0.36 0.33

Core FFO and Value Creation (A) Adjusted EBITDA

(in millions)(in millions)

$560 $513 $500 $450

$404 $413

$400 $361 $366

$420

$326 $329

$302 $300

$280 $268

$200

$140

$100

$- $-

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Core FFO Value Creation—Prologis Share

(A) Includes value creation from the stabilization of development buildings and the sale of value-added conversion properties. Value creation in the first quarter of 2015 and fourth quarter of 2014 includes $137.0 million and $36.8 million, respectively related to the sale of value-added conversions.

Copyright © 2015 Prologis

5

|

|

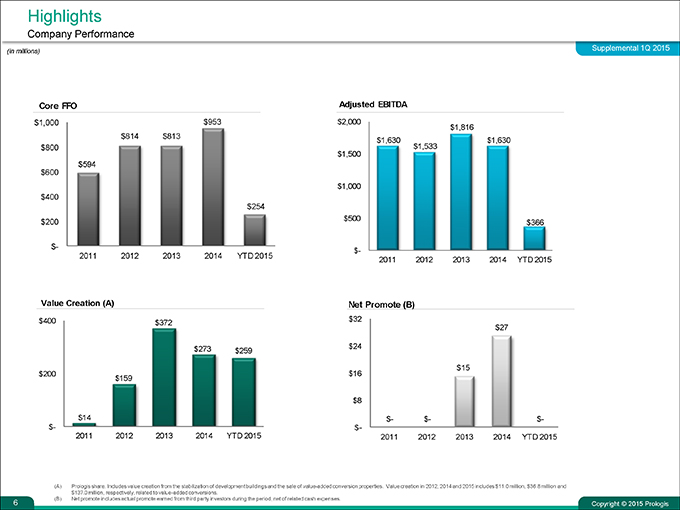

Highlights

Company Performance

(in millions) Supplemental 1Q 2015

Core FFO Adjusted EBITDA

$1,000 $953 $2,000 $1,816

$814 $813 $1,630 $1,630

$800 $1,533

$1,500

$594

$600

$1,000

$400

$254

$200 $500 $366

$- $-

2011 2012 2013 2014 YTD 2015 2011 2012 2013 2014 YTD 2015

Value Creation (A) Net Promote (B)

$400 $372 $32 $27

$273 $259 $24

$15

$ $16

$8

$- $- $-

$-

YTD 2015 2011 2012 2013 2014 YTD 2015

(A) Prologis share. Includes value creation from the stabilization of development buildings and the sale of value-added conversion properties. Value creation in 2012, 2014 and 2015 includes $11.0 million, $36.8 million and $137.0 million, respectively, related to value-added conversions.

(B) Net promote includes actual promote earned from third party investors during the period, net of related cash expenses.

Copyright © 2015 Prologis

6

|

|

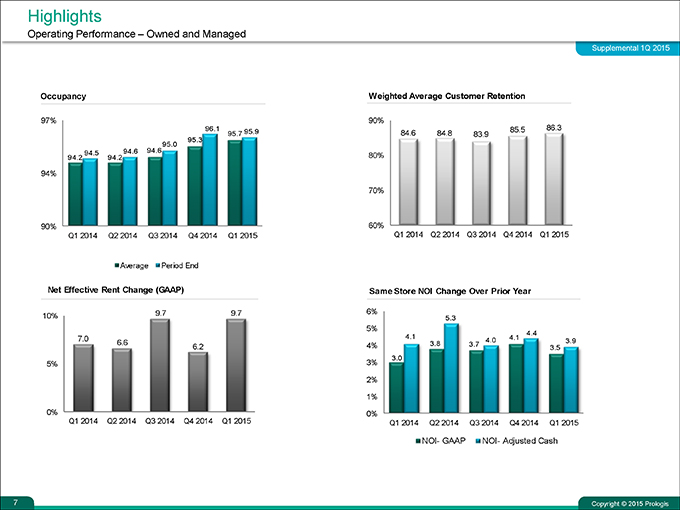

Highlights

Operating Performance – Owned and Managed

Supplemental 1Q 2015

Occupancy Weighted Average Customer Retention

97% 90%

96.1 95.7 95.9 84.6 84.8 83.9 85.5 86.3

95.0 95.3

94.5 94.6 94.6

94.2 94.2 80%

94%

70%

90% 60%

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Average Period End

Net Effective Rent Change (GAAP) Same Store NOI Change Over Prior Year

9.7 9.7 6%

10% 5.3

5% 4.4

7.0 4.1 4.0 4.1 3.9

6.6 6.2 4% 3.8 3.7 3.5

3.0

5% 3%

2%

1%

0%

015 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

NOI- GAAP NOI- Adjusted Cash

Copyright © 2015 Prologis

7

|

|

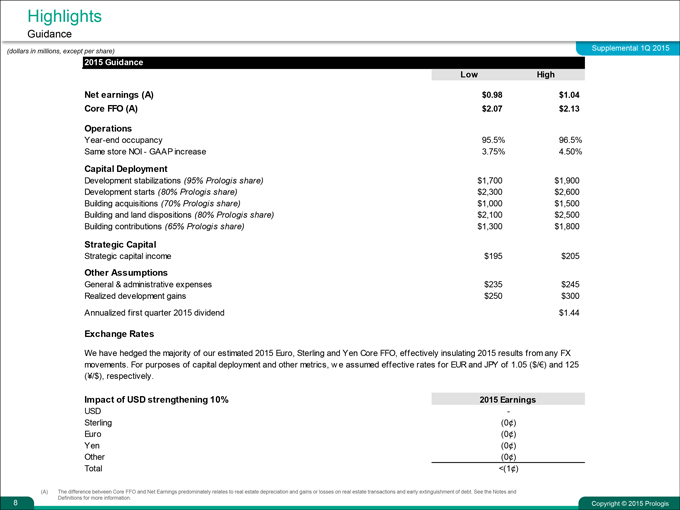

Copyright © 2015 Prologis Supplemental 1Q 2015

Highlights

Guidance

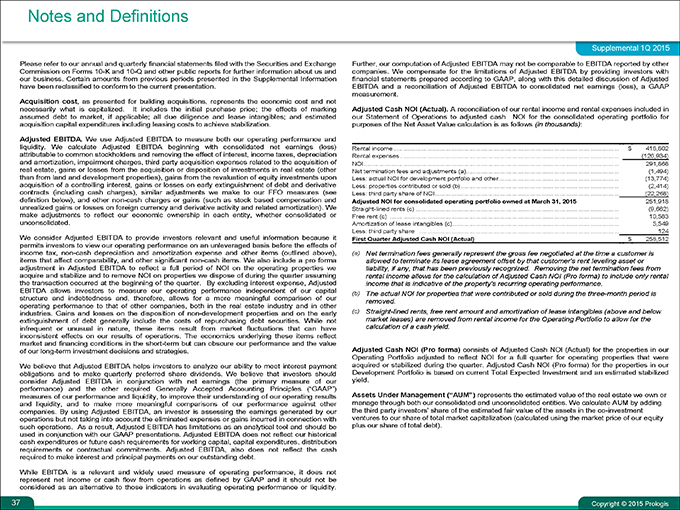

(A)The difference between Core FFO and Net Earnings predominately relates to real estate depreciation and gains or losses on real estate transactions and early extinguishment of debt. See the Notes and Definitions for more information.

(dollars in millions, except per share) 2015 Guidance LowHighNet earnings (A)$0.98$1.04Core FFO (A)$2.07$2.13OperationsYear-end occupancy95.5%96.5%Same store NOI - GAAP increase3.75%4.50%Capital DeploymentDevelopment stabilizations (95% Prologis share)$1,700$1,900Development starts (80% Prologis share)$2,300$2,600Building acquisitions (70% Prologis share)$1,000$1,500Building and land dispositions (80% Prologis share)$2,100$2,500Building contributions (65% Prologis share)$1,300$1,800Strategic CapitalStrategic capital income$195$205Other AssumptionsGeneral & administrative expenses$235$245Annualized first quarter 2015 dividend$1.44Exchange RatesImpact of USD strengthening 10%2015 EarningsUSD-Sterling(0¢)Euro(0¢)Yen(0¢)Other(0¢)Total<(1¢)We have hedged the majority of our estimated 2015 Euro, Sterling and Yen Core FFO, effectively insulating 2015 results from any FX movements. For purposes of capital deployment and other metrics, we assumed effective rates for EUR and JPY of 1.05 ($/¬) and 125 (¥/$), respectively.

8

|

|

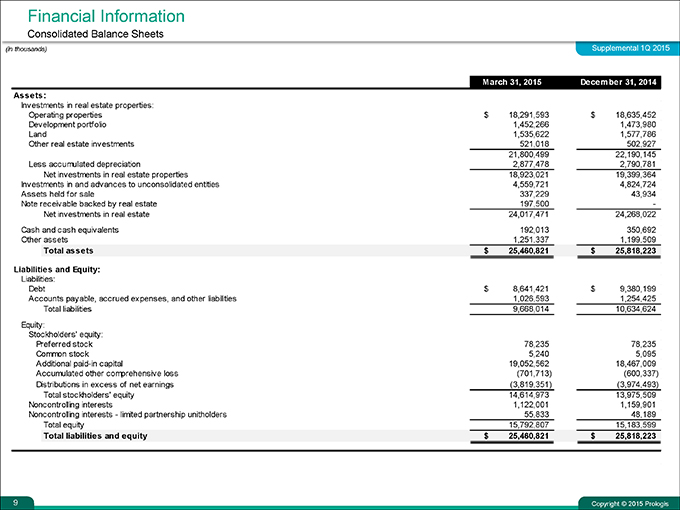

Financial Information

Consolidated Balance Sheets

(in thousands) Supplemental 1Q 2015

March 31, 2015 December 31, 2014

Assets:

Investments in real estate properties:

Operating properties $ 18,291,593 $ 18,635,452

Development portfolio 1,452,266 1,473,980

Land 1,535,622 1,577,786

Other real estate investments 521,018 502,927

21,800,499 22,190,145

Less accumulated depreciation 2,877,478 2,790,781

Net investments in real estate properties 18,923,021 19,399,364

Investments in and advances to unconsolidated entities 4,559,721 4,824,724

Assets held for sale 337,229 43,934

Note receivable backed by real estate 197,500 -

Net investments in real estate 24,017,471 24,268,022

Cash and cash equivalents 192,013 350,692

Other assets 1,251,337 1,199,509

Total assets $ 25,460,821 $ 25,818,223

Liabilities and Equity:

Liabilities:

Debt $ 8,641,421 $ 9,380,199

Accounts payable, accrued expenses, and other liabilities 1,026,593 1,254,425

Total liabilities 9,668,014 10,634,624

Equity:

Stockholders’ equity:

Preferred stock 78,235 78,235

Common stock 5,240 5,095

Additional paid-in capital 19,052,562 18,467,009

Accumulated other comprehensive loss (701,713) (600,337)

Distributions in excess of net earnings (3,819,351) (3,974,493)

Total stockholders’ equity 14,614,973 13,975,509

Noncontrolling interests 1,122,001 1,159,901

Noncontrolling interests—limited partnership unitholders 55,833 48,189

Total equity 15,792,807 15,183,599

Total liabilities and equity $ 25,460,821 $ 25,818,223

Copyright © 2015 Prologis

9

|

|

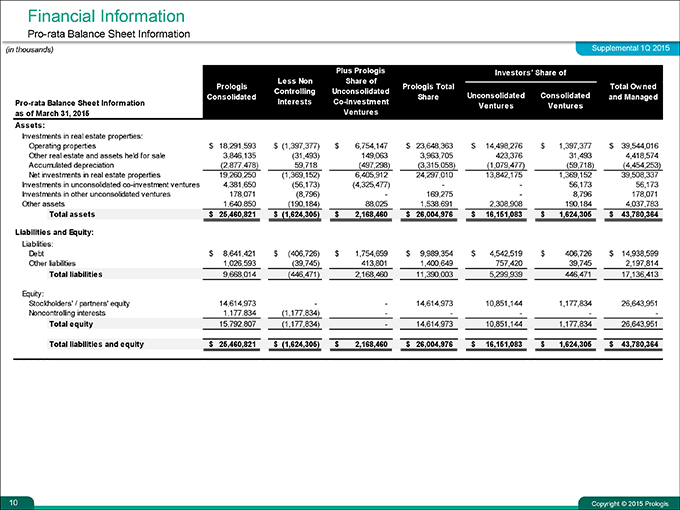

Financial Information

Pro-rata Balance Sheet Information

(in thousands) Supplemental 1Q 2015

Plus Prologis Investors’ Share of

Less Non Share of

Prologis Prologis Total Total Owned

Controlling Unconsolidated

Consolidated Share Unconsolidated Consolidated and Managed

Pro-rata Balance Sheet Information Interests Co-Investment Ventures Ventures

as of March 31, 2015 Ventures

Assets:

Investments in real estate properties:

Operating properties $ 18,291,593 $ (1,397,377) $ 6,754,147 $ 23,648,363 $ 14,498,276 $ 1,397,377 $ 39,544,016

