Earnings Release and Supplemental Information

Unaudited

Second Quarter 2012

Table of Contents

Second Quarter 2012 Report

Overview

Press Release 1

Highlights

Company Profile 4

Financial Information

Consolidated Balance Sheets 6

Consolidated Statements of Operations 7

Reconciliation of Net Earnings (Loss) to FFO 8

EBITDA Reconciliation 9

Operations Overview

Operating Portfolio 10

Operating Metrics 13

Customer Information 14

Capital Deployment

Building Dispositions and Contributions 15

Building Acquisitions 16

Development Starts 17

Development Portfolio 19

Land Portfolio 20

Private Capital

Detail Fund Information 22

Fund Operating and Balance Sheet Information 23

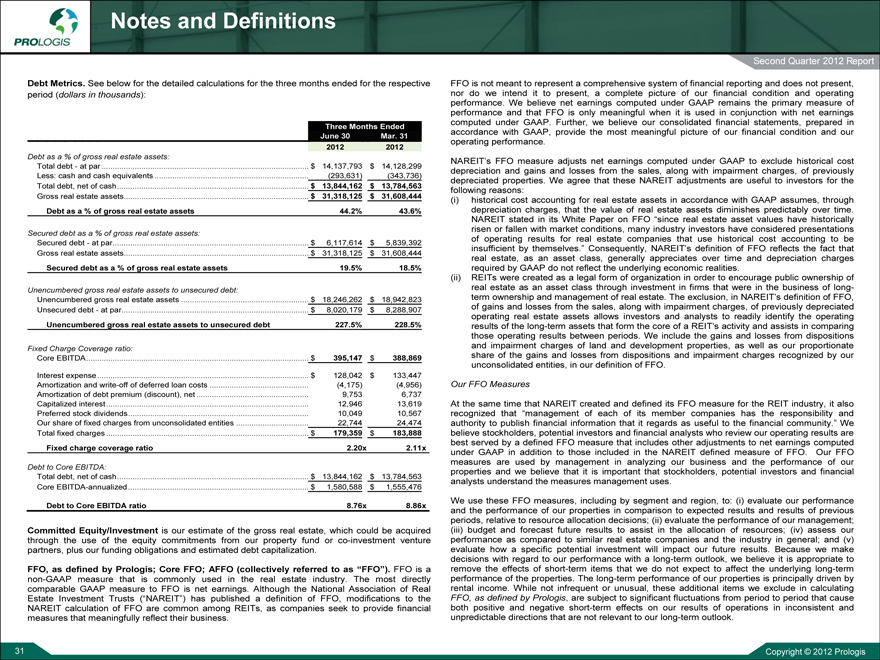

Capitalization

Debt and Equity Summary 24

Debt Covenants and Other Metrics 25

Assets Under Management 26

Net Asset Value

Components 27

Notes and Definitions 29

Port Reading, New Jersey, United States

Prologis Park Narashino, Chiba, Japan

Prologis Park Chanteloup, Cramayel, France

Copyright © 2012 Prologis

Copyright ©

2012 Prologis

1

Prologis, Inc. Announces Second Quarter 2012 Earnings Results

-

Core FFO of $0.43 per fully diluted share -

-

35 million square feet of leasing in its combined operating and development portfolios -

-

Company increases low end of full year guidance -

SAN FRANCISCO, July 26, 2012 – Prologis, Inc. (NYSE: PLD), the leading

global owner, operator and developer of industrial real estate, today reported

results for the second quarter of 2012.

Core funds from operations (Core FFO) per fully diluted share was $0.43 for

the second quarter 2012 compared to $0.35 for the same period in 2011.

Funds from operations (FFO) as defined by Prologis per fully diluted share was

$0.37 for the second quarter 2012 compared to $0.03 for the same period in

2011. The difference between Core FFO and FFO in the second quarter 2012

primarily relates to merger integration expenses. Net loss per share was

$(0.02) for the second quarter 2012 compared to a net loss of $(0.49) for the

same period in 2011. The second quarter 2011 comparative results reflect two

months of stand-alone legacy ProLogis and approximately one month of

results for the combined company. Therefore, they are not directly comparable

to the 2012 reported results.

“We delivered solid results for the second quarter despite forecasts of slower

economic growth," said Hamid R. Moghadam, chairman and co-chief executive

officer, Prologis. “We continue to make excellent progress on our priorities,

increasing occupancy in our operating and development portfolios. We also

received unitholder and regulatory approval to liquidate Prologis European

Properties. While we will continue to exercise a patient and deliberate

approach to achieving our strategic goals by the end of 2013, Prologis is well

positioned to remain opportunistic, flexible and laser-focused on taking

advantage of growth opportunities around the world.”

Operating Portfolio Metrics

During the quarter, the company leased a total of 35.0 million square feet (3.3

million square meters) in its combined operating and development portfolios.

Prologis ended the quarter above plan with 92.4 percent occupancy in its

operating portfolio, up 10 basis points over the prior quarter. Tenant retention

in the quarter was 82.4 percent, with renewals totaling 20.2 million square feet

(1.9 million square meters).

Same-store net operating income (NOI) in the second quarter of 2012

increased 0.4 percent over the second quarter 2011 on a GAAP basis,

compared to an increase of 1.7 percent in the first quarter of 2012. Rental

rates on leases signed in the second quarter same-store pool decreased by

3.9 percent from in-place rents, as compared to a decrease of 1.1 percent in

the first quarter 2012.

“Building on the momentum from last quarter, the team delivered another

strong quarter of leasing volume across our global portfolio, and we completed

the majority of our lease expirations for the balance of the year,” said Walter C.

Rakowich, co-chief executive officer, Prologis. “While the strongest demand

continues to be for large, Class-A facilities, we saw a notable improvement in

our facilities that are less than 100,000 square feet, and occupancy in Europe

continues to hold. Customers have new requirements for e-commerce facilities

and remain focused on improving supply chain efficiencies. Given continued

supply constraints, our customers with targeted requirements are increasingly

pursuing build-to-suits, which we are able to readily accommodate with our

strategic land portfolio.”

Dispositions and Contributions

During the quarter, the company completed approximately $228 million in

building and land dispositions and contributions, of which $191 million was

Prologis’ share. The building sales and contributions reflect a weighted

average stabilized capitalization rate of 7.6 percent.

Development Starts & Building Acquisitions

Capital deployed or committed during the second quarter 2012 totaled

approximately $313 million, of which $277 million was Prologis’ share,

including:

Development starts of $229 million totaling 3.7 million square feet

(343,740 square meters) in nine projects, which monetized $52 million of

land. Of the total expected investment, 70 percent was in build-to-suit

projects. The estimated value creation on development starts in the

second quarter is $33 million with a stabilized yield of 7.2 percent and a

margin of approximately 14 percent.

Building acquisitions of $85 million in 13 logistics facilities totaling

approximately 1.5 million square feet (139,350 square meters) with a

stabilized capitalization rate of 7.2 percent. Of the total acquisitions, $48

million was Prologis’ share.

At quarter end, Prologis’ global development portfolio comprised 13.5 million

square feet (1.3 million square meters), with a total expected investment of

$1.3 billion of which Prologis’ share is $1 billion. The estimated value creation

at stabilization is expected to be $228 million with a stabilized yield of 7.8

percent and a margin of approximately 18 percent.

|

Copyright ©

2012 Prologis

2

Private Capital Activity

During the quarter, Prologis raised $163 million in new third-party equity for

the Prologis Targeted U.S. Logistics Fund and the Prologis Targeted Europe

Logistics Fund. In addition, ProLogis European Properties’ (PEPR) unitholders

approved the liquidation of the fund during its annual meeting held on June 27,

2012. Prologis currently owns 99.5 percent of the ordinary units and 98.6

percent of the preferred units of PEPR.

“We had a strong quarter of capital raising for our open-end funds from a

diverse mix of new and existing investors,” said Guy F. Jaquier, chief executive

officer, Prologis Private Capital. “This level of activity is demonstrative of the

continued demand for high-quality industrial real estate around the globe. In

Japan, we continue to move forward with our development fund and to

evaluate the optimal structure for our operating assets. In Europe we are

pleased to be winding up PEPR ahead of schedule and recapitalizing

PEPR’s high-quality assets over the next several quarters.”

Capital Markets

Prologis completed $1.2 billion of debt financings, re-financings and pay-

downs, with approximately $989 million related to the REIT and $176 million

on behalf of our property funds during the quarter.