Other real estate and assets held for sale 3,846,135 (31,493) 149,063 3,963,705 423,376 31,493 4,418,574

Accumulated depreciation(2,877,478) 59,718 (497,298) (3,315,058) (1,079,477) (59,718) (4,454,253)

Net investments in real estate properties 19,260,250 (1,369,152) 6,405,912 24,297,010 13,842,175 1,369,152 39,508,337

Investments in unconsolidated co-investment ventures 4,381,650 (56,173) (4,325,477) — 56,173 56,173

Investments in other unconsolidated ventures 178,071 (8,796) — 169,275 — 8,796 178,071

Other assets 1,640,850 (190,184) 88,025 1,538,691 2,308,908 190,184 4,037,783

Total assets $ 25,460,821 $ (1,624,305) $ 2,168,460 $ 26,004,976 $ 16,151,083 $ 1,624,305 $ 43,780,364

Liabilities and Equity:

Liabilities:

Debt $ 8,641,421 $ (406,726) $ 1,754,659 $ 9,989,354 $ 4,542,519 $ 406,726 $ 14,938,599

Other liabilities 1,026,593 (39,745) 413,801 1,400,649 757,420 39,745 2,197,814

Total liabilities 9,668,014 (446,471) 2,168,460 11,390,003 5,299,939 446,471 17,136,413

Equity:

Stockholders’ / partners’ equity 14,614,973 — 14,614,973 10,851,144 1,177,834 26,643,951

Noncontrolling interests 1,177,834(1,177,834)

Total equity 15,792,807 (1,177,834) — 14,614,973 10,851,144 1,177,834 26,643,951

Total liabilities and equity $ 25,460,821 $ (1,624,305) $ 2,168,460 $ 26,004,976 $ 16,151,083 $ 1,624,305 $ 43,780,364

Copyright © 2015 Prologis

10

|

|

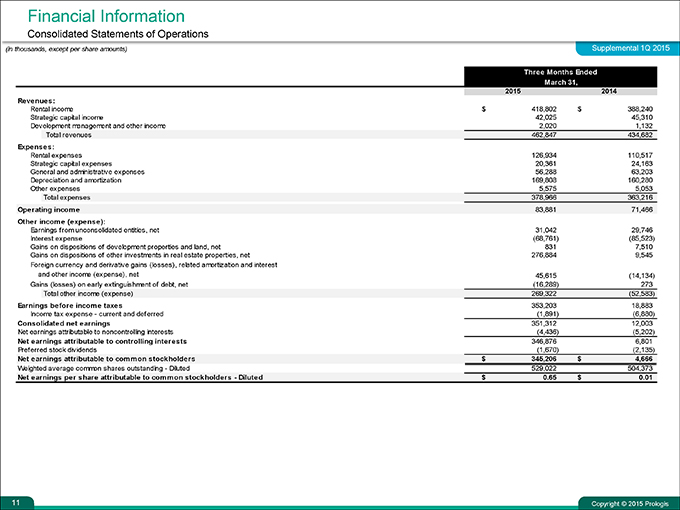

Financial Information

Consolidated Statements of Operations

(in thousands, except per share amounts) Supplemental 1Q 2015

Three Months Ended

March 31,

2015 2014

Revenues:

Rental income $ 418,802 $ 388,240

Strategic capital income 42,025 45,310

Development management and other income 2,020 1,132

Total revenues 462,847 434,682

Expenses:

Rental expenses 126,934 110,517

Strategic capital expenses 20,361 24,163

General and administrative expenses 56,288 63,203

Depreciation and amortization 169,808 160,280

Other expenses 5,575 5,053

Total expenses 378,966 363,216

Operating income 83,881 71,466

Other income (expense):

Earnings from unconsolidated entities, net 31,042 29,746

Interest expense (68,761) (85,523)

Gains on dispositions of development properties and land, net 831 7,510

Gains on dispositions of other investments in real estate properties, net 276,884 9,545

Foreign currency and derivative gains (losses), related amortization and interest

and other income (expense), net 45,615 (14,134)

Gains (losses) on early extinguishment of debt, net (16,289) 273

Total other income (expense) 269,322 (52,583)

Earnings before income taxes 353,203 18,883

Income tax expense—current and deferred (1,891) (6,880)

Consolidated net earnings 351,312 12,003

Net earnings attributable to noncontrolling interests (4,436) (5,202)

Net earnings attributable to controlling interests 346,876 6,801

Preferred stock dividends (1,670) (2,135)

Net earnings attributable to common stockholders $ 345,206 $ 4,666

Weighted average common shares outstanding—Diluted 529,022 504,373

Net earnings per share attributable to common stockholders—Diluted $ 0.65 $ 0.01

Copyright © 2015 Prologis

11

|

|

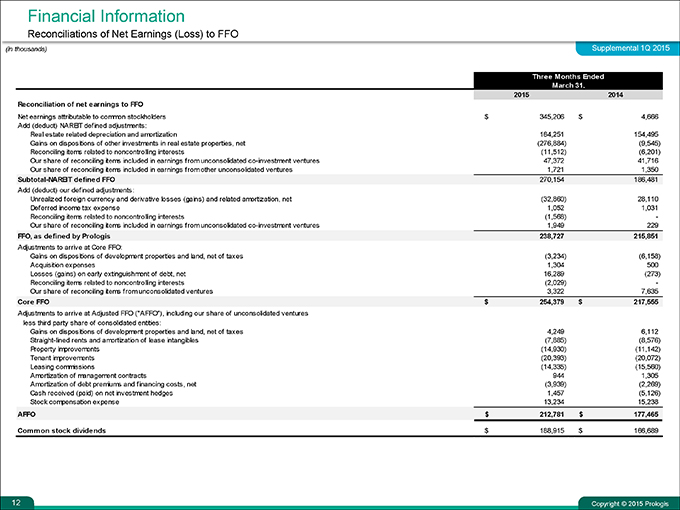

Financial Information

Reconciliations of Net Earnings (Loss) to FFO

(in thousands) Supplemental 1Q 2015

Three Months Ended

March 31,

2015 2014

Reconciliation of net earnings to FFO

Net earnings attributable to common stockholders $ 345,206 $ 4,666

Add (deduct) NAREIT defined adjustments:

Real estate related depreciation and amortization 164,251 154,495

Gains on dispositions of other investments in real estate properties, net(276,884)(9,545)

Reconciling items related to noncontrolling interests(11,512)(6,201)

Our share of reconciling items included in earnings from unconsolidated co-investment ventures 47,372 41,716

Our share of reconciling items included in earnings from other unconsolidated ventures 1,721 1,350

Subtotal-NAREIT defined FFO 270,154 186,481

Add (deduct) our defined adjustments:

Unrealized foreign currency and derivative losses (gains) and related amortization, net(32,860) 28,110

Deferred income tax expense 1,052 1,031

Reconciling items related to noncontrolling interests(1,568) -

Our share of reconciling items included in earnings from unconsolidated co-investment ventures 1,949 229

FFO, as defined by Prologis 238,727 215,851

Adjustments to arrive at Core FFO:

Gains on dispositions of development properties and land, net of taxes(3,234)(6,158)

Acquisition expenses 1,304 500

Losses (gains) on early extinguishment of debt, net 16,289(273)

Reconciling items related to noncontrolling interests(2,029) -

Our share of reconciling items from unconsolidated ventures 3,322 7,635

Core FFO $ 254,379 $ 217,555

Adjustments to arrive at Adjusted FFO (“AFFO”), including our share of unconsolidated ventures

less third party share of consolidated entities:

Gains on dispositions of development properties and land, net of taxes 4,249 6,112

Straight-lined rents and amortization of lease intangibles(7,885)(8,576)

Property improvements(14,930)(11,142)

Tenant improvements(20,393)(20,072)

Leasing commissions(14,335)(15,560)

Amortization of management contracts 944 1,305

Amortization of debt premiums and financing costs, net(3,939)(2,269)

Cash received (paid) on net investment hedges 1,457(5,126)

Stock compensation expense 13,234 15,238

AFFO $ 212,781 $ 177,465

Common stock dividends $ 188,915 $ 166,689

Copyright © 2015 Prologis

12

|

|

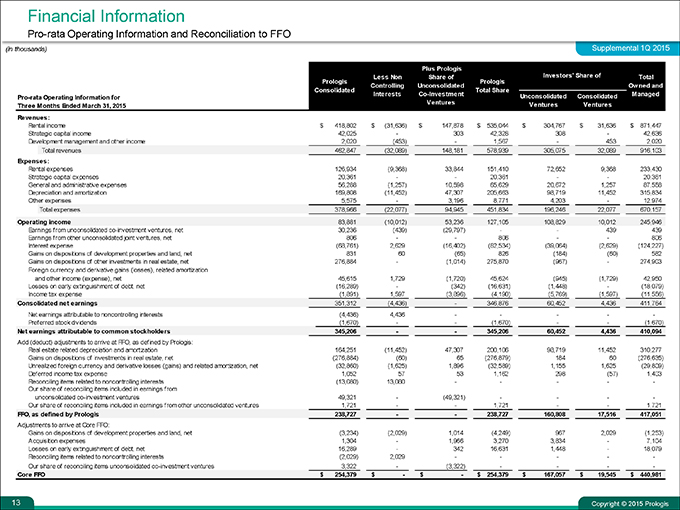

Financial Information

Pro-rata Operating Information and Reconciliation to FFO

(in thousands) Supplemental 1Q 2015

Plus Prologis

Less Non Share of Investors’ Share of Total

Prologis Prologis

Controlling Unconsolidated Owned and

Consolidated Total Share

Pro-rata Operating Information for Interests Co-Investment Unconsolidated Consolidated Managed

Three Months Ended March 31, 2015 Ventures Ventures Ventures

Revenues:

Rental income $ 418,802 $ (31,636) $ 147,878 $ 535,044 $ 304,767 $ 31,636 $ 871,447

Strategic capital income 42,025 — 303 42,328 308 — 42,636

Development management and other income 2,020 (453) — 1,567 — 453 2,020

Total revenues 462,847 (32,089) 148,181 578,939 305,075 32,089 916,103

Expenses:

Rental expenses 126,934 (9,368) 33,844 151,410 72,652 9,368 233,430

Strategic capital expenses 20,361 — 20,361 — 20,361

General and administrative expenses 56,288 (1,257) 10,598 65,629 20,672 1,257 87,558

Depreciation and amortization 169,808 (11,452) 47,307 205,663 98,719 11,452 315,834

Other expenses 5,575 — 3,196 8,771 4,203 — 12,974

Total expenses 378,966(22,077) 94,945 451,834 196,246 22,077 670,157

Operating income 83,881(10,012) 53,236 127,105 108,829 10,012 245,946

Earnings from unconsolidated co-investment ventures, net 30,236 (439) (29,797) — 439 439

Earnings from other unconsolidated joint ventures, net 806 — 806 — 806

Interest expense (68,761) 2,629 (16,402) (82,534) (39,064) (2,629) (124,227)

Gains on dispositions of development properties and land, net 831 60 (65) 826 (184) (60) 582

Gains on dispositions of other investments in real estate, net 276,884 — (1,014) 275,870 (967) — 274,903

Foreign currency and derivative gains (losses), related amortization

and other income (expense), net 45,615 1,729 (1,720) 45,624 (945) (1,729) 42,950

Losses on early extinguishment of debt, net (16,289) — (342) (16,631) (1,448) — (18,079)

Income tax expense (1,891) 1,597 (3,896) (4,190) (5,769) (1,597) (11,556)

Consolidated net earnings 351,312 (4,436) — 346,876 60,452 4,436 411,764

Net earnings attributable to noncontrolling interests (4,436) 4,436

Preferred stock dividends (1,670) — (1,670) — (1,670)

Net earnings attributable to common stockholders 345,206 — 345,206 60,452 4,436 410,094

Add (deduct) adjustments to arrive at FFO, as defined by Prologis:

Real estate related depreciation and amortization 164,251 (11,452) 47,307 200,106 98,719 11,452 310,277

Gains on dispositions of investments in real estate, net (276,884) (60) 65 (276,879) 184 60 (276,635)

Unrealized foreign currency and derivative losses (gains) and related amortization, net (32,860) (1,625) 1,896 (32,589) 1,155 1,625 (29,809)

Deferred income tax expense 1,052 57 53 1,162 298 (57) 1,403

Reconciling items related to noncontrolling interests (13,080) 13,080

Our share of reconciling items included in earnings from

unconsolidated co-investment ventures 49,321 - (49,321)

Our share of reconciling items included in earnings from other unconsolidated ventures 1,721 — 1,721 — 1,721

FFO, as defined by Prologis 238,727 — 238,727 160,808 17,516 417,051

Adjustments to arrive at Core FFO:

Gains on dispositions of development properties and land, net (3,234) (2,029) 1,014 (4,249) 967 2,029 (1,253)

Acquisition expenses 1,304—1,966 3,270 3,834—7,104

Losses on early extinguishment of debt, net 16,289—342 16,631 1,448—18,079

Reconciling items related to noncontrolling interests (2,029) 2,029

Our share of reconciling items unconsolidated co-investment ventures 3,322 - (3,322)