Significant financing activity during the second quarter included the following:

Repayment of $449 million of its 2.25

percent convertible notes and $59 million of senior unsecured notes at maturity in the

second quarter, as previously announced;

Financings of three TMK bonds of 25.4 billion yen (USD 332 million) with a

weighted average term of 6.6 years and weighted average rate of 1.21

percent; and

Subsequent to quarter end, Prologis closed two transactions for Prologis

European Properties Fund II, a 40 million pounds sterling (USD 63 million)

secured facility and a 145 million euro (USD 184 million) senior unsecured

term loan.

“We continue to have access to capital markets at attractive rates globally,

demonstrating the quality of our assets and strength of our global

platform,” said Thomas S. Olinger, chief

financial officer, Prologis. “Excluding the

impact of fund rationalization activity, we have reduced our share of debt

by $2.3 billion since the

merger.”

Guidance for 2012

Prologis increased the low end of its full-year 2012 Core FFO guidance range

to $1.64 to $1.70 per diluted share, up from $1.60 to $1.70 per diluted share.

The company also expects to recognize net earnings, for GAAP purposes, of

$0.22 to $0.28 per share. The difference between the company’s Core FFO

and net earnings guidance for 2012 predominantly relates to real estate

depreciation, recognized gains on real estate transactions and merger-related

expenses.

The Core FFO and earnings guidance reflected above excludes any potential

future gains (losses) recognized from real estate transactions. In reconciling

from net earnings to Core FFO, Prologis makes certain adjustments, including

but not limited to real estate depreciation and amortization expense,

impairment charges, deferred taxes, and unrealized gains or losses on foreign

currency or derivative activity, as well as transaction and merger costs.

Webcast and Conference Call Information

The company will host a webcast /conference call to discuss quarterly results,

current market conditions and future outlook today, July 26, 2012, at 12:00 p.m.

U.S. Eastern Time. Interested parties are encouraged to access the live

webcast by clicking the microphone icon located near the top of the opening

Interested parties also can participate via conference call by dialing 877-256-

7020 from the United States and Canada or (+1) 973-409-9692 internationally

with reservation code 93137132.

A telephonic replay will be available from July 27, 2012, through August 27,

2012, at 855-859-2056 (from the United States and Canada) or (+1) 404-537-

3406 (from all other countries), with the reservation code 93137132. The

webcast and podcast replay will be posted when available in the "Financial

Information" section of the Prologis Investor Relations website.

About Prologis

Prologis, Inc., is the leading owner, operator and developer of industrial real

estate, focused on global and regional markets across the Americas, Europe

and Asia. As of June 30, 2012, Prologis owned or had investments in, on a

consolidated basis or through unconsolidated joint ventures, properties and

page

of

the

Prologis

Investor

Relations

website

(http://ir.prologis.com). |

Copyright ©

2012 Prologis

3

development projects expected to total approximately 569 million square feet

(52.9 million square meters) in 21 countries. The company leases modern

distribution facilities to more than 4,500 customers, including manufacturers,

retailers, transportation companies, third-party logistics providers and other

enterprises.

The statements in this release that are not historical facts are

forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933, as amended, and Section 21E of the Securities

Exchange Act of 1934, as amended. These forward-looking statements

are based on current expectations, estimates and projections about the industry

and markets in which Prologis operates, management’s beliefs and

assumptions made by management. Such statements involve

uncertainties that could significantly impact Prologis’ financial

results. Words such as “expects,” “anticipates,” “intends,” “plans,”

“believes,” “seeks,” “estimates,” variations of

such words and similar expressions are intended to identify such

forward-looking statements, which generally are not historical in

nature. All statements that address operating performance, events or

developments that we expect or anticipate will occur in the future —

including statements relating to rent and occupancy growth, development

activity and changes in sales or contribution volume of developed

properties, disposition activity, general conditions in the geographic areas where

we operate, synergies to be realized from our recent merger transaction, our

debt and financial position, our ability to form new property funds and

the availability of capital in existing or new property funds — are

forward-looking statements. These statements are not guarantees of

future performance and involve certain risks, uncertainties and

assumptions that are difficult to predict. Although we believe the expectations

reflected in any forward-looking statements are based on reasonable

assumptions, we can give no assurance that our expectations will be

attained and therefore, actual outcomes and results may differ materially

from what is expressed or forecasted in such forward-looking

statements. Some of the factors that may affect outcomes and results include,

but are not limited to: (i) national, international, regional and local

economic climates, (ii) changes in financial markets, interest rates and

foreign currency exchange rates, (iii) increased or unanticipated

competition for our properties, (iv) risks associated with acquisitions,

dispositions and development of properties, (v) maintenance of real estate

investment trust (“REIT”) status and tax structuring, (vi)

availability of financing and capital, the levels of debt that we

maintain and our credit ratings, (vii) risks related to our investments

in our co-investment ventures and funds, including our ability to establish

new co- investment ventures and funds, (viii) risks of doing business

internationally, including currency risks, (ix) environmental

uncertainties, including risks of natural disasters, and (x) those

additional factors discussed in reports filed with the Securities and Exchange

Commission by Prologis under the heading “Risk Factors.” Prologis

undertakes no duty to update any forward-looking statements appearing

in this release. Prologis Contacts

Tracy A. Ward

James Larkin

SVP, IR & Corporate Communications

VP, Corporate Communications

Direct: +1 415 733 9565

Direct: +1 415 733 9411

Email: tward@prologis.com

Email: jlarkin@prologis.com

|

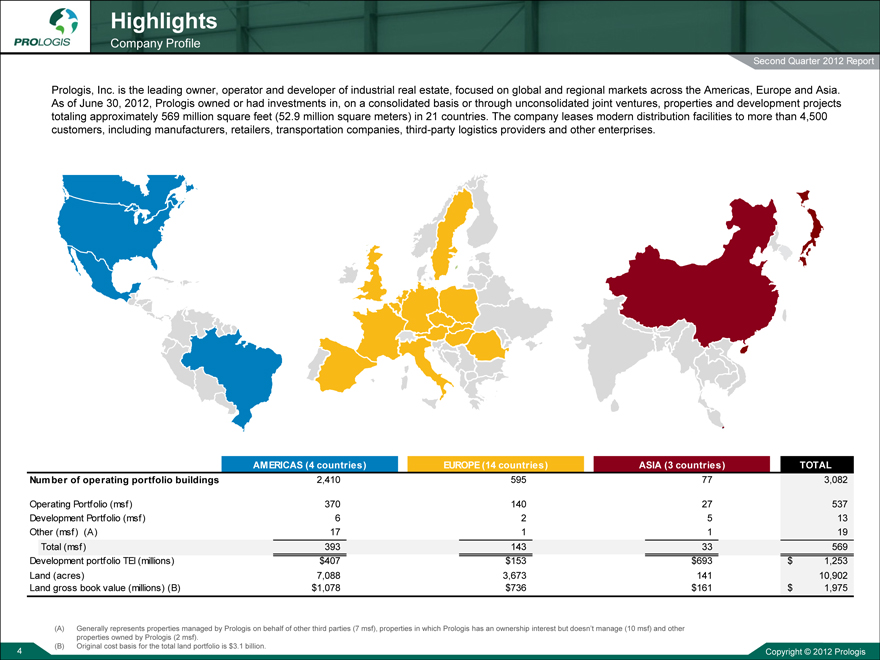

Highlights

Company Profile

Second Quarter 2012 Report

Prologis, Inc. is the leading owner, operator and developer of industrial real estate, focused on global and regional markets across the Americas, Europe and Asia. As of June 30, 2012, Prologis owned or had investments in, on a consolidated basis or through unconsolidated joint ventures, properties and development projects totaling approximately 569 million square feet (52.9 million square meters) in 21 countries. The company leases modern distribution facilities to more than 4,500 customers, including manufacturers, retailers, transportation companies, third-party logistics providers and other enterprises.

AMERICAS (4 countries) EUROPE (14 countries) ASIA (3 countries) TOTAL

Number of operating portfolio buildings 2,410 595 77 3,082

Operating Portfolio (msf) 370 140 27 537

Development Portfolio (msf) 6 2 5 13

Other (msf) (A) 17 1 1 19

Total (msf) 393 143 33 569

Development portfolio TEI (millions) $407 $153 $693 $ 1,253

Land (acres) 7,088 3,673 141 10,902

Land gross book value (millions) (B) $1,078 $736 $161 $ 1,975

(A) Generally represents properties managed by Prologis on behalf of other third parties (7 msf), properties in which Prologis has an ownership interest but doesn’t manage (10 msf) and other properties owned by Prologis (2 msf).

(B) Original cost basis for the total land portfolio is $3.1 billion.

Copyright © 2012 Prologis

4

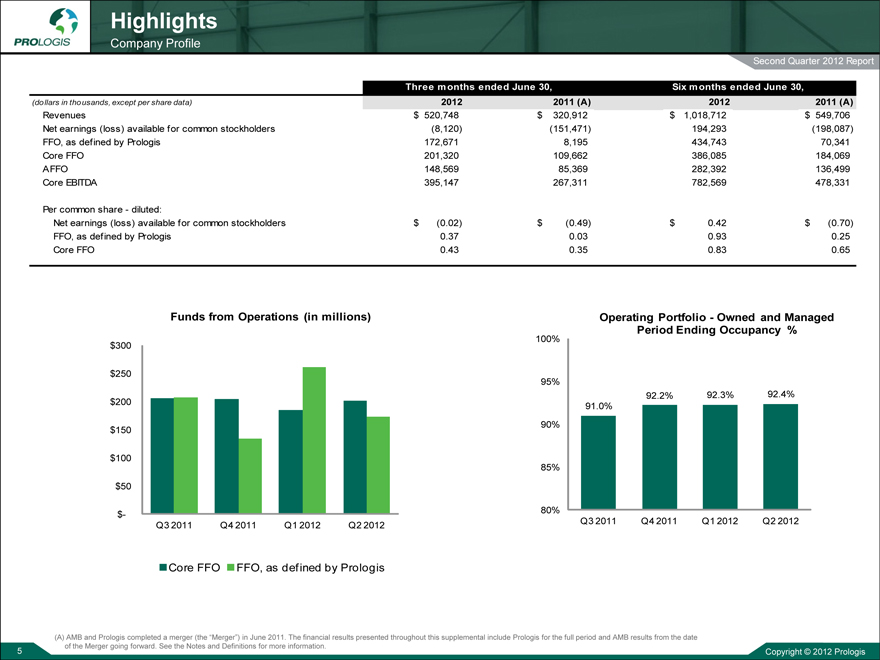

Highlights

Company Profile

Second Quarter 2012 Report

Three months ended June 30, Six months ended June 30,

(dollars in thousands, except per share data) 2012 2011 (A) 2012 2011 (A)

Revenues $ 520,748 $ 320,912 $ 1,018,712 $ 549,706

Net earnings (loss) available for common stockholders (8,120) (151,471) 194,293 (198,087)

FFO, as defined by Prologis 172,671 8,195 434,743 70,341

Core FFO 201,320 109,662 386,085 184,069

AFFO 148,569 85,369 282,392 136,499

Core EBITDA 395,147 267,311 782,569 478,331

Per common share-diluted:

Net earnings (loss) available for common stockholders $ (0.02) $ (0.49) $ 0.42 $ (0.70)

FFO, as defined by Prologis 0.37 0.03 0.93 0.25

Core FFO 0.43 0.35 0.83 0.65

Funds from Operations (in millions)

$300

$250

$200

$150

$100

$50

$-

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Operating Portfolio-Owned and Managed

Period Ending Occupancy %

100%

95%

92.2% 92.3% 92.4%

91.0%

90%

85%

80%

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Core FFO FFO, as defined by Prologis

(A) AMB and Prologis completed a merger (the “Merger”) in June 2011. The financial results presented throughout this supplemental include Prologis for the full period and AMB results from the date of the Merger going forward. See the Notes and Definitions for more information.

Copyright © 2012 Prologis

5

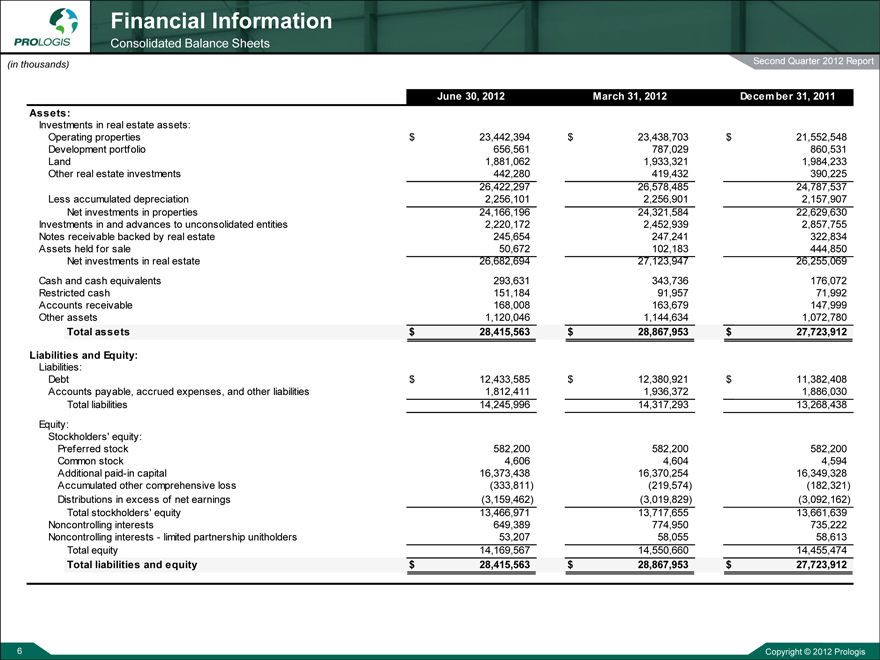

Financial Information

Consolidated Balance Sheets

Second Quarter 2012 Report

(in thousands)

June 30, 2012 March 31, 2012 December 31, 2011

Assets:

Investments in real estate assets:

Operating properties $ 23,442,394 $ 23,438,703 $ 21,552,548

Development portfolio 656,561 787,029 860,531

Land 1,881,062 1,933,321 1,984,233

Other real estate investments 442,280 419,432 390,225

26,422,297 26,578,485 24,787,537

Less accumulated depreciation 2,256,101 2,256,901 2,157,907

Net investments in properties 24,166,196 24,321,584 22,629,630

Investments in and advances to unconsolidated entities 2,220,172 2,452,939 2,857,755

Notes receivable backed by real estate 245,654 247,241 322,834

Assets held for sale 50,672 102,183 444,850

Net investments in real estate 26,682,694 27,123,947 26,255,069

Cash and cash equivalents 293,631 343,736 176,072

Restricted cash 151,184 91,957 71,992

Accounts receivable 168,008 163,679 147,999

Other assets 1,120,046 1,144,634 1,072,780

Total assets $ 28,415,563 $ 28,867,953 $ 27,723,912

Liabilities and Equity:

Liabilities:

Debt $ 12,433,585 $ 12,380,921 $ 11,382,408

Accounts payable, accrued expenses, and other liabilities 1,812,411 1,936,372 1,886,030

Total liabilities 14,245,996 14,317,293 13,268,438

Equity:

Stockholders’ equity:

Preferred stock 582,200 582,200 582,200

Common stock 4,606 4,604 4,594

Additional paid-in capital 16,373,438 16,370,254 16,349,328

Accumulated other comprehensive loss (333,811) (219,574) (182,321)

Distributions in excess of net earnings (3,159,462) (3,019,829) (3,092,162)

Total stockholders’ equity 13,466,971 13,717,655 13,661,639

Noncontrolling interests 649,389 774,950 735,222

Noncontrolling interests-limited partnership unitholders 53,207 58,055 58,613

Total equity 14,169,567 14,550,660 14,455,474

Total liabilities and equity $ 28,415,563 $ 28,867,953 $ 27,723,912

Copyright © 2012 Prologis

6

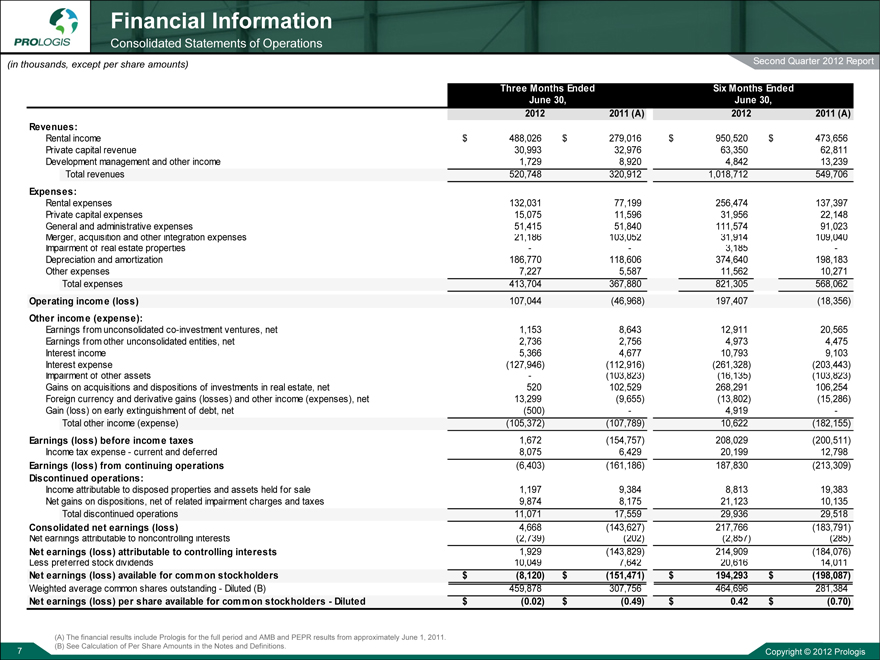

Financial Information

Consolidated Statements of Operations

(in thousands, except per share amounts)