Core FFO $ 254,379 $—$—$ 254,379 $ 167,057 $ 19,545 $ 440,981

Copyright © 2015 Prologis

13

|

|

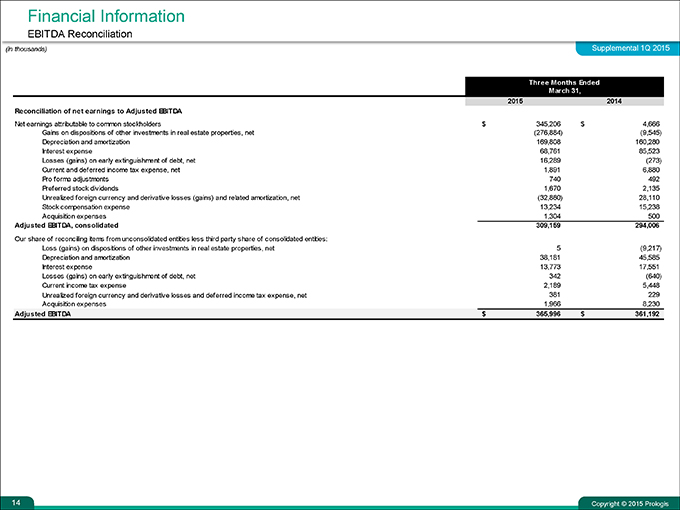

Financial Information

EBITDA Reconciliation

(in thousands) Supplemental 1Q 2015

Three Months Ended

March 31,

2015 2014

Reconciliation of net earnings to Adjusted EBITDA

Net earnings attributable to common stockholders $ 345,206 $ 4,666

Gains on dispositions of other investments in real estate properties, net (276,884) (9,545)

Depreciation and amortization 169,808 160,280

Interest expense 68,761 85,523

Losses (gains) on early extinguishment of debt, net 16,289 (273)

Current and deferred income tax expense, net 1,891 6,880

Pro forma adjustments 740 492

Preferred stock dividends 1,670 2,135

Unrealized foreign currency and derivative losses (gains) and related amortization, net (32,860) 28,110

Stock compensation expense 13,234 15,238

Acquisition expenses 1,304 500

Adjusted EBITDA, consolidated 309,159 294,006

Our share of reconciling items from unconsolidated entities less third party share of consolidated entities:

Loss (gains) on dispositions of other investments in real estate properties, net 5 (9,217)

Depreciation and amortization 38,181 45,585

Interest expense 13,773 17,551

Losses (gains) on early extinguishment of debt, net 342 (640)

Current income tax expense 2,189 5,448

Unrealized foreign currency and derivative losses and deferred income tax expense, net 381 229

Acquisition expenses 1,966 8,230

Adjusted EBITDA $ 365,996 $ 361,192

Copyright © 2015 Prologis

14

|

|

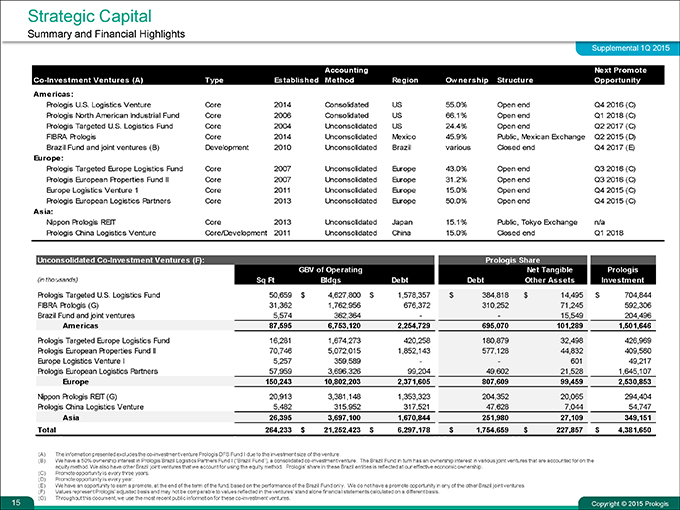

Strategic Capital

Summary and Financial Highlights

Supplemental 1Q 2015

Accounting Next Promote

Co-Investment Ventures (A) Type Established Method Region Ownership Structure Opportunity

Americas:

Prologis U.S. Logistics Venture Core 2014 Consolidated US 55.0% Open end Q4 2016 (C)

Prologis North American Industrial Fund Core 2006 Consolidated US 66.1% Open end Q1 2018 (C)

Prologis Targeted U.S. Logistics Fund Core 2004 Unconsolidated US 24.4% Open end Q2 2017 (C)

FIBRA Prologis Core 2014 Unconsolidated Mexico 45.9% Public, Mexican Exchange Q2 2015 (D)

Brazil Fund and joint ventures (B) Development 2010 Unconsolidated Brazil various Closed end Q4 2017 (E)

Europe:

Prologis Targeted Europe Logistics Fund Core 2007 Unconsolidated Europe 43.0% Open end Q3 2016 (C)

Prologis European Properties Fund II Core 2007 Unconsolidated Europe 31.2% Open end Q3 2016 (C)

Europe Logistics Venture 1 Core 2011 Unconsolidated Europe 15.0% Open end Q4 2015 (C)

Prologis European Logistics Partners Core 2013 Unconsolidated Europe 50.0% Open end Q4 2015 (C)

Asia:

Nippon Prologis REIT Core 2013 Unconsolidated Japan 15.1% Public, Tokyo Exchange n/a

Prologis China Logistics Venture Core/Development 2011 Unconsolidated China 15.0% Closed end Q1 2018

Unconsolidated Co-Investment Ventures (F): Prologis Share

GBV of Operating Net Tangible Prologis

(in thousands) Sq Ft Bldgs Debt Debt Other Assets Investment

Prologis Targeted U.S. Logistics Fund 50,659 $ 4,627,800 $ 1,578,357 $ 384,818 $ 14,495 $ 704,844

FIBRA Prologis (G) 31,362 1,762,956 676,372 310,252 71,245 592,306

Brazil Fund and joint ventures 5,574 362,364 — 15,549 204,496

Americas 87,595 6,753,120 2,254,729 695,070 101,289 1,501,646

Prologis Targeted Europe Logistics Fund 16,281 1,674,273 420,258 180,879 32,498 426,969

Prologis European Properties Fund II 70,746 5,072,015 1,852,143 577,128 44,832 409,560

Europe Logistics Venture I 5,257 359,589 — 601 49,217

Prologis European Logistics Partners 57,959 3,696,326 99,204 49,602 21,528 1,645,107

Europe 150,243 10,802,203 2,371,605 807,609 99,459 2,530,853

Nippon Prologis REIT (G) 20,913 3,381,148 1,353,323 204,352 20,065 294,404

Prologis China Logistics Venture 5,482 315,952 317,521 47,628 7,044 54,747

Asia 26,395 3,697,100 1,670,844 251,980 27,109 349,151

Total 264,233 $ 21,252,423 $ 6,297,178 $ 1,754,659 $ 227,857 $ 4,381,650

(A) The information presented excludes the co-investment venture Prologis DFS Fund I due to the investment size of the venture.

(B) We have a 50% ownership interest in Prologis Brazil Logistics Partners Fund I (“Brazil Fund”), a consolidated co-investment venture. The Brazil Fund in turn has an ownership interest in various joint ventures that are accounted for on the equity method. We also have other Brazil joint ventures that we account for using the equity method. Prologis’ share in these Brazil entities is reflected at our effective economic ownership.

(C) Promote opportunity is every three years. (D) Promote opportunity is every year.

(E) We have an opportunity to earn a promote, at the end of the term of the fund, based on the performance of the Brazil Fund only. We do not have a promote opportunity in any of the other Brazil joint ventures.

(F) Values represent Prologis’ adjusted basis and may not be comparable to values reflected in the ventures’ stand alone financial statements calculated on a different basis.

(G) Throughout this document, we use the most recent public information for these co-investment ventures.

Copyright © 2015 Prologis

15

|

|

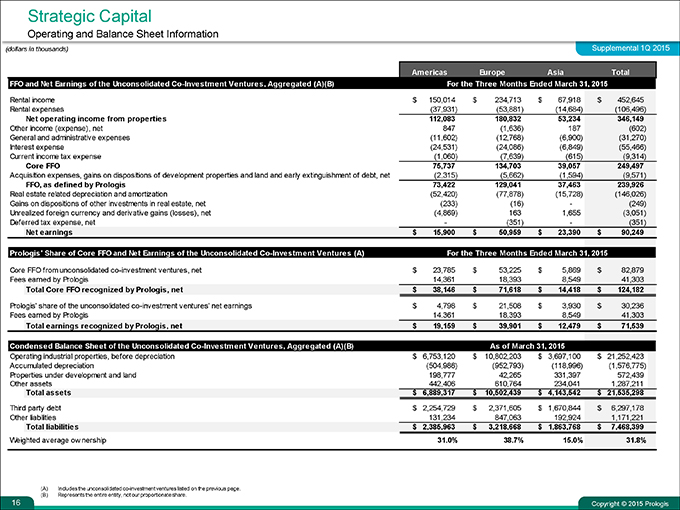

Strategic Capital

Operating and Balance Sheet Information

(dollars in thousands) Supplemental 1Q 2015

Americas Europe Asia Total

FFO and Net Earnings of the Unconsolidated Co-Investment Ventures, Aggregated (A)(B) For the Three Months Ended March 31, 2015

Rental income $ 150,014 $ 234,713 $ 67,918 $ 452,645

Rental expenses(37,931)(53,881)(14,684)(106,496)

Net operating income from properties 112,083 180,832 53,234 346,149

Other income (expense), net 847(1,636) 187(602)

General and administrative expenses(11,602)(12,768)(6,900)(31,270)

Interest expense(24,531)(24,086)(6,849)(55,466)

Current income tax expense(1,060)(7,639)(615)(9,314)

Core FFO 75,737 134,703 39,057 249,497

Acquisition expenses, gains on dispositions of development properties and land and early extinguishment of debt, net(2,315)(5,662)(1,594)(9,571)

FFO, as defined by Prologis 73,422 129,041 37,463 239,926

Real estate related depreciation and amortization(52,420)(77,878)(15,728)(146,026)

Gains on dispositions of other investments in real estate, net(233)(16) -(249)

Unrealized foreign currency and derivative gains (losses), net(4,869) 163 1,655(3,051)

Deferred tax expense, net -(351) -(351)

Net earnings $ 15,900 $ 50,959 $ 23,390 $ 90,249

Prologis’ Share of Core FFO and Net Earnings of the Unconsolidated Co-Investment Ventures (A) For the Three Months Ended March 31, 2015

Core FFO from unconsolidated co-investment ventures, net $ 23,785 $ 53,225 $ 5,869 $ 82,879

Fees earned by Prologis 14,361 18,393 8,549 41,303

Total Core FFO recognized by Prologis, net $ 38,146 $ 71,618 $ 14,418 $ 124,182

Prologis’ share of the unconsolidated co-investment ventures’ net earnings $ 4,798 $ 21,508 $ 3,930 $ 30,236

Fees earned by Prologis 14,361 18,393 8,549 41,303

Total earnings recognized by Prologis, net $ 19,159 $ 39,901 $ 12,479 $ 71,539

Condensed Balance Sheet of the Unconsolidated Co-Investment Ventures, Aggregated (A)(B) As of March 31, 2015

Operating industrial properties, before depreciation $ 6,753,120 $ 10,802,203 $ 3,697,100 $ 21,252,423

Accumulated depreciation(504,986)(952,793)(118,996)(1,576,775)

Properties under development and land 198,777 42,265 331,397 572,439

Other assets 442,406 610,764 234,041 1,287,211

Total assets $ 6,889,317 $ 10,502,439 $ 4,143,542 $ 21,535,298

Third party debt $ 2,254,729 $ 2,371,605 $ 1,670,844 $ 6,297,178

Other liabilities 131,234 847,063 192,924 1,171,221

Total liabilities $ 2,385,963 $ 3,218,668 $ 1,863,768 $ 7,468,399

Weighted average ow nership 31.0% 38.7% 15.0% 31.8%

(A) Includes the unconsolidated co-investment ventures listed on the previous page. (B) Represents the entire entity, not our proportionate share.