Second Quarter 2012 Report

Three Months Ended Six Months Ended

June 30, June 30,

2012 2011 (A) 2012 2011 (A)

Revenues:

Rental income $ 488,026 $ 279,016 $ 950,520 $ 473,656

Private capital revenue 30,993 32,976 63,350 62,811

Development management and other income 1,729 8,920 4,842 13,239

Total revenues 520,748 320,912 1,018,712 549,706

Expenses:

Rental expenses 132,031 77,199 256,474 137,397

Private capital expenses 15,075 11,596 31,956 22,148

General and administrative expenses 51,415 51,840 111,574 91,023

Merger, acquisition and other integration expenses 21,186 103,052 31,914 109,040

Impairment of real estate properties- - 3,185 -

Depreciation and amortization 186,770 118,606 374,640 198,183

Other expenses 7,227 5,587 11,562 10,271

Total expenses 413,704 367,880 821,305 568,062

Operating income (loss) 107,044 (46,968) 197,407 (18,356)

Other income (expense):

Earnings from unconsolidated co-investment ventures, net 1,153 8,643 12,911 20,565

Earnings from other unconsolidated entities, net 2,736 2,756 4,973 4,475

Interest income 5,366 4,677 10,793 9,103

Interest expense (127,946) (112,916) (261,328) (203,443)

Impairment of other assets- (103,823) (16,135) (103,823)

Gains on acquisitions and dispositions of investments in real estate, net 520 102,529 268,291 106,254

Foreign currency and derivative gains (losses) and other income (expenses), net 13,299 (9,655) (13,802) (15,286)

Gain (loss) on early extinguishment of debt, net (500) - 4,919 -

Total other income (expense) (105,372) (107,789) 10,622 (182,155)

Earnings (loss) before income taxes 1,672 (154,757) 208,029 (200,511)

Income tax expense-current and deferred 8,075 6,429 20,199 12,798

Earnings (loss) from continuing operations (6,403) (161,186) 187,830 (213,309)

Discontinued operations:

Income attributable to disposed properties and assets held for sale 1,197 9,384 8,813 19,383

Net gains on dispositions, net of related impairment charges and taxes 9,874 8,175 21,123 10,135

Total discontinued operations 11,071 17,559 29,936 29,518

Consolidated net earnings (loss) 4,668 (143,627) 217,766 (183,791)

Net earnings attributable to noncontrolling interests (2,739) (202) (2,857) (285)

Net earnings (loss) attributable to controlling interests 1,929 (143,829) 214,909 (184,076)

Less preferred stock dividends 10,049 7,642 20,616 14,011

Net earnings (loss) available for common stockholders $ (8,120) $ (151,471) $ 194,293 $ (198,087)

Weighted average common shares outstanding-Diluted (B) 459,878 307,756 464,696 281,384

Net earnings (loss) per share available for common stockholders-Diluted $ (0.02) $ (0.49) $ 0.42 $ (0.70)

(A) The financial results include Prologis for the full period and AMB and PEPR results from approximately June 1, 2011. (B) See Calculation of Per Share Amounts in the Notes and Definitions.

Copyright © 2012 Prologis

7

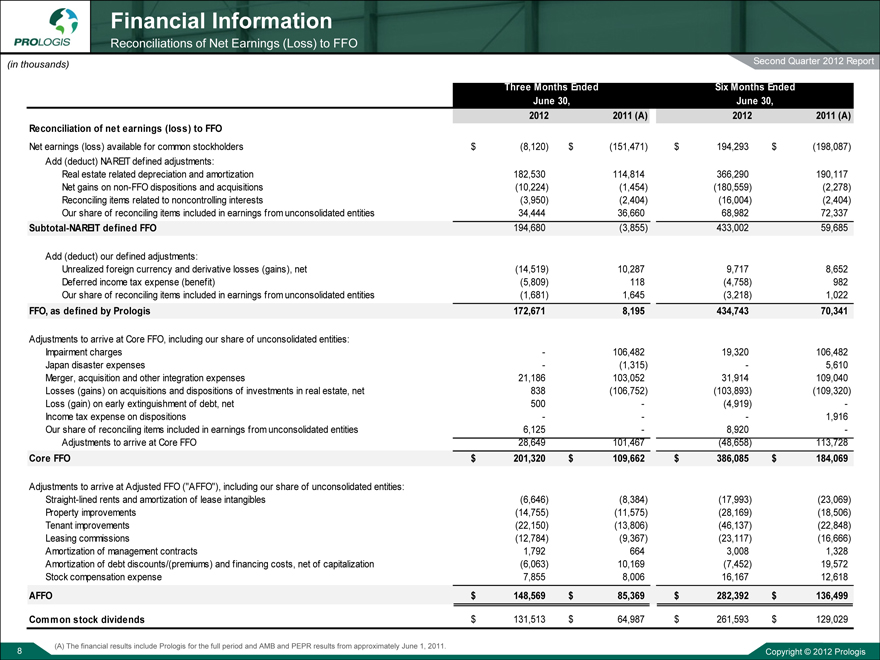

Financial Information

Reconciliations of Net Earnings (Loss) to FFO

(in thousands) Second Quarter 2012 Report

Three Months Ended Six Months Ended

June 30, June 30,

2012 2011 (A) 2012 2011 (A)

Reconciliation of net earnings (loss) to FFO

Net earnings (loss) available for common stockholders $ (8,120) $ (151,471) $ 194,293 $ (198,087)

Add (deduct) NAREIT defined adjustments:

Real estate related depreciation and amortization 182,530 114,814 366,290 190,117

Net gains on non-FFO dispositions and acquisitions (10,224) (1,454) (180,559) (2,278)

Reconciling items related to noncontrolling interests (3,950) (2,404) (16,004) (2,404)

Our share of reconciling items included in earnings from unconsolidated entities 34,444 36,660 68,982 72,337

Subtotal-NAREIT defined FFO 194,680 (3,855) 433,002 59,685

Add (deduct) our defined adjustments:

Unrealized foreign currency and derivative losses (gains), net (14,519) 10,287 9,717 8,652

Deferred income tax expense (benefit) (5,809) 118 (4,758) 982

Our share of reconciling items included in earnings from unconsolidated entities (1,681) 1,645 (3,218) 1,022

FFO, as defined by Prologis 172,671 8,195 434,743 70,341

Adjustments to arrive at Core FFO, including our share of unconsolidated entities:

Impairment charges - 106,482 19,320 106,482

Japan disaster expenses - (1,315) - 5,610

Merger, acquisition and other integration expenses 21,186 103,052 31,914 109,040

Losses (gains) on acquisitions and dispositions of investments in real estate, net 838 (106,752) (103,893) (109,320)

Loss (gain) on early extinguishment of debt, net 500 - (4,919) -

Income tax expense on dispositions - - - 1,916

Our share of reconciling items included in earnings from unconsolidated entities 6,125 - 8,920 -

Adjustments to arrive at Core FFO 28,649 101,467 (48,658) 113,728

Core FFO $ 201,320 $ 109,662 $ 386,085 $ 184,069

Adjustments to arrive at Adjusted FFO (“AFFO”), including our share of unconsolidated entities:

Straight-lined rents and amortization of lease intangibles (6,646) (8,384) (17,993) (23,069)

Property improvements (14,755) (11,575) (28,169) (18,506)

Tenant improvements (22,150) (13,806) (46,137) (22,848)

Leasing commissions (12,784) (9,367) (23,117) (16,666)

Amortization of management contracts 1,792 664 3,008 1,328

Amortization of debt discounts/(premiums) and financing costs, net of capitalization (6,063) 10,169 (7,452) 19,572

Stock compensation expense 7,855 8,006 16,167 12,618

AFFO $ 148,569 $ 85,369 $ 282,392 $ 136,499

Common stock dividends $ 131,513 $ 64,987 $ 261,593 $ 129,029

(A) The financial results include Prologis for the full period and AMB and PEPR results from approximately June 1, 2011.

Copyright © 2012 Prologis

8

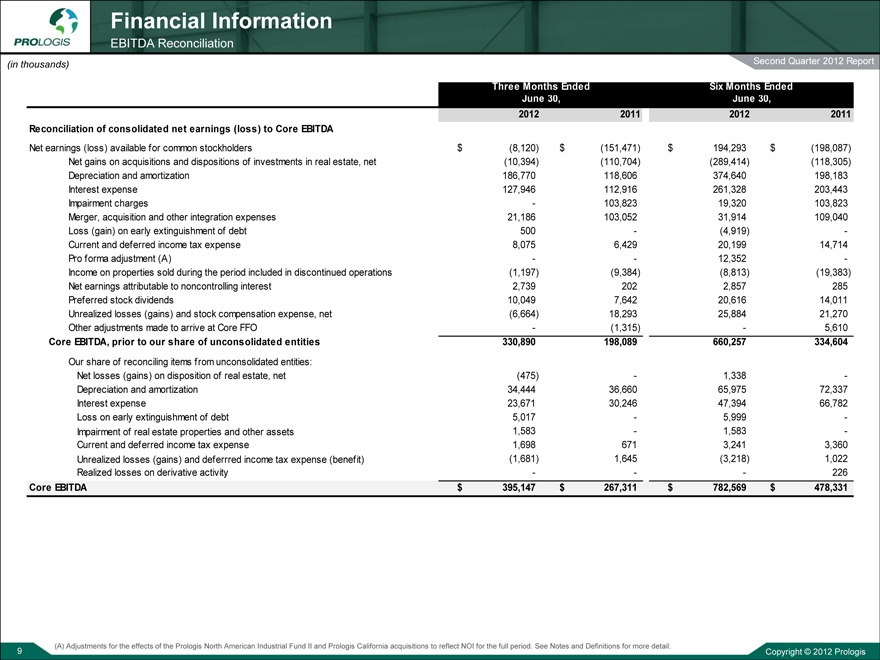

Financial Information

EBITDA Reconciliation

(in thousands) Second Quarter 2012 Report

Three Months Ended Six Months Ended

June 30, June 30,

2012 2011 2012 2011

Reconciliation of consolidated net earnings (loss) to Core EBITDA

Net earnings (loss) available for common stockholders $ (8,120) $ (151,471) $ 194,293 $ (198,087)

Net gains on acquisitions and dispositions of investments in real estate, net (10,394) (110,704) (289,414) (118,305)

Depreciation and amortization 186,770 118,606 374,640 198,183

Interest expense 127,946 112,916 261,328 203,443

Impairment charges - 103,823 19,320 103,823

Merger, acquisition and other integration expenses 21,186 103,052 31,914 109,040

Loss (gain) on early extinguishment of debt 500 - (4,919) -

Current and deferred income tax expense 8,075 6,429 20,199 14,714

Pro forma adjustment (A) - - 12,352 -

Income on properties sold during the period included in discontinued operations (1,197) (9,384) (8,813) (19,383)

Net earnings attributable to noncontrolling interest 2,739 202 2,857 285

Preferred stock dividends 10,049 7,642 20,616 14,011

Unrealized losses (gains) and stock compensation expense, net (6,664) 18,293 25,884 21,270

Other adjustments made to arrive at Core FFO - (1,315) - 5,610

Core EBITDA, prior to our share of unconsolidated entities 330,890 198,089 660,257 334,604

Our share of reconciling items from unconsolidated entities:

Net losses (gains) on disposition of real estate, net (475) - 1,338 -

Depreciation and amortization 34,444 36,660 65,975 72,337

Interest expense 23,671 30,246 47,394 66,782

Loss on early extinguishment of debt 5,017 - 5,999 -

Impairment of real estate properties and other assets 1,583 - 1,583 -

Current and deferred income tax expense 1,698 671 3,241 3,360

Unrealized losses (gains) and deferrred income tax expense (benefit) (1,681) 1,645 (3,218) 1,022

Realized losses on derivative activity - - - 226

Core EBITDA $ 395,147 $ 267,311 $ 782,569 $ 478,331

(A) Adjustments for the effects of the Prologis North American Industrial Fund II and Prologis California acquisitions to reflect NOI for the full period. See Notes and Definitions for more detail.

Copyright © 2012 Prologis

9

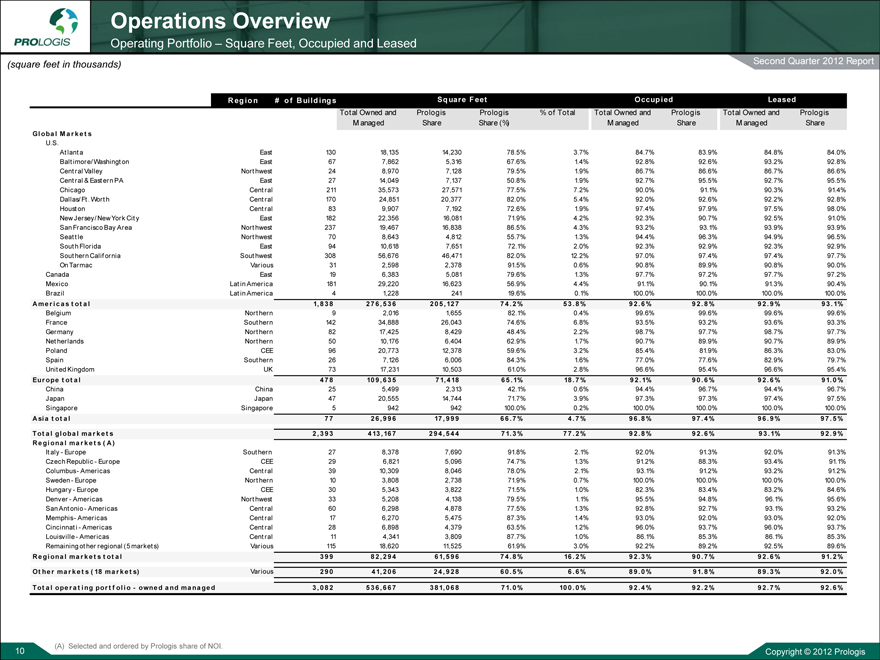

Operations Overview

Operating Portfolio – Square Feet, Occupied and Leased

(square feet in thousands)

Second Quarter 2012 Report

Region # of Buildings Square Feet Occupied Leased

Total Owned and Prologis Prologis % of Total Total Owned and Prologis Total Owned and Prologis

Managed Share Share (%) Managed Share Managed Share

Global Markets

U.S.

Atlanta East 130 18,135 14,230 78.5% 3.7% 84.7% 83.9% 84.8% 84.0%

Baltimore/Washington East 67 7,862 5,316 67.6% 1.4% 92.8% 92.6% 93.2% 92.8%

Central Valley Northwest 24 8,970 7,128 79.5% 1.9% 86.7% 86.6% 86.7% 86.6%

Central & Eastern PA East 27 14,049 7,137 50.8% 1.9% 92.7% 95.5% 92.7% 95.5%

Chicago Central 211 35,573 27,571 77.5% 7.2% 90.0% 91.1% 90.3% 91.4%

Dallas/ Ft . Worth Central 170 24,851 20,377 82.0% 5.4% 92.0% 92.6% 92.2% 92.8%

Houst on Central 83 9,907 7,192 72.6% 1.9% 97.4% 97.9% 97.5% 98.0%

New Jersey/ New York City East 182 22,356 16,081 71.9% 4.2% 92.3% 90.7% 92.5% 91.0%

San Francisco Bay Area Northwest 237 19,467 16,838 86.5% 4.3% 93.2% 93.1% 93.9% 93.9%

Seattle Northwest 70 8,643 4,812 55.7% 1.3% 94.4% 96.3% 94.9% 96.5%

South Florida East 94 10,618 7,651 72.1% 2.0% 92.3% 92.9% 92.3% 92.9%

Southern California Southwest 308 56,676 46,471 82.0% 12.2% 97.0% 97.4% 97.4% 97.7%