Copyright © 2015 Prologis

16

|

|

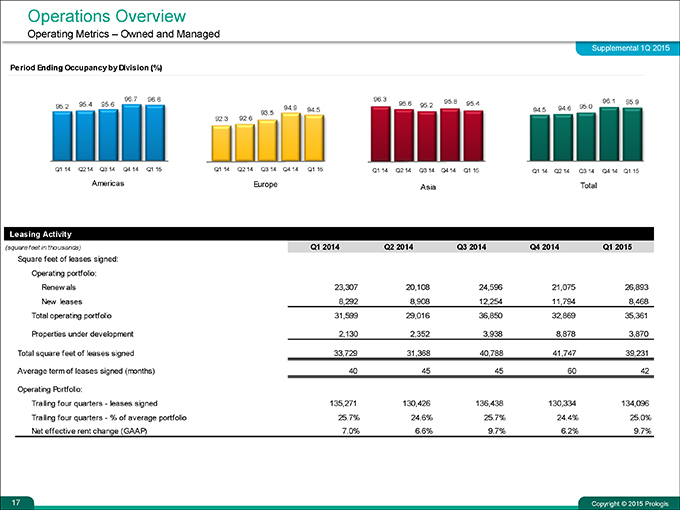

Operations Overview

Operating Metrics – Owned and Managed

Supplemental 1Q 2015

Period Ending Occupancy by Division (%)

Leasing Activity

(square feet in thousands) Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Square feet of leases signed:

Operating portfolio:

Renew als 23,307 20,108 24,596 21,075 26,893

New leases 8,292 8,908 12,254 11,794 8,468

Total operating portfolio 31,599 29,016 36,850 32,869 35,361

Properties under development 2,130 2,352 3,938 8,878 3,870

Total square feet of leases signed 33,729 31,368 40,788 41,747 39,231

Average term of leases signed (months) 40 45 45 60 42

Operating Portfolio:

Trailing four quarters—leases signed 135,271 130,426 136,438 130,334 134,096

Trailing four quarters—% of average portfolio 25.7% 24.6% 25.7% 24.4% 25.0%

Net effective rent change (GAAP) 7.0% 6.6% 9.7% 6.2% 9.7%

Copyright © 2015 Prologis

17

|

|

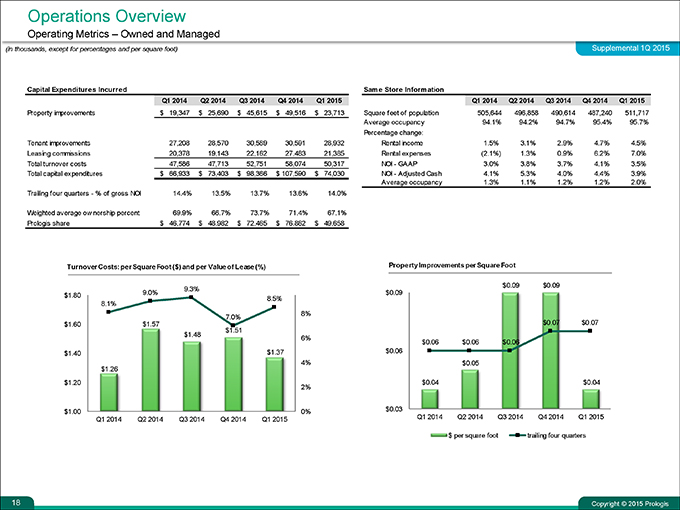

Operations Overview

Operating Metrics – Owned and Managed

(in thousands, except for percentages and per square foot) Supplemental 1Q 2015

Capital Expenditures Incurred

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Property improvements $ 19,347 $ 25,690 $ 45,615 $ 49,516 $ 23,713

Tenant improvements 27,208 28,570 30,589 30,591 28,932

Leasing commissions 20,378 19,143 22,162 27,483 21,385

Total turnover costs 47,586 47,713 52,751 58,074 50,317

Total capital expenditures $ 66,933 $ 73,403 $ 98,366 $ 107,590 $ 74,030

Trailing four quarters—% of gross NOI 14.4% 13.5% 13.7% 13.6% 14.0%

Weighted average ow nership percent 69.9% 66.7% 73.7% 71.4% 67.1%

Prologis share $ 46,774 $ 48,982 $ 72,465 $ 76,862 $ 49,658

Same Store Information

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Square feet of population 505,644 496,858 490,614 487,240 511,717

Average occupancy 94.1% 94.2% 94.7% 95.4% 95.7%

Percentage change:

Rental income 1.5% 3.1% 2.9% 4.7% 4.5%

Rental expenses(2.1%) 1.3% 0.9% 6.2% 7.0%

NOI—GAAP 3.0% 3.8% 3.7% 4.1% 3.5%

NOI—Adjusted Cash 4.1% 5.3% 4.0% 4.4% 3.9%

Average occupancy 1.3% 1.1% 1.2% 1.2% 2.0%

Turnover Costs: per Square Foot ($) and per Value of Lease (%)

Property Improvements per Square Foot

Copyright © 2015 Prologis

18

|

|

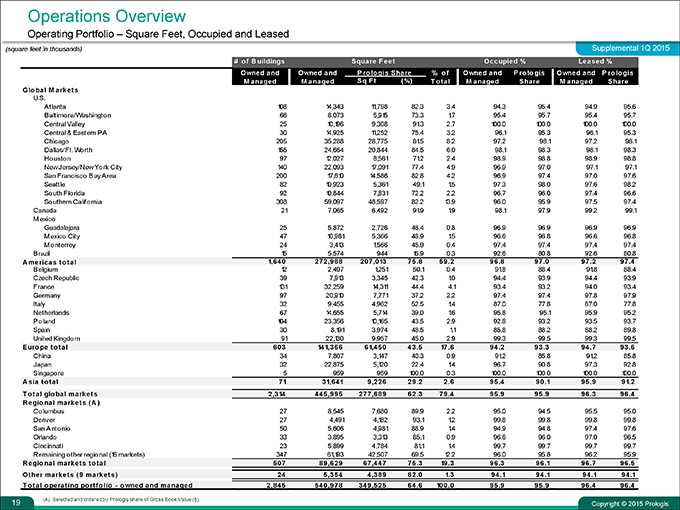

Operations Overview

Operating Portfolio – Square Feet, Occupied and Leased

(square feet in thousands) Supplemental 1Q 2015

# o f B uildings Square F eet Occupied % Leased %

Owned and Owned and P ro lo gis Share% o f Owned and P ro lo gis Owned and P ro lo gis

Managed M anaged Sq F t(%) T o tal M anaged Share M anaged Share

Global M arkets U.S.

Atlanta 108 14,343 11,798 82.3 3.4 94.3 95.4 94.9 95.6

Baltimore/Washington 66 8,073 5,915 73.3 1.7 95.4 95.7 95.4 95.7

Central Valley 25 10,196 9,308 91.3 2.7 100.0 100.0 100.0 100.0

Central & Eastern PA 30 14,925 11,252 75.4 3.2 96.1 95.3 96.1 95.3

Chicago 205 35,288 28,775 81.5 8.2 97.2 98.1 97.2 98.1

Dallas/Ft. Worth 155 24,664 20,844 84.5 6.0 98.1 98.3 98.1 98.3

Houston 97 12,027 8,561 71.2 2.4 98.9 98.8 98.9 98.8

New Jersey/New York City 140 22,093 17,091 77.4 4.9 96.9 97.0 97.1 97.1

San Francisco Bay Area 200 17,610 14,586 82.8 4.2 96.9 97.4 97.0 97.6

Seattle 82 10,923 5,361 49.1 1.5 97.3 98.0 97.6 98.2

South Florida 92 10,844 7,831 72.2 2.2 96.7 96.0 97.4 96.6

Southern California 308 59,097 48,597 82.2 13.9 96.0 95.9 97.5 97.4

Canada 21 7,065 6,492 91.9 1.9 98.1 97.9 99.2 99.1

Mexico Guadalajara 25 5,872 2,726 46.4 0.8 96.9 96.9 96.9 96.9

Mexico City 47 10,981 5,366 48.9 1.5 96.6 96.8 96.6 96.8

Monterrey 24 3,413 1,566 45.9 0.4 97.4 97.4 97.4 97.4

Brazil 15 5,574 944 16.9 0.3 92.6 80.8 92.6 80.8

Americas to tal 1,640 272,988 207,013 75 .8 59 .2 96 .8 97 .0 97 .2 97 .4

Belgium 12 2,497 1,251 50.1 0.4 91.8 88.4 91.8 88.4

Czech Republic 39 7,913 3,345 42.3 1.0 94.4 93.9 94.4 93.9

France 131 32,259 14,311 44.4 4.1 93.4 93.2 94.0 93.4

Germany 97 20,910 7,771 37.2 2.2 97.4 97.4 97.8 97.9

Italy 32 9,455 4,962 52.5 1.4 87.0 77.8 87.0 77.8

Netherlands 67 14,655 5,714 39.0 1.6 95.8 95.1 95.9 95.2

Poland 104 23,356 10,165 43.5 2.9 92.8 93.2 93.5 93.7

Spain 30 8,191 3,974 48.5 1.1 85.8 88.2 88.2 89.8

United Kingdom 91 22,130 9,957 45.0 2.9 99.3 99.5 99.3 99.5

Euro pe to tal 603 141,366 61,450 43 .5 17 .6 94 .2 93 .3 94 .7 93 .6

China 34 7,807 3,147 40.3 0.9 91.2 85.8 91.2 85.8

Japan 32 22,875 5,120 22.4 1.4 96.7 90.8 97.3 92.8

Singapore 5 959 959 100.0 0.3 100.0 100.0 100.0 100.0

Asia to tal 71 31,641 9,226 29 .2 2 .6 95 .4 90 .1 95 .9 91.2

Total global markets 2,314 445,995 277,689 62 .3 79 .4 95 .9 95 .9 96 .3 96 .4

Regional markets(A )

Columbus 27 8,545 7,680 89.9 2.2 95.0 94.5 95.5 95.0

Denver 27 4,491 4,182 93.1 1.2 99.8 99.8 99.8 99.8

San Antonio 50 5,606 4,981 88.9 1.4 94.9 94.8 97.4 97.6

Orlando 33 3,895 3,313 85.1 0.9 96.6 96.0 97.0 96.5

Cincinnati 23 5,899 4,784 81.1 1.4 99.7 99.7 99.7 99.7

Remaining other regional (16 markets) 347 61,193 42,507 69.5 12.2 96.0 95.8 96.2 95.9

Regio nal markets to tal 507 89,629 67,447 75 .3 19 .3 96 .3 96 .1 96 .7 96 .5

Other markets (9 markets) 24 5,354 4,389 82 .0 1.3 94 .1 94 .1 94 .1 94 .1

Total operating po rtfo lio—o wned and managed 2,845 540,978 349,525 64 .6 100 .0 95 .9 95 .9 96 .4 96 .4

(A) Selected and ordered by Prologis share of Gross Book Value ($).

Copyright © 2015 Prologis

19

|

|

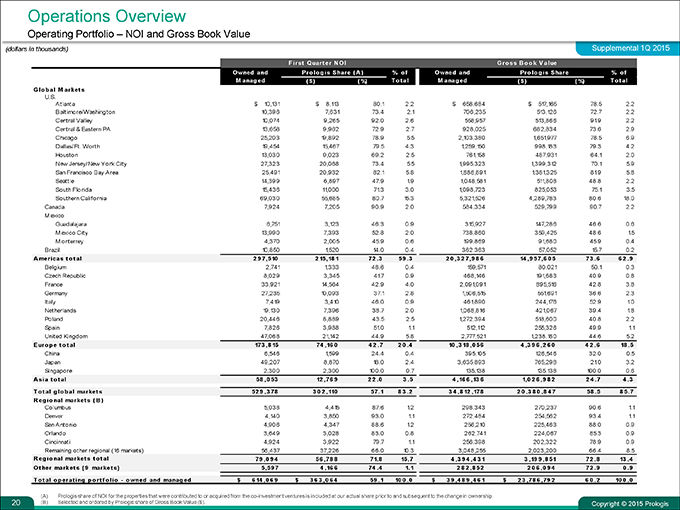

Operations Overview

Operating Portfolio – NOI and Gross Book Value

(dollars in thousands) Supplemental 1Q 2015

F irst Quart er N OI Gro ss B o o k V alue

Owned and Pro lo g is Share ( A )% o f Owned and Pro lo g is Share% o f

Managed( $)( %) Total Managed( $)( %) T o t al

Glob al Markets U.S.