On Tarmac Various 31 2,598 2,378 91.5% 0.6% 90.8% 89.9% 90.8% 90.0%

Canada East 19 6,383 5,081 79.6% 1.3% 97.7% 97.2% 97.7% 97.2%

Mexico Lat in America 181 29,220 16,623 56.9% 4.4% 91.1% 90.1% 91.3% 90.4%

Brazil Lat in America 4 1,228 241 19.6% 0.1% 100.0% 100.0% 100.0% 100.0%

Americas total 1, 838276, 536205 , 12774.2 % 53.8 % 92.6 % 92.8 % 92.9 % 93.1%

Belgium Northern 9 2,016 1,655 82.1% 0.4% 99.6% 99.6% 99.6% 99.6%

France Southern 142 34,888 26,043 74.6% 6.8% 93.5% 93.2% 93.6% 93.3%

Germany Northern 82 17,425 8,429 48.4% 2.2% 98.7% 97.7% 98.7% 97.7%

Netherlands Northern 50 10,176 6,404 62.9% 1.7% 90.7% 89.9% 90.7% 89.9%

Poland CEE 96 20,773 12,378 59.6% 3.2% 85.4% 81.9% 86.3% 83.0%

Spain Southern 26 7,126 6,006 84.3% 1.6% 77.0% 77.6% 82.9% 79.7%

United Kingdom UK 73 17,231 10,503 61.0% 2.8% 96.6% 95.4% 96.6% 95.4%

Europe total 478109 , 63571, 41865.1% 18.7 % 92.1% 90.6 % 92.6 % 91.0 %

China China 25 5,499 2,313 42.1% 0.6% 94.4% 96.7% 94.4% 96.7%

Japan Japan 47 20,555 14,744 71.7% 3.9% 97.3% 97.3% 97.4% 97.5%

Singapore Singapore 5942 942 100.0% 0.2% 100.0% 100.0% 100.0% 100.0%

Asia total 7726, 99617, 99966.7 % 4.7 % 96.8 % 97.4 % 96.9 % 97.5 %

Tot al global markets 2,393413, 167294, 54471.3 % 77.2 % 92.8 % 92.6 % 93.1% 92.9 %

Regional markets ( A)

Italy—Europe Southern 27 8,378 7,690 91.8% 2.1% 92.0% 91.3% 92.0% 91.3%

Czech Republic—Europe CEE 29 6,821 5,096 74.7% 1.3% 91.2% 88.3% 93.4% 91.1%

Columbus- Americas Central 39 10,309 8,046 78.0% 2.1% 93.1% 91.2% 93.2% 91.2%

Sweden—Europe Northern 10 3,808 2,738 71.9% 0.7% 100.0% 100.0% 100.0% 100.0%

Hungary—Europe CEE 30 5,343 3,822 71.5% 1.0% 82.3% 83.4% 83.2% 84.6%

Denver—Americas Northwest 33 5,208 4,138 79.5% 1.1% 95.5% 94.8% 96.1% 95.6%

San Antonio—Americas Central 60 6,298 4,878 77.5% 1.3% 92.8% 92.7% 93.1% 93.2%

Memphis—Americas Central 17 6,270 5,475 87.3% 1.4% 93.0% 92.0% 93.0% 92.0%

Cincinnati—Americas Central 28 6,898 4,379 63.5% 1.2% 96.0% 93.7% 96.0% 93.7%

Louisville—Americas Central 11 4,341 3,809 87.7% 1.0% 86.1% 85.3% 86.1% 85.3%

Remaining other regional (5 markets) Various 115 18,620 11,525 61.9% 3.0% 92.2% 89.2% 92.5% 89.6%

Regional markets total 39982 , 29461, 59674.8 % 16.2 % 92.3 % 90.7 % 92.6 % 91.2 %

Other markets (18 markets) Various 29041, 20624 , 92860.5 % 6.6 % 89.0 % 91.8 % 89.3 % 92.0%

Total operating portfolio—owned and managed 3,082536, 667381, 06871.0% 100.0% 92.4 % 92.2 % 92.7 % 92.6 %

(A) Selected and ordered by Prologis share of NOI.

Copyright © 2012 Prologis

10

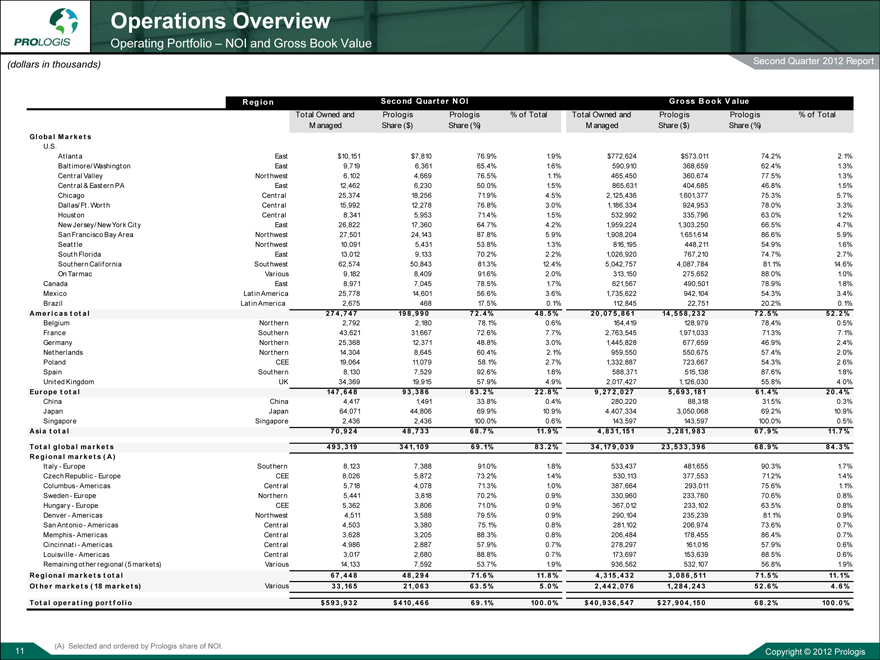

Operations Overview

Operating Portfolio – NOI and Gross Book Value

(dollars in thousands)

Second Quarter 2012 Report

Region Second Quarter NOI Gross Book Value

Total Owned and Prologis Prologis % of Total Total Owned and Prologis Prologis % of Total

Managed Share ($) Share (%) Managed Share ($) Share (%)

Global Markets

Atlanta East $10,151 $7,810 76.9% 1.9% $772,624 $573,011 74.2% 2.1%

Baltimore/ Washington East 9,719 6,361 65.4% 1.6% 590,910 368,659 62.4% 1.3%

Central Valley Northwest 6,102 4,669 76.5% 1.1% 465,450 360,674 77.5% 1.3%

Central & Eastern PA East 12,462 6,230 50.0% 1.5% 865,631 404,685 46.8% 1.5%

Chicago Central 25,374 18,256 71.9% 4.5% 2,125,436 1,601,377 75.3% 5.7%

Dallas/ Ft. Worth Central 15,992 12,278 76.8% 3.0% 1,186,334 924,953 78.0% 3.3%

Houston Central 8,341 5,953 71.4% 1.5% 532,992 335,796 63.0% 1.2%

New Jersey/ New York City East 26,822 17,360 64.7% 4.2% 1,959,224 1,303,250 66.5% 4.7%

San Francisco Bay Area Northwest 27,501 24,143 87.8% 5.9% 1,908,204 1,651,614 86.6% 5.9%

Seattle Northwest 10,091 5,431 53.8% 1.3% 816,195 448,211 54.9% 1.6%

South Florida East 13,012 9,133 70.2% 2.2% 1,026,920 767,210 74.7% 2.7%

Southern California Southwest 62,574 50,843 81.3% 12.4% 5,042,757 4,087,784 81.1% 14.6%

On Tarmac Various 9,182 8,409 91.6% 2.0% 313,150 275,652 88.0% 1.0%

Canada East 8,971 7,045 78.5% 1.7% 621,567 490,501 78.9% 1.8%

Mexico Latin America 25,778 14,601 56.6% 3.6% 1,735,622 942,104 54.3% 3.4%

Brazil Latin America 2,675 468 17.5% 0.1% 112,845 22,751 20.2% 0.1%

Americastotal 274,747 198,990 72.4% 48.5% 20,075,861 14,558,232 72.5% 52.2%

Belgium Northern 2,792 2,180 78.1% 0.6% 164,419 128,979 78.4% 0.5%

France Southern 43,621 31,667 72.6% 7.7% 2,763,545 1,971,033 71.3% 7.1%

Germany Northern 25,368 12,371 48.8% 3.0% 1,445,828 677,659 46.9% 2.4%

Netherlands Northern 14,304 8,645 60.4% 2.1% 959,550 550,675 57.4% 2.0%

Poland CEE 19,064 11,079 58.1% 2.7% 1,332,887 723,667 54.3% 2.6%

Spain Southern 8,130 7,529 92.6% 1.8% 588,371 515,138 87.6% 1.8%

United Kingdom UK 34,369 19,915 57.9% 4.9% 2,017,427 1,126,030 55.8% 4.0%

Europe total 147,648 93,386 63.2% 22.8% 9,272,027 5,693,181 61.4% 20.4%

China China 4,417 1,491 33.8% 0.4% 280,220 88,318 31.5% 0.3%

Japan Japan 64,071 44,806 69.9% 10.9% 4,407,334 3,050,068 69.2% 10.9%

Singapore Singapore 2,436 2,436 100.0% 0.6% 143,597 143,597 100.0% 0.5%

Asiatotal 70,924 48,733 68.7% 11.9% 4,831,151 3,281,983 67.9% 11.7%

Tot al global markets 493,319 341,109 69.1% 83.2% 34,179,039 23,533,396 68.9% 84.3%

Regional markets ( A)

Italy - Europe Southern 8,123 7,388 91.0% 1.8% 533,437 481,655 90.3% 1.7%

Czech Republic - Europe CEE 8,026 5,872 73.2% 1.4% 530,113 377,553 71.2% 1.4%

Columbus - Americas Central 5,718 4,078 71.3% 1.0% 387,664 293,011 75.6% 1.1%

Sweden - Europe Northern 5,441 3,818 70.2% 0.9% 330,960 233,760 70.6% 0.8%

Hungary - Europe CEE 5,362 3,806 71.0% 0.9% 367,012 233,102 63.5% 0.8%

Denver - Americas Northwest 4,511 3,588 79.5% 0.9% 290,104 235,239 81.1% 0.9%

San Antonio - Americas Central 4,503 3,380 75.1% 0.8% 281,102 206,974 73.6% 0.7%

Memphis - Americas Central 3,628 3,205 88.3% 0.8% 206,484 178,455 86.4% 0.7%

Cincinnati - Americas Central 4,986 2,887 57.9% 0.7% 278,297 161,016 57.9% 0.6%

Louisville - Americas Central 3,017 2,680 88.8% 0.7% 173,697 153,639 88.5% 0.6%

Remaining other regional (5 markets) Various 14,133 7,592 53.7% 1.9% 936,562 532,107 56.8% 1.9%

Regional markets total 67,448 48,294 71.6% 11.8% 4,315,432 3,086,511 71.5% 11.1%

Other markets (18 markets) Various 33,165 21,063 63.5% 5.0% 2,442,076 1,284,243 52.6% 4.6%

Total operating portfolio $593,932 $410,466 69.1% 100.0% $40,936,547 $27,904,150 68.2% 100.0%

(A) Selected and ordered by Prologis share of NOI.

Copyright © 2012 Prologis

11

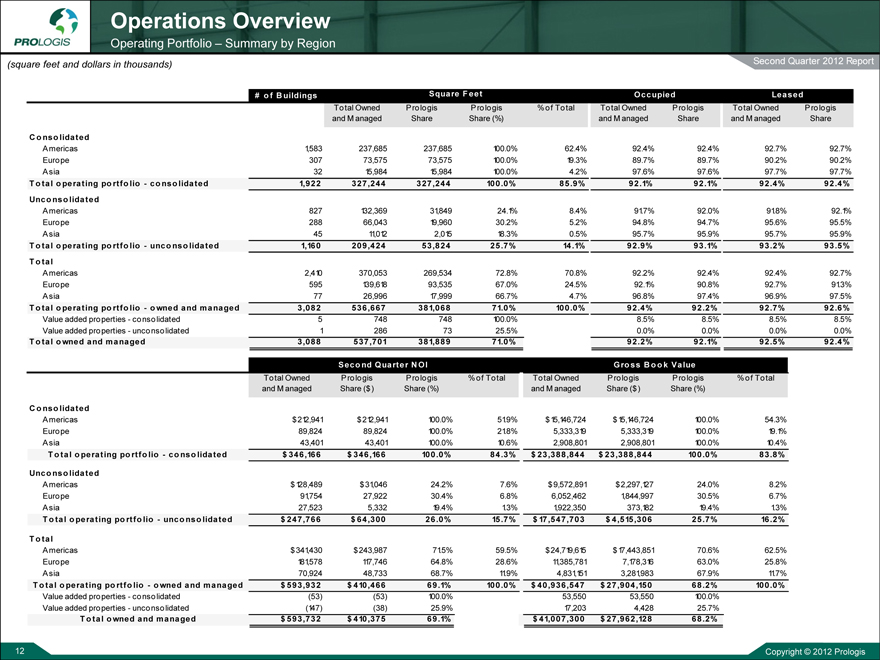

Operations Overview

Operating Portfolio – Summary by Region

(square feet and dollars in thousands)

Second Quarter 2012 Report

# of Buildings Square Feet Occupied Leased

Total Owned Prologis Prologis % of Total Total Owned Prologis Total Owned Prologis

and Managed Share Share (%) and Managed Share and M anaged Share

Consolidated

Americas 1,583 237,685 237,685 100.0% 62.4% 92.4% 92.4% 92.7% 92.7%

Europe 307 73,575 73,575 100.0% 19.3% 89.7% 89.7% 90.2% 90.2%

Asia 32 15,984 15,984 100.0% 4.2% 97.6% 97.6% 97.7% 97.7%

Total operating portfolio - consolidated 1,922 327,244 327,244 100.0% 85.9% 92.1% 92.1% 92.4% 92.4%

Unconsolidated

Americas 827 132,369 31,849 24.1% 8.4% 91.7% 92.0% 91.8% 92.1%

Europe 288 66,043 19,960 30.2% 5.2% 94.8% 94.7% 95.6% 95.5%

Asia 45 11,012 2,015 18.3% 0.5% 95.7% 95.9% 95.7% 95.9%

Total operating portfolio - unconsolidated 1,160 209,424 53,824 25.7% 14.1% 92.9% 93.1% 93.2% 93.5%

Total

Americas 2,410 370,053 269,534 72.8% 70.8% 92.2% 92.4% 92.4% 92.7%

Europe 595 139,618 93,535 67.0% 24.5% 92.1% 90.8% 92.7% 913%91.3%

Asia 77 26,996 17,999 66.7% 4.7% 96.8% 97.4% 96.9% 97.5%

Total operating portfolio - owned and managed 3,082 536,667 381,068 71.0% 100.0% 92.4% 92.2% 92.7% 92.6%

Value added properties - consolidated 5 748 748 100.0% 8.5% 8.5% 8.5% 8.5%

Value added properties - unconsolidated 1 286 73 25.5% 0.0% 0.0% 0.0% 0.0%

Total owned and managed 3,088 537,701 381,889 71.0% 92.2% 92.1% 92.5% 92.4%

Second Quarter NOI Gross Book Value

Total Owned Prologis Prologis %of% of Total Total Owned Prologis Prologis %of% of Total

and Managed Share ($) Share (%) and Managed Share ($) Share (%)

Consolidated

Americas $212,941 $212,941 100.0% 51.9% $15,146,724 $15,146,724 100.0% 54.3%

Europe 89,824 89,824 100.0% 21.8% 5,333,319 5,333,319 100.0% 19.1%

Asia 43,401 43,401 100.0% 10.6% 2,908,801 2,908,801 100.0% 10.4%

Total operating portfolio - consolidated $ 346,166 $ 346,166 100.0% 84.3% $ 23,388,844 $ 23,388,844 100.0% 83.8%

Unconsolidated

Americas $128,489 $31,046 24.2% 7.6% $9,572,891 $2,297,127 24.0% 8.2%

Europe 91,754 27,922 30.4% 6.8% 6,052,462 1,844,997 30.5% 6.7%

Asia 27,523 5,332 19.4% 1.3% 1,922,350 373,182 19.4% 1.3%

Total operating portfolio - unconsolidated $ 247,766 $ 64,300 26.0% 15.7% $ 17,547,703 $ 4,515,306 25.7% 16.2%

Total

Americas $341,430 $243,987 71.5% 59.5% $24,719,615 $17,443,851 70.6% 62.5%

Europe 181578, 117,746 64.8% 28.6% 11,385,781 7,178,316 63.0% 25.8%

Asia 70,924 48,733 68.7% 11.9% 4,831,151 3,281,983 67.9% 11.7%

Total operating portfolio - owned and managed $ 593,932 $ 410,466 69.1% 100.0% $ 40,936,547 $ 27,904,150 68.2% 100.0%

Value added properties - consolidated (53) (53) 100.0% 53,550 53,550 100.0%

Value added properties - unconsolidated (147) (38) 25.9% 17,203 4,428 25.7%

Total owned and managed $ 593,732 $ 410,375 69.1% $ 41,007,300 $ 27,962,128 68.2%