Atlanta $ 10,131 $ 8,113 80.1 2.2 $ 658,684 $ 517,165 78.5 2.2

Baltimore/Washington 10,396 7,631 73.4 2.1 706,235 513,126 72.7 2.2

Central Valley 10,074 9,265 92.0 2.6 558,957 513,866 91.9 2.2

Central & Eastern PA 13,658 9,962 72.9 2.7 928,025 682,834 73.6 2.9

Chicago 25,203 19,892 78.9 5.5 2,103,380 1,651,977 78.5 6.9

Dallas/Ft. Worth 19,454 15,467 79.5 4.3 1,259,150 998,183 79.3 4.2

Houston 13,030 9,023 69.2 2.5 761,158 487,931 64.1 2.0

New Jersey/New York City 27,323 20,068 73.4 5.5 1,995,323 1,399,312 70.1 5.9

San Francisco Bay Area 25,491 20,932 82.1 5.8 1,686,891 1,381,325 81.9 5.8

Seattle 14,399 6,897 47.9 1.9 1,048,581 511,808 48.8 2.2

South Florida 15,436 11,000 71.3 3.0 1,098,723 825,053 75.1 3.5

Southern California 69,030 55,685 80.7 15.3 5,321,526 4,289,783 80.6 18.0

Canada 7,924 7,205 90.9 2.0 584,334 529,799 90.7 2.2

Mexico Guadalajara 6,751 3,123 46.3 0.9 315,927 147,286 46.6 0.6

Mexico City 13,990 7,393 52.8 2.0 738,860 359,425 48.6 1.5

Monterrey 4,370 2,005 45.9 0.6 199,869 91,680 45.9 0.4

Brazil 10,850 1,520 14.0 0.4 362,363 57,052 15.7 0.2

Americas t o t al 2 9 7,510 2 15,18 1 72 .3 59 .3 2 0 ,3 2 7,9 8 6 14 ,9 57,6 0 5 73 .6 6 2 .9

Belgium 2,741 1,333 48.6 0.4 159,571 80,021 50.1 0.3

Czech Republic 8,029 3,345 41.7 0.9 468,146 191,683 40.9 0.8

France 33,921 14,564 42.9 4.0 2,091,091 895,516 42.8 3.8

Germany 27,235 10,093 37.1 2.8 1,506,515 551,691 36.6 2.3

Italy 7,419 3,410 46.0 0.9 461,890 244,176 52.9 1.0

Netherlands 19,130 7,396 38.7 2.0 1,068,816 421,067 39.4 1.8

Poland 20,446 8,889 43.5 2.5 1,272,394 518,600 40.8 2.2

Spain 7,826 3,988 51.0 1.1 512,112 255,326 49.9 1.1

United Kingdom 47,068 21,142 44.9 5.8 2,777,521 1,238,180 44.6 5.2

Europe total 173 ,8 15 74 ,16 0 4 2 .7 2 0 .4 10 ,3 18 ,0 56 4 ,3 9 6 ,2 6 0 4 2 .6 18 .5

China 6,546 1,599 24.4 0.4 395,105 126,546 32.0 0.5

Japan 49,207 8,870 18.0 2.4 3,635,893 765,298 21.0 3.2

Singapore 2,300 2,300 100.0 0.7 135,138 135,138 100.0 0.6

Asia tot al 58 ,0 53 12 ,76 9 2 2 .0 3 .5 4 ,16 6 ,13 6 1,0 2 6 ,9 8 2 2 4 .7 4 .3

Total global market s 52 9 ,3 78 3 0 2 ,110 57.1 8 3 .2 3 4 ,8 12 ,178 2 0 ,3 8 0 ,8 4 7 58 .5 8 5.7

Regional markets ( B )

Columbus 5,038 4,415 87.6 1.2 298,343 270,237 90.6 1.1

Denver 4,140 3,850 93.0 1.1 272,484 254,562 93.4 1.1

San Antonio 4,906 4,347 88.6 1.2 256,210 225,463 88.0 0.9

Orlando 3,649 3,028 83.0 0.8 262,741 224,067 85.3 0.9

Cincinnati 4,924 3,922 79.7 1.1 256,398 202,322 78.9 0.9

Remaining other regional (16 markets) 56,437 37,226 66.0 10.3 3,048,255 2,023,200 66.4 8.5

Regional markets total 79 ,0 9 4 56 ,78 8 71.8 15.7 4 ,3 9 4 ,4 3 1 3 ,19 9 ,8 51 72 .8 13 .4

Other markets ( 9 market s) 5,59 7 4 ,16 6 74 .4 1.1 2 8 2 ,8 52 2 0 6 ,0 9 4 72 .9 0 .9

Total operating portfolio—owned and managed $ 6 14 ,0 6 9 $ 3 6 3 ,0 6 4 59 .1 10 0 .0 $ 3 9 ,4 8 9 ,4 6 1 $ 2 3 ,78 6 ,79 2 6 0 .2 10 0 .0

(A) Prologis share of NOI for the properties that were contributed to or acquired from the co-investment ventures is included at our actual share prior to and subsequent to the change in ownership.

(B) Selected and ordered by Prologis share of Gross Book Value ($).

Copyright © 2015 Prologis

20

|

|

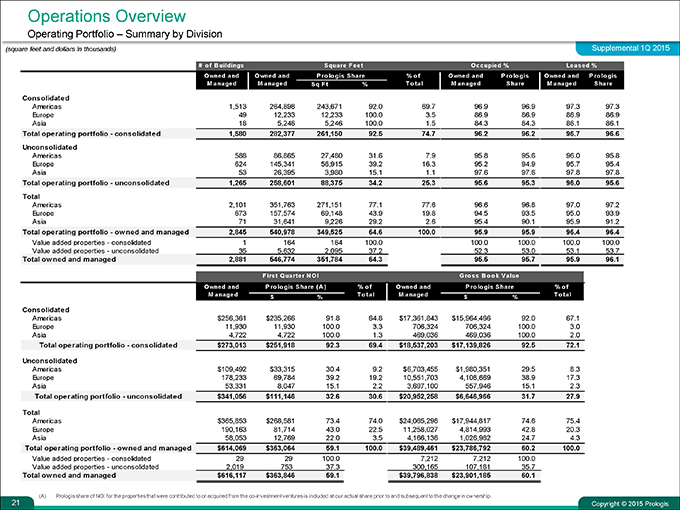

Operations Overview

Operating Portfolio – Summary by Division

(square feet and dollars in thousands) Supplemental 1Q 2015

# of Buildings Square Feet Occupied % Leased %

Owned and Owned and Prologis Share% o f Owned and Prologis Owned and Prologis

Managed Managed Sq Ft% Total Managed Share Managed Share

Consolidated Americas 1,513 264,898 243,671 92.0 69.7 96.9 96.9 97.3 97.3

Europe 49 12,233 12,233 100.0 3.5 86.9 86.9 86.9 86.9

Asia 18 5,246 5,246 100.0 1.5 84.3 84.3 86.1 86.1

Total operating portfolio—consolidated 1,580 282,377 261,150 92.5 74.7 96.2 96.2 96.7 96.6

Unconsolidated Americas 588 86,865 27,480 31.6 7.9 95.8 95.6 96.0 95.8

Europe 624 145,341 56,915 39.2 16.3 95.2 94.9 95.7 95.4

Asia 53 26,395 3,980 15.1 1.1 97.6 97.6 97.8 97.8

Total operating portfolio—unconsolidated 1,265 258,601 88,375 34.2 25.3 95.6 95.3 96.0 95.6

Total Americas 2,101 351,763 271,151 77.1 77.6 96.6 96.8 97.0 97.2

Europe 673 157,574 69,148 43.9 19.8 94.5 93.5 95.0 93.9

Asia 71 31,641 9,226 29.2 2.6 95.4 90.1 95.9 91.2

Total operating portfolio—owned and managed 2,845 540,978 349,525 64.6 100.0 95.9 95.9 96.4 96.4

Value added properties—consolidated 1 164 164 100.0 100.0 100.0 100.0 100.0

Value added properties—unconsolidated 35 5,632 2,095 37.2 52.3 53.0 53.1 53.7

Total ow ned and managed 2,881 546,774 351,784 64.3 95.5 95.7 95.9 96.1

F irst Quarter N OI Gross Book Value

Owned and Prologis Share (A)% of Owned and Prologis Share% o f

Managed Total Managed Total

$% $% Consolidated

Americas $256,361 $235,266 91.8 64.8 $17,361,843 $15,964,466 92.0 67.1

Europe 11,930 11,930 100.0 3.3 706,324 706,324 100.0 3.0

Asia 4,722 4,722 100.0 1.3 469,036 469,036 100.0 2.0

Total operating portfolio—consolidated $273,013 $251,918 92.3 69.4 $18,537,203 $17,139,826 92.5 72.1

Unconsolidated Americas $109,492 $33,315 30.4 9.2 $6,703,455 $1,980,351 29.5 8.3

Europe 178,233 69,784 39.2 19.2 10,551,703 4,108,669 38.9 17.3

Asia 53,331 8,047 15.1 2.2 3,697,100 557,946 15.1 2.3

Total operating portfolio—unconsolidated $341,056 $111,146 32.6 30.6 $20,952,258 $6,646,966 31.7 27.9

Total Americas $365,853 $268,581 73.4 74.0 $24,065,298 $17,944,817 74.6 75.4

Europe 190,163 81,714 43.0 22.5 11,258,027 4,814,993 42.8 20.3

Asia 58,053 12,769 22.0 3.5 4,166,136 1,026,982 24.7 4.3

Total operating portfolio—ow ned and managed $614,069 $363,064 59.1 100.0 $39,489,461 $23,786,792 60.2 100.0 Value added properties—consolidated 29 29 100.0 7,212 7,212 100.0

Value added properties—unconsolidated 2,019 753 37.3 300,165 107,181 35.7

Total ow ned and managed $616,117 $363,846 59.1 $39,796,838 $23,901,185 60.1

(A) Prologis share of NOI for the properties that were contributed to or acquired from the co-investment ventures is included at our actual share prior to and subsequent to the change in ownership.

Copyright © 2015 Prologis

21

|

|

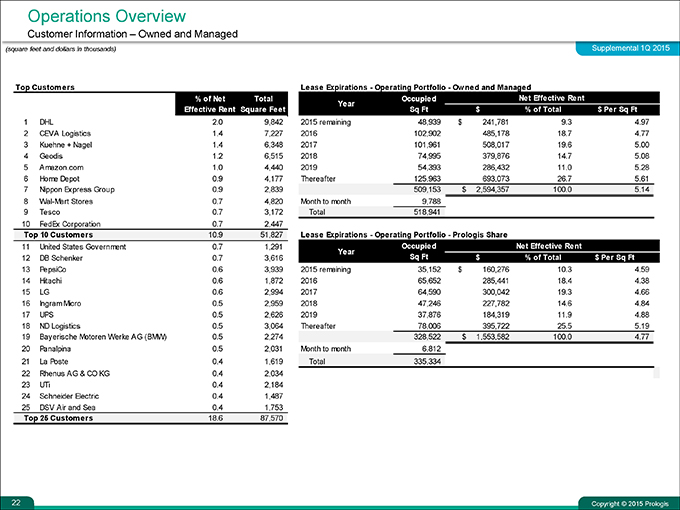

Operations Overview

Customer Information – Owned and Managed

(square feet and dollars in thousands) Supplemental 1Q 2015

Top Customers % of Net Total

Effective Rent Square Feet

1 DHL 2.0 9,842

2 CEVA Logistics 1.4 7,227

3 Kuehne + Nagel 1.4 6,348

4 Geodis 1.2 6,515

5 Amazon.com 1.0 4,440

6 Home Depot 0.9 4,177

7 Nippon Express Group 0.9 2,839

8 Wal-Mart Stores 0.7 4,820

9 Tesco 0.7 3,172

10 FedEx Corporation 0.7 2,447

Top 10 Customers 10.9 51,827

11 United States Government 0.7 1,291

12 DB Schenker 0.7 3,616

13 PepsiCo 0.6 3,939

14 Hitachi 0.6 1,872

15 LG 0.6 2,994

16 Ingram Micro 0.5 2,959

17 UPS 0.5 2,626

18 ND Logistics 0.5 3,064

19 Bayerische Motoren Werke AG (BMW) 0.5 2,274

20 Panalpina 0.5 2,031

21 La Poste 0.4 1,619

22 Rhenus AG & CO KG 0.4 2,034

23 UTi 0.4 2,184

24 Schneider Electric 0.4 1,487

25 DSV Air and Sea 0.4 1,753

Top 25 Customers 18.6 87,570

Lease Expirations—Operating Portfolio—Ow ned and Managed

Year Occupied Net Effective Rent

Sq Ft $% of Total $ Per Sq Ft

2015 remaining 48,939 $ 241,781 9.3 4.97

2016 102,902 485,178 18.7 4.77

2017 101,961 508,017 19.6 5.00

2018 74,995 379,876 14.7 5.08

2019 54,393 286,432 11.0 5.28

Thereafter 125,963 693,073 26.7 5.61

509,153 $ 2,594,357 100.0 5.14

Month to month 9,788 Total 518,941

Lease Expirations—Operating Portfolio—Prologis Share

Occupied Net Effective Rent

Year Sq Ft $% of Total $ Per Sq Ft

2015 remaining 35,152 $ 160,276 10.3 4.59

2016 65,652 285,441 18.4 4.38

2017 64,590 300,042 19.3 4.66

2018 47,246 227,782 14.6 4.84

2019 37,876 184,319 11.9 4.88

Thereafter 78,006 395,722 25.5 5.19

328,522 $ 1,553,582 100.0 4.77

Month to month 6,812 Total 335,334

Copyright © 2015 Prologis

22

|

|

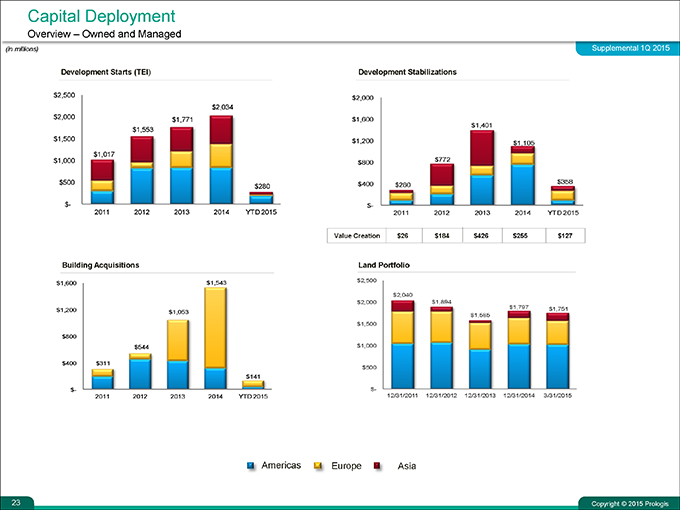

Capital Deployment

Overview – Owned and Managed

(in millions) Supplemental 1Q 2015

Development Starts (TEI) Development Stabilizations

Building Acquisitions Land Portfolio

Copyright © 2015 Prologis

23

|

|

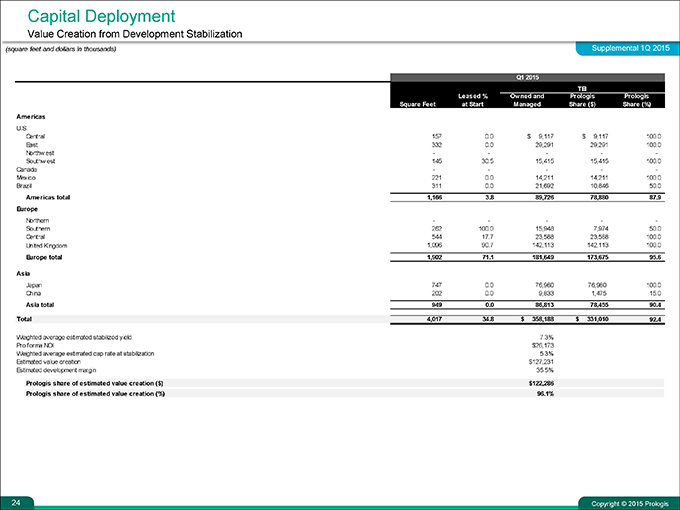

Capital Deployment

Value Creation from Development Stabilization

(square feet and dollars in thousands) Supplemental 1Q 2015

Q1 2015

TEI

Leased % Owned and Prologis Prologis

Square Feet at Start Managed Share ($) Share (%)

Americas

U.S.

Central 157 0.0 $ 9,117 $ 9,117 100.0

East 332 0.0 29,291 29,291 100.0

Northwest

Southwest 145 30.5 15,415 15,415 100.0

Canada

Mexico 221 0.0 14,211 14,211 100.0

Brazil 311 0.0 21,692 10,846 50.0

Americas total 1,166 3.8 89,726 78,880 87.9

Europe

Northern

Southern 262 100.0 15,948 7,974 50.0

Central 544 17.7 23,588 23,588 100.0

United Kingdom 1,096 90.7 142,113 142,113 100.0

Europe total 1,902 71.1 181,649 173,675 95.6

Asia

Japan 747 0.0 76,980 76,980 100.0

China 202 0.0 9,833 1,475 15.0

Asia total 949 0.0 86,813 78,455 90.4

Total 4,017 34.8 $ 358,188 $ 331,010 92.4

Weighted average estimated stabilized yield 7.3%

Pro forma NOI $26,173

Weighted average estimated cap rate at stabilization 5.3%

Estimated value creation $127,231

Estimated development margin 35.5%

Prologis share of estimated value creation ($) $122,286

Prologis share of estimated value creation (%) 96.1%

Copyright © 2015 Prologis

24

|

|

Capital Deployment

Development Starts

(square feet and dollars in thousands) Supplemental 1Q 2015

Q1 2015

TEI

Leased % at Owned and Prologis Share Prologis

Square Feet Start Managed($) Share (%)

Americas

U.S.

Central 1,080 38.1 $ 64,880 $ 64,880 100.0

East

Northw est 647 0.0 63,577 63,577 100.0

Southw est 835 0.0 65,053 65,053 100.0

Canada

Mexico

Brazil

Americas total 2,562 16.1 193,510 193,510 100.0

Europe

Northern 287 100.0 14,752 4,597 31.2

Southern

Central 298 68.8 11,145 11,145 100.0

United Kingdom

Europe total 585 84.1 25,897 15,742 60.8

Asia

Japan

China 957 0.0 60,738 9,111 15.0

Asia total 957 0.0 60,738 9,111 15.0

Total 4,104 22.0 $ 280,145 $ 218,363 77.9

Weighted average estimated stabilized yield 7.1%

Pro forma NOI $19,803

Weighted average estimated cap rate at stabilization 5.9%

Estimated value creation $57,505

Estimated development margin 20.5%

Prologis share of estimated value creation ($) $46,039

Prologis share of estimated value creation (%) 80.1%

% BTS (based on Prologis share) 16.5%

Copyright © 2015 Prologis

25

|

|

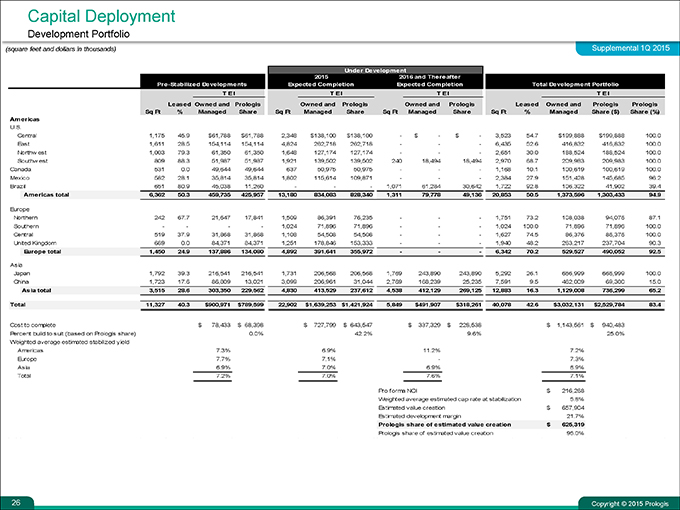

Capital Deployment

Development Portfolio

(square feet and dollars in thousands) Supplemental 1Q 2015

Under Development

2015 2016 and Thereafter

Pre-Stabilized Developments Expected Completion Expected Completion Total Development Portfolio

T E I T E I T E I T E I

Leased Owned and Prologis Owned and Prologis Owned and Prologis Leased Owned and Prologis Prologis

Sq Ft% Managed Share Sq Ft Managed Share Sq Ft Managed Share Sq Ft% Managed Share ($) Share (%)

Americas U.S.

Central 1,175 45.9 $61,788 $61,788 2,348 $138,100 $138,100—$—$—3,523 54.7 $199,888 $199,888 100.0

East 1,611 28.5 154,114 154,114 4,824 262,718 262,718 ——6,435 52.6 416,832 416,832 100.0

Northwest 1,003 79.3 61,350 61,350 1,648 127,174 127,174 ——2,651 30.0 188,524 188,524 100.0

Southwest 809 88.3 51,987 51,987 1,921 139,502 139,502 240 18,494 18,494 2,970 68.7 209,983 209,983 100.0

Canada 531 0.0 49,644 49,644 637 50,975 50,975 ——1,168 10.1 100,619 100,619 100.0

Mexico 582 28.1 35,814 35,814 1,802 115,614 109,871 ——2,384 27.9 151,428 145,685 96.2

Brazil 651 80.9 45,038 11,260 ——1,071 61,284 30,642 1,722 92.8 106,322 41,902 39.4

Americas total 6,362 50.3 459,735 425,957 13,180 834,083 828,340 1,311 79,778 49,136 20,853 50.5 1,373,596 1,303,433 94.9 Europe

Northern 242 67.7 21,647 17,841 1,509 86,391 76,235 ——1,751 73.2 108,038 94,076 87.1

Southern — — 1,024 71,896 71,896 ——1,024 100.0 71,896 71,896 100.0

Central 519 37.9 31,868 31,868 1,108 54,508 54,508 ——1,627 74.5 86,376 86,376 100.0

United Kingdom 689 0.0 84,371 84,371 1,251 178,846 153,333 ——1,940 48.2 263,217 237,704 90.3

Europe total 1,450 24.9 137,886 134,080 4,892 391,641 355,972 ——6,342 70.2 529,527 490,052 92.5

Asia Japan 1,792 39.3 216,541 216,541 1,731 206,568 206,568 1,769 243,890 243,890 5,292 26.1 666,999 666,999 100.0

China 1,723 17.6 86,809 13,021 3,099 206,961 31,044 2,769 168,239 25,235 7,591 9.5 462,009 69,300 15.0

Asia total 3,515 28.6 303,350 229,562 4,830 413,529 237,612 4,538 412,129 269,125 12,883 16.3 1,129,008 736,299 65.2

Total 11,327 40.3 $900,971 $789,599 22,902 $1,639,253 $1,421,924 5,849 $491,907 $318,261 40,078 42.6 $3,032,131 $2,529,784 83.4

Cost to complete $ 78,433 $ 68,398 $ 727,799 $ 643,547 $ 337,329 $ 228,538 $ 1,143,561 $ 940,483

Percent build to suit (based on Prologis share) 0.0% 42.2% 9.6% 25.0%

Weighted average estimated stabilized yield

Americas 7.3% 6.9% 11.2% 7.2%

Europe 7.7% 7.1%—7.3%

Asia 6.9% 7.0% 6.9% 6.9%

Total 7.2% 7.0% 7.6% 7.1%

Pro forma NOI $ 216,268

Weighted average estimated cap rate at stabilization 5.8%

Estimated value creation $ 657,904

Estimated development margin 21.7%

Prologis share of estim ated value creation $ 625,319

Prologis share of estimated value creation 95.0%

Copyright © 2015 Prologis

26

|

|

Capital Deployment

Third Party Building Acquisitions

(square feet and dollars in thousands) Supplemental 1Q 2015

Q1 2015

Square Prologis Share Owned and Managed Prologis Share Prologis Share

Feet of Square Feet Acquisition Cost of Acquisition of Acquisition

Cost ($) Cost (%)

Third Party Building Acquisitions

Americas

Prologis wholly ow ned 181 181 $ 21,132 $ 21,132 100.0

Prologis Targeted U.S. Logistics Fund 168 41 22,898 5,578 24.4

Total Americas 349 222 44,030 26,710 60.7

Europe

Prologis Targeted Europe Logistics Fund 747 322 27,938 12,021 43.0

Prologis European Properties Fund II 1,306 405 68,971 21,489 31.2

Total Europe 2,053 727 96,909 33,510 34.6

Total Third Party Building Acquisitions 2,402 949 $ 140,939 $ 60,220 42.7

Weighted average stabilized cap rate 6.8%

Copyright © 2015 Prologis

27

|

|

Capital Deployment

Dispositions and Contributions

(square feet and dollars in thousands) Supplemental 1Q 2015

Q1 2015

Prologis Ow ned and Prologis Share of

Square Prologis Share

Share of Managed Total Proceeds

Feet of Proceeds ($)

Square Feet Proceeds(%) (A)

Third Party Building Dispositions

Americas

Prologis w holly ow ned (B) 2,359 2,359 $ 455,424 $ 455,424 100.0

Prologis North American Industrial Fund 334 221 9,307 6,156 66.1

Total Americas 2,693 2,580 464,731 461,580 99.3

Europe

Total Europe

Asia

Total Asia

Total Third Party Building Dispositions 2,693 2,580 $ 464,731 $ 461,580 99.3

Building Contributions to Co-Investm ent Ventures

Americas

Total Americas

Europe

ProLogis European Properties Fund II 507 507 $ 29,643 $ 20,407 68.8

Total Europe 507 507 29,643 20,407 68.8

Asia

Total Asia

Total Contributions to Co-Investment Ventures 507 507 $ 29,643 $ 20,407 68.8

Total Building Dispositions and Contributions 3,200 3,087 $ 494,374 $ 481,987 97.5

Land dispositions 24,841 21,318 85.8

Other real estate dispositions 14,797 14,797 100.0

Grand Total Dispositions and Contributions $ 534,012 $ 518,102 97.0

Weighted average stabilized cap rate on building dispositions and contributions 3.6%

(A) For contributions, this amount reflects total proceeds to Prologis, net of units received for partial consideration. (B) Activity in the first quarter of 2015 includes a previous announced sale under our value added conversion program.

Copyright © 2015 Prologis

28

|

|

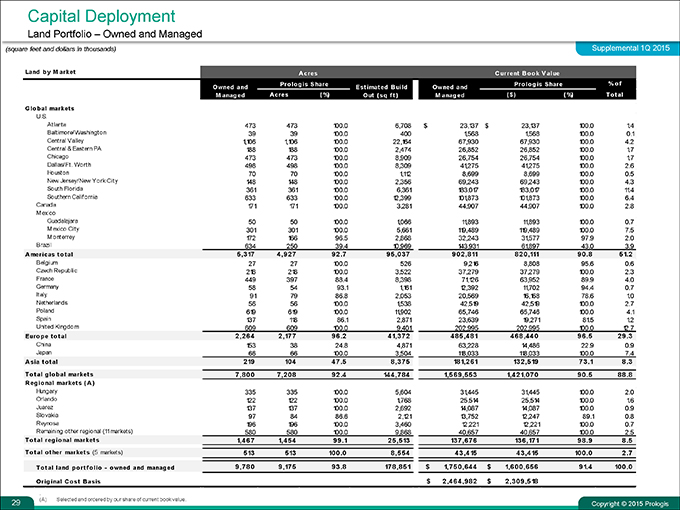

Capital Deployment

Land Portfolio – Owned and Managed

(square feet and dollars in thousands) Supplemental 1Q 2015

Land by Market Acres Current Book Value

Prolog is Share Prolog is Share% o f

Owned and Est imat ed B uild Owned and

Managed Acres(%) Out (sq ft) Managed($)( %) Total

Global markets

U.S.

Atlanta 473 473 100.0 6,708 $ 23,137 $ 23,137 100.0 1.4

Baltimore/Washington 39 39 100.0 400 1,568 1,568 100.0 0.1

Central Valley 1,106 1,106 100.0 22,164 67,930 67,930 100.0 4.2

Central & Eastern PA 188 188 100.0 2,474 26,852 26,852 100.0 1.7

Chicago 473 473 100.0 8,909 26,754 26,754 100.0 1.7

Dallas/Ft. Worth 498 498 100.0 8,309 41,275 41,275 100.0 2.6

Houston 70 70 100.0 1,112 8,699 8,699 100.0 0.5

New Jersey/New York City 148 148 100.0 2,356 69,243 69,243 100.0 4.3

South Florida 361 361 100.0 6,361 183,017 183,017 100.0 11.4

Southern California 633 633 100.0 12,399 101,873 101,873 100.0 6.4

Canada 171 171 100.0 3,281 44,907 44,907 100.0 2.8

Mexico

Guadalajara 50 50 100.0 1,066 11,893 11,893 100.0 0.7

Mexico City 301 301 100.0 5,661 119,489 119,489 100.0 7.5

Monterrey 172 166 96.5 2,868 32,243 31,577 97.9 2.0

Brazil 634 250 39.4 10,969 143,931 61,897 43.0 3.9

Americas t o t al 5,317 4,927 92 .7 95,037 902,811 820,111 90 .8 51.2

Belgium 27 27 100.0 526 9,216 8,808 95.6 0.6

Czech Republic 218 218 100.0 3,522 37,279 37,279 100.0 2.3

France 449 397 88.4 8,398 71,126 63,952 89.9 4.0

Germany 58 54 93.1 1,161 12,392 11,702 94.4 0.7

Italy 91 79 86.8 2,053 20,569 16,168 78.6 1.0

Netherlands 56 56 100.0 1,538 42,519 42,519 100.0 2.7

Poland 619 619 100.0 11,902 65,746 65,746 100.0 4.1

Spain 137 118 86.1 2,871 23,639 19,271 81.5 1.2

United Kingdom 609 609 100.0 9,401 202,995 202,995 100.0 12.7

Euro p e t o t al 2,264 2,177 96 .2 41,372 485,481 468,440 96 .5 29 .3

China 153 38 24.8 4,871 63,228 14,486 22.9 0.9

Japan 66 66 100.0 3,504 118,033 118,033 100.0 7.4

Asia total 219 104 47 .5 8,375 181,261 132,519 73 .1 8 .3

Total global market s 7,800 7,208 92 .4 144,784 1,569,553 1,421,070 90 .5 88 .8

Regional markets (A)

Hungary 335 335 100.0 5,604 31,445 31,445 100.0 2.0

Orlando 122 122 100.0 1,768 25,514 25,514 100.0 1.6

Juarez 137 137 100.0 2,692 14,087 14,087 100.0 0.9

Slovakia 97 84 86.6 2,121 13,752 12,247 89.1 0.8

Reynosa 196 196 100.0 3,460 12,221 12,221 100.0 0.7

Remaining other regional (11markets) 580 580 100.0 9,868 40,657 40,657 100.0 2.5

Total regional markets 1,467 1,454 99 .1 25,513 137,676 136,171 98 .9 8 .5

Total ot her markets (5 markets) 513 513 100 .0 8,554 43,415 43,415 100 .0 2 .7

Total land port folio—owned and managed 9,780 9,175 93 .8 178,851 $ 1,750,644 $ 1,600,656 91.4 100 .0

Original Cost Basis $ 2,464,982 $ 2,309,518

(A) Selected and ordered by our share of current book value.

Copyright © 2015 Prologis

29

|

|

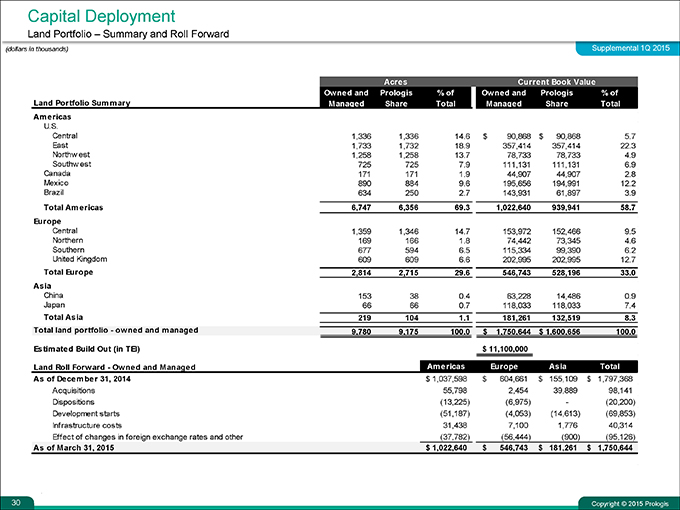

Capital Deployment

Land Portfolio – Summary and Roll Forward

(dollars in thousands) Supplemental 1Q 2015

Acres Current Book Value

Owned and Prologis % of Owned and Prologis % of

Land Portfolio Summary Managed Share Total Managed Share Total

Americas U.S.

Central 1,336 1,336 14.6 $ 90,868 $ 90,868 5.7

East 1,733 1,732 18.9 357,414 357,414 22.3

Northwest 1,258 1,258 13.7 78,733 78,733 4.9

Southwest 725 725 7.9 111,131 111,131 6.9

Canada 171 171 1.9 44,907 44,907 2.8

Mexico 890 884 9.6 195,656 194,991 12.2

Brazil 634 250 2.7 143,931 61,897 3.9

Total Americas 6,747 6,356 69.3 1,022,640 939,941 58.7

Europe

Central 1,359 1,346 14.7 153,972 152,466 9.5

Northern 169 166 1.8 74,442 73,345 4.6

Southern 677 594 6.5 115,334 99,390 6.2

United Kingdom 609 609 6.6 202,995 202,995 12.7

Total Europe 2,814 2,715 29.6 546,743 528,196 33.0

Asia

China 153 38 0.4 63,228 14,486 0.9

Japan 66 66 0.7 118,033 118,033 7.4

Total Asia 219 104 1.1 181,261 132,519 8.3

Total land portfolio—ow ned and managed 9,780 9,175 100.0 $ 1,750,644 $ 1,600,656 100.0

Estimated Build Out (in TEI) $ 11,100,000

Land Roll Forw ard—Ow ned and Managed Americas Europe Asia Total

As of December 31, 2014 $ 1,037,598 $ 604,661 $ 155,109 $ 1,797,368

Acquisitions 55,798 2,454 39,889 98,141

Dispositions(13,225)(6,975) -(20,200)

Development starts(51,187)(4,053)(14,613)(69,853)

Infrastructure costs 31,438 7,100 1,776 40,314

Effect of changes in foreign exchange rates and other(37,782)(56,444)(900)(95,126)

As of March 31, 2015 $ 1,022,640 $ 546,743 $ 181,261 $ 1,750,644

Copyright © 2015 Prologis

30

|

|

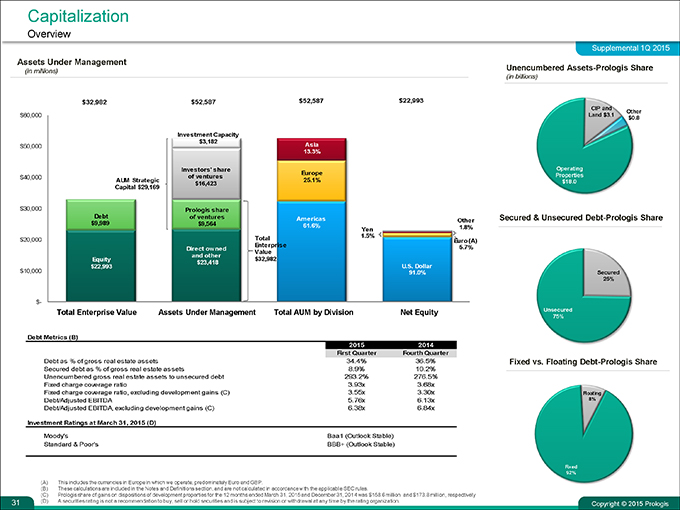

Capitalization Overview Supplemental 1Q 2015

Assets Under Management (in millions)

Debt Metrics (B) 2015 2014

First Quarter Fourth Quarter

Debt as % of gross real estate assets 34.4% 36.5%

Secured debt as % of gross real estate assets 8.9% 10.2%

Unencumbered gross real estate assets to unsecured debt 293.2% 276.5%

Fixed charge coverage ratio 3.93x 3.68x

Fixed charge coverage ratio, excluding development gains (C) 3.55x 3.30x

Debt/Adjusted EBITDA 5.76x 6.13x

Debt/Adjusted EBITDA, excluding development gains (C) 6.38x 6.84x

Investment Ratings at March 31, 2015 (D)

Moody’s Baa1 (Outlook Stable)

Standard & Poor’s BBB+ (Outlook Stable)

Unencumbered Assets-Prologis Share (in billions)

Secured & Unsecured Debt-Prologis Share

Fixed vs. Floating Debt-Prologis Share

(A) This includes the currencies in Europe in which we operate, predominately Euro and GBP.

(B) These calculations are included in the Notes and Definitions section, and are not calculated in accordance with the applicable SEC rules.

(C) Prologis share of gains on dispositions of development properties for the 12 months ended March 31, 2015 and December 31, 2014 was $158.6 million and $173.8 million, respectively

(D) A securities rating is not a recommendation to buy, sell or hold securities and is subject to revision or withdrawal at any time by the rating organization.

Copyright © 2015 Prologis

31

|

|

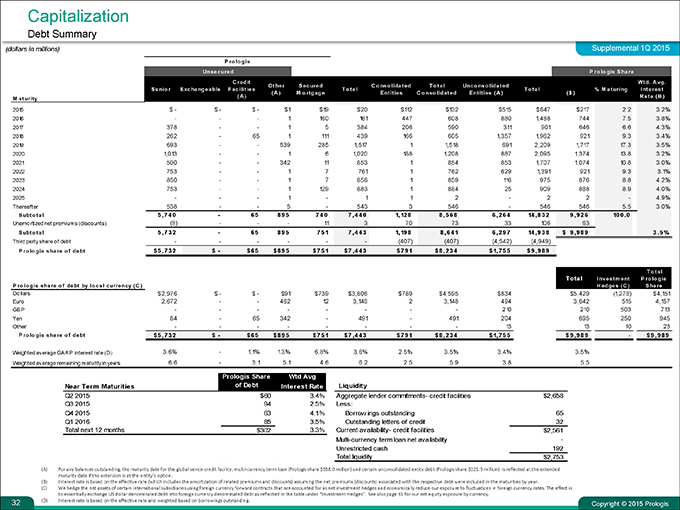

Capitalization Debt Summary

(dollars in millions) Supplemental 1Q 2015 Prologis

Unsecured Prologis Share Credit Wtd. A vg.

Other Secured C o nso lidated T o tal Unco nso lidated

Senio r Exchangeable F acilities T o tal T o tal% M aturing Interest

(A) Mortgage Entities Consolidated Entities (A)($) Maturity(A) Rate (B)

2015 $—$—$—$1 $19 $20 $112 $132 $515 $647 $217 2.2 3.2%

2016 ——1 160 161 447 608 880 1,488 744 7.5 3.8%

2017 378 — 1 5 384 206 590 311 901 646 6.6 4.3%

2018 262—65 1 111 439 166 605 1,357 1,962 921 9.3 3.4%

2019 693 — 539 285 1,517 1 1,518 691 2,209 1,717 17.3 3.5%

2020 1,013 — 1 6 1,020 188 1,208 887 2,095 1,374 13.8 3.2%

2021 500 — 342 11 853 1 854 853 1,707 1,074 10.8 3.0%

2022 753 — 1 7 761 1 762 629 1,391 921 9.3 3.1%

2023 850 — 1 7 858 1 859 116 975 876 8.8 4.2%

2024 753 — 1 129 883 1 884 25 909 888 8.9 4.0%

2025 ——1—1 1 2—2 2—4.9%

Thereafter 538 — 5—543 3 546—546 546 5.5 3.0%

Subtotal 5 ,7 4 0—6 5 8 9 5 7 4 0 7 ,4 4 0 1,12 8 8 ,5 6 8 6 ,2 6 4 14 ,8 3 2 9 ,9 2 6 10 0 . 0

Unamortized net premiums (discounts)(8) ——11 3 70 73 33 106 63

Subtotal 5 ,7 3 2—6 5 8 9 5 7 5 1 7 ,4 4 3 1,19 8 8 ,6 4 1 6 ,2 9 7 14 ,9 3 8 $ 9 ,9 8 9 3 . 5 %

Third party share of debt — — —(407) (407) (4,542) (4,949)

Prologis share o f debt $ 5 ,7 3 2 $—$ 6 5 $ 8 9 5 $ 7 5 1 $ 7 ,4 4 3 $ 7 9 1 $ 8 ,2 3 4 $ 1,7 5 5 $ 9 ,9 8 9

Total Total Investment Prologis

Prologis share o f debt by local currency (C) Hedges (C) Share

Dollars $2,976 $—$—$91 $739 $3,806 $789 $4,595 $834 $5,429(1,278) $4,151

Euro 2,672 — 462 12 3,146 2 3,148 494 3,642 515 4,157

GBP — — — — 210 210 503 713

Yen 84—65 342—491—491 204 695 250 945

Other — — — — 13 13 10 23

Prologis share o f debt $ 5,732 $—$ 65 $ 895 $ 751 $ 7,443 $ 791 $ 8,234 $ 1,755 $ 9 ,989—$ 9,98 9

Weighted average GAAP interest rate (D) 3.6%—1.1% 1.3% 6.8% 3.6% 2.5% 3.5% 3.4% 3.5%

Weighted average remaining maturity in years 6.6—3.1 5.1 4.6 6.2 2.5 5.9 3.8 5.5

Prologis Share Wtd Avg Near Term Maturities of Debt Interest Rate Liquidity

Q2 2015 $60 3.4% Aggregate lender commitments- credit facilities $2,658

Q3 2015 94 2.5% Less: Q4 2015 63 4.1% Borrow ings outstanding 65

Q1 2016 85 3.5% Outstanding letters of credit 32

Total next 12 months $302 3.3% Current availability- credit facilities $2,561

Multi-currency term loan net availability -

Unrestricted cash 192 Total liquidity $2,753

(A) For any balances outstanding, the maturity date for the global senior credit facility, multi-currency term loan (Prologis share $538.0 million) and certain unconsolidated entity debt (Prologis share $221.5 million) is reflected at the extended maturity date if the extension is at the entity’s option.

(B) Interest rate is based on the effective rate (which includes the amortization of related premiums and discounts) assuming the net premiums (discounts) associated with the respective debt were included in the maturities by year.

(C) We hedge the net assets of certain international subsidiaries using foreign currency forward contracts that are accounted for as net investment hedges and economically reduce our exposure to fluctuations in foreign currency rates. The effect is to essentially exchange US dollar denominated debt into foreign currency denominated debt as reflected in the table under “Investment Hedges”. See also page 31 for our net equity exposure by currency.

(D) Interest rate is based on the effective rate and weighted based on borrowings outstanding.

Copyright © 2015 Prologis

32

|

|

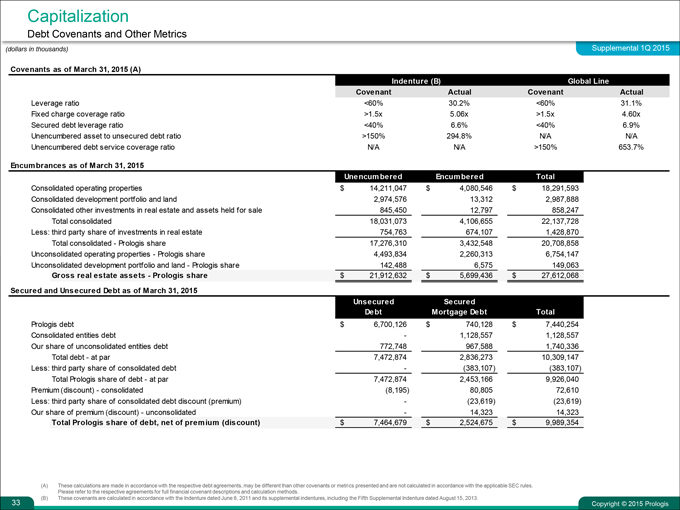

Capitalization

Debt Covenants and Other Metrics

(dollars in thousands) Supplemental 1Q 2015

Covenants as of March 31, 2015 (A)

Indenture (B) Global Line

Covenant Actual Covenant Actual

Leverage ratio <60% 30.2% <60% 31.1% Fixed charge coverage ratio >1.5x 5.06x >1.5x 4.60x Secured debt leverage ratio <40% 6.6% <40% 6.9% Unencumbered asset to unsecured debt ratio >150% 294.8% N/A N/A Unencumbered debt service coverage ratio N/A N/A >150% 653.7%

Encumbrances as of March 31, 2015

Unencumbered Encumbered Total

Consolidated operating properties $ 14,211,047 $ 4,080,546 $ 18,291,593 Consolidated development portfolio and land 2,974,576 13,312 2,987,888 Consolidated other investments in real estate and assets held for sale 845,450 12,797 858,247 Total consolidated 18,031,073 4,106,655 22,137,728 Less: third party share of investments in real estate 754,763 674,107 1,428,870 Total consolidated - Prologis share 17,276,310 3,432,548 20,708,858 Unconsolidated operating properties - Prologis share 4,493,834 2,260,313 6,754,147 Unconsolidated development portfolio and land - Prologis share 142,488 6,575 149,063 Gross real estate assets - Prologis share $ 21,912,632 $ 5,699,436 $ 27,612,068

Secured and Unsecured Debt as of March 31, 2015

Unsecured Secured

Debt Mortgage Debt Total

Prologis debt $ 6,700,126 $ 740,128 $ 7,440,254 Consolidated entities debt - 1,128,557 1,128,557 Our share of unconsolidated entities debt 772,748 967,588 1,740,336 Total debt - at par 7,472,874 2,836,273 10,309,147 Less: third party share of consolidated debt - (383,107) (383,107) Total Prologis share of debt - at par 7,472,874 2,453,166 9,926,040 Premium (discount) - consolidated (8,195) 80,805 72,610 Less: third party share of consolidated debt discount (premium) - (23,619) (23,619) Our share of premium (discount) - unconsolidated - 14,323 14,323

Total Prologis share of debt, net of premium (discount) $ 7,464,679 $ 2,524,675 $ 9,989,354

(A) These calculations are made in accordance with the respective debt agreements, may be different than other covenants or metrics presented and are not calculated in accordance with the applicable SEC rules. Please refer to the respective agreements for full financial covenant descriptions and calculation methods.

(B) These covenants are calculated in accordance with the Indenture dated June 8, 2011 and its supplemental indentures, including the Fifth Supplemental Indenture dated August 15, 2013.

33 Copyright © 2015 Prologis

|

|

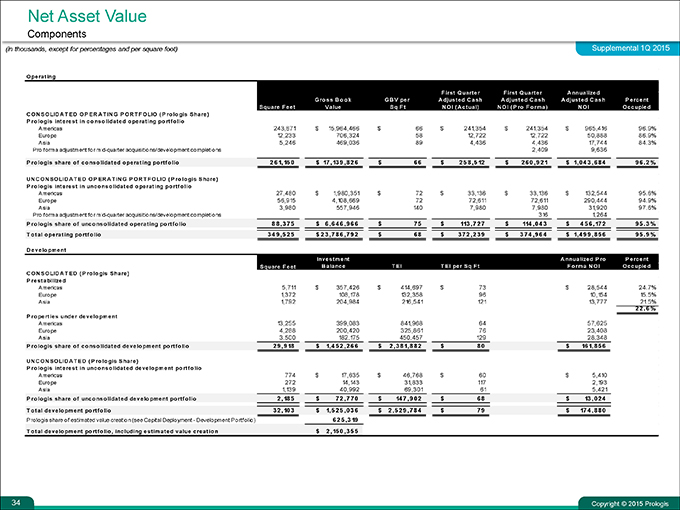

Net Asset Value Components

(in thousands, except for percentages and per square foot) Supplemental 1Q 2015

Operating

F irst Quarter F irst Quarter A nnualized

Gross Book GBV per Adjusted Cash Adjusted Cash Adjusted Cash Percent

Square Feet Value Sq Ft NOI (Actual) NOI (Pro Forma) NOI Occupied

CONSOLIDATED OPERATING PORTFOLIO (Prologis Share)

Prologis interest in consolidated operating portfolio

Americas 243,671 $ 15,964,466 $ 66 $ 241,354 $ 241,354 $ 965,416 96.9%

Europe 12,233 706,324 58 12,722 12,722 50,888 86.9%

Asia 5,246 469,036 89 4,436 4,436 17,744 84.3%

Proforma adjustment for mid-quarter acquisitions/development completions 2,409 9,636

Prologis share of consolidated operating portfolio 261,150 $ 17,139, 826 $ 66 $ 258,512 $ 260,921 $ 1,0 43,6849 6.2%

UNCONSOLIDATED OPERATING PORTFOLIO (Prologis Share)

Prologis interest in unconso lidated operating portfolio

Americas 27,480 $ 1,980,351 $ 72 $ 33,136 $ 33,136 $ 132,544 95.6%

Europe 56,915 4,108,669 72 72,611 72,611 290,444 94.9%

Asia 3,980 557,946 140 7,980 7,980 31,920 97.6%

Proforma adjustment for mid-quarter acquisitions/development completions 316 1,264

Prologis share of unconsolidated operating portfolio 88,375 $ 6,646,966 $ 75 $ 113 , 7 2 7 $ 114 , 0 4 3 $ 4 5 6 , 17 2 9 5 . 3 %

Total operating portfolio 3 4 9 , 5 2 5 $ 2 3 , 7 8 6 , 7 9 2 $ 6 8 $ 3 7 2 , 2 3 9 $ 3 7 4 , 9 6 4 $ 1, 4 9 9 , 8 5 6 9 5 .. 9 %

Development

Investment Annualized Pro Percent

Square Feet Balance TEI TEI per Sq Ft Forma NOI Occupied

CONSOLIDATED (Prologis Share)

Prestabilized

Americas 5,711 $ 357,426 $ 414,697 $ 73 $ 28,544 24.7%

Europe 1,372 108,178 132,358 96 10,154 15.5%

Asia 1,792 204,984 216,541 121 13,777 21.5% 22.6 %

Properties under development

Americas 13,255 399,083 841,968 64 57,625

Europe 4,288 200,420 325,861 76 23,408

Asia 3,500 182,175 450,457 129 28,348

Prologis share of consolidated development portfolio 29,918 $ 1, 4 5 2 , 2 6 6 $ 2 , 3 8 1, 8 8 2 $ 8 0 $ 16 1, 8 5 6

UNCONSOLIDATED (Prologis Share)

Prologis interest in unconsolidated development portfolio

Americas 774 $ 17,635 $ 46,768 $ 60 $ 5,410

Europe 272 14,143 31,833 117 2,193

Asia 1,139 40,992 69,301 61 5,421

Prologis share of unconsolidated development portfolio 2, 18 5 $ 7 2 , 7 7 0 $ 14 7 , 9 0 2 $ 6 8 $ 13 , 0 2 4

Total development portfolio 3 2 , 10 3 $ 1, 5 2 5 , 0 3 6 $ 2 , 5 2 9 , 7 8 4 $ 7 9 $ 17 4 , 8 8 0

Prologis share of estimated value creation (see Capital Deployment—Development Portfolio) 6 2 5 , 3 19

Total development portfolio, including estimated value creatio n $ 2 , 15 0 , 3 5 5

Copyright © 2015 Prologis

34

|

|

Net Asset Value

Components—Continued

(in thousands) Supplemental 1Q 2015

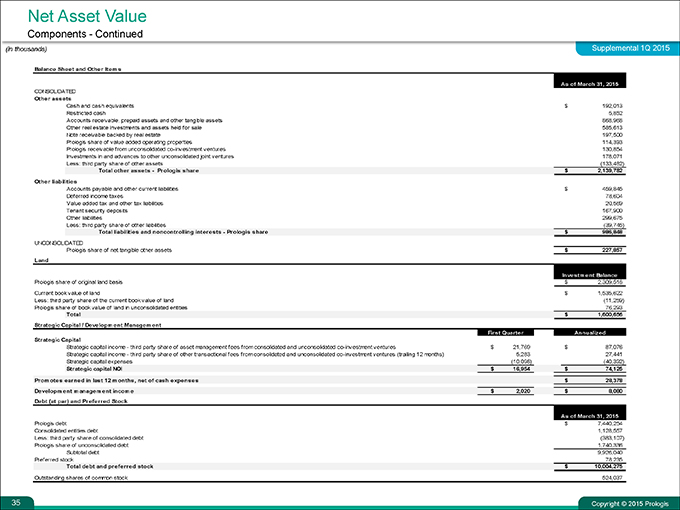

Balance Sheet and Other Items

As of March 31, 2015

CONSOLIDATED Other assets

Cash and cash equivalents $ 192,013

Restricted cash 5,852

Accounts receivable, prepaid assets and other tangible assets 868,968

Other real estate investments and assets held for sale 585,613

Note receivable backed by real estate 197,500

Prologis share of value added operating properties 114,393

Prologis receivable from unconsolidated co-investment ventures 130,854