Copyright © 2012 Prologis

12

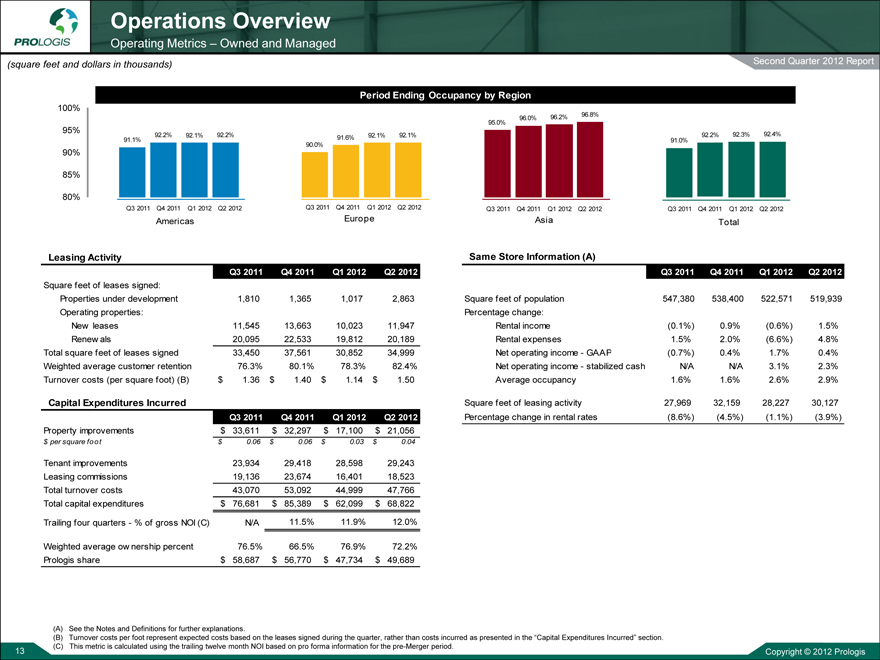

Operations Overview

Operating Metrics – Owned and Managed

Second Quarter 2012 Report

(square feet and dollars in thousands)

100% 95% 90% 85% 80%

Period Ending Occupancy by Region

92.2% 92.1% 92.2%

91.1%

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Americas

91.6% 92.1% 92.1%

90.0%

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Europe

96.0% 96.2% 96.8%

95.0%

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Asia

92.2% 92.3% 92.4%

91.0%

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Total

Leasing Activity

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Square feet of leases signed:

Properties under development 1,810 1,365 1,017 2,863

Operating properties:

New leases 11,545 13,663 10,023 11,947

Renewals 20,095 22,533 19,812 20,189

Total square feet of leases signed 33,450 37,561 30,852 34,999

Weighted average customer retention 76.3% 80.1% 78.3% 82.4%

Turnover costs (per square foot) (B) $ 1.36 $ 1.40 $ 1.14 $ 1.50

Capital Expenditures Incurred

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Property improvements $ 33,611 $ 32,297 $ 17,100 $ 21,056

$ per square foot $ 0.06 $ 0.06 $ 0.03 $ 0.04

Tenant improvements 23,934 29,418 28,598 29,243

Leasing commissions 19,136 23,674 16,401 18,523

Total turnover costs 43,070 53,092 44,999 47,766

Total capital expenditures $ 76,681 $ 85,389 $ 62,099 $ 68,822

Trailing four quarters-% of gross NOI (C) N/A 11.5% 11.9% 12.0%

Weighted average ownership percent 76.5% 66.5% 76.9% 72.2%

Prologis share $ 58,687 $ 56,770 $ 47,734 $ 49,689

Same Store Information (A)

Q3 2011 Q4 2011 Q1 2012 Q2 2012

Square feet of population 547,380 538,400 522,571 519,939

Percentage change:

Rental income (0.1%) 0.9% (0.6%) 1.5%

Rental expenses 1.5% 2.0% (6.6%) 4.8%

Net operating income-GAAP (0.7%) 0.4% 1.7% 0.4%

Net operating income-stabilized cash N/A N/A 3.1% 2.3%

Average occupancy 1.6% 1.6% 2.6% 2.9%

Square feet of leasing activity 27,969 32,159 28,227 30,127

Percentage change in rental rates (8.6%) (4.5%) (1.1%) (3.9%)

(A) See the Notes and Definitions for further explanations.

(B) Turnover costs per foot represent expected costs based on the leases signed during the quarter, rather than costs incurred as presented in the “Capital Expenditures Incurred” section. (C) This metric is calculated using the trailing twelve month NOI based on pro forma information for the pre-Merger period.

Copyright © 2012 Prologis

13

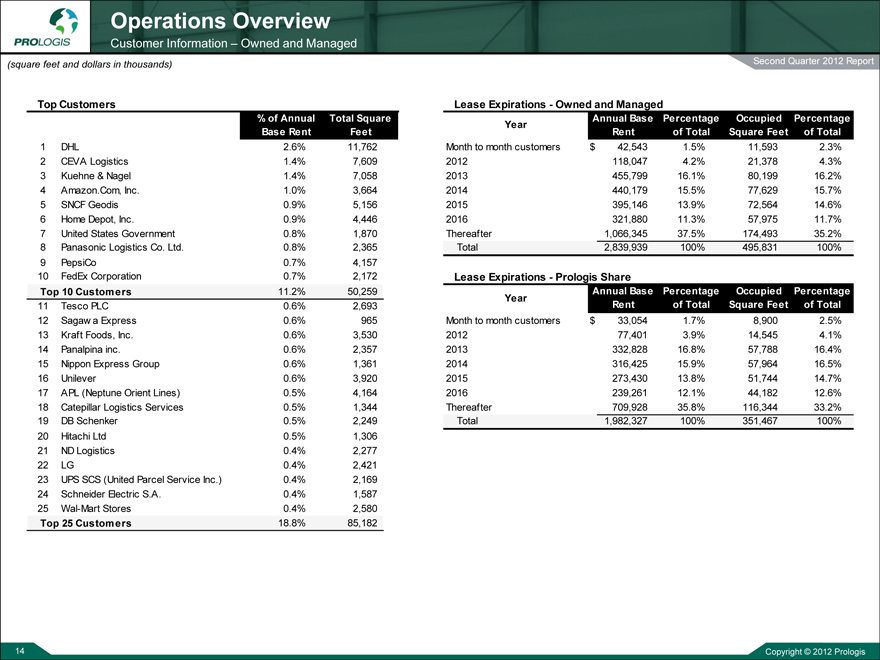

Operations Overview

Customer Information – Owned and Managed

(square feet and dollars in thousands)

Second Quarter 2012 Report

Top Customers

% of Annual Total Square

Base Rent Feet

1 DHL 2.6% 11,762

2 CEVA Logistics 1.4% 7,609

3 Kuehne & Nagel 1.4% 7,058

4 Amazon.Com, Inc. 1.0% 3,664

5 SNCF Geodis 0.9% 5,156

6 Home Depot, Inc. 0.9% 4,446

7 United States Government 0.8% 1,870

8 Panasonic Logistics Co. Ltd. 0.8% 2,365

9 PepsiCo 0.7% 4,157

10 FedEx Corporation 0.7% 2,172

Top 10 Customers 11.2% 50,259

11 Tesco PLC 0.6% 2,693

12 Sagawa Express 0.6% 965

13 Kraft Foods, Inc. 0.6% 3,530

14 Panalpina inc. 0.6% 2,357

15 Nippon Express Group 0.6% 1,361

16 Unilever 0.6% 3,920

17 APL (Neptune Orient Lines) 0.5% 4,164

18 Catepillar Logistics Services 0.5% 1,344

19 DB Schenker 0.5% 2,249

20 Hitachi Ltd 0.5% 1,306

21 ND Logistics 0.4% 2,277

22 LG 0.4% 2,421

23 UPS SCS (United Parcel Service Inc.) 0.4% 2,169

24 Schneider Electric S.A. 0.4% 1,587

25 Wal-Mart Stores 0.4% 2,580

Top 25 Customers 18.8% 85,182

Lease Expirations - Owned and Managed

Year Annual Base Percentage Occupied Percentage

Rent of Total Square Feet of Total

Month to month customers $ 42,543 1.5% 11,593 2.3%

2012 118,047 4.2% 21,378 4.3%

2013 455,799 16.1% 80,199 16.2%

2014 440,179 15.5% 77,629 15.7%

2015 395,146 13.9% 72,564 14.6%

2016 321,880 11.3% 57,975 11.7%

Thereafter 1,066,345 37.5% 174,493 35.2%

Total $ 2,839,939 100% 495,831 100%

Lease Expirations - Prologis Share

Annual Base Percentage Occupied Percentage

Year Rent of Total Square Feet of Total

Month to month customers $ 33,054 1.7% 8,900 2.5%

2012 77,401 3.9% 14,545 4.1%

2013 332,828 16.8% 57,788 16.4%

2014 316,425 15.9% 57,964 16.5%

2015 273,430 13.8% 51,744 14.7%

2016 239,261 12.1% 44,182 12.6%

Thereafter 709,928 35.8% 116,344 33.2%

Total $ 1,982,327 100% 351,467 100%

Copyright © 2012 Prologis

14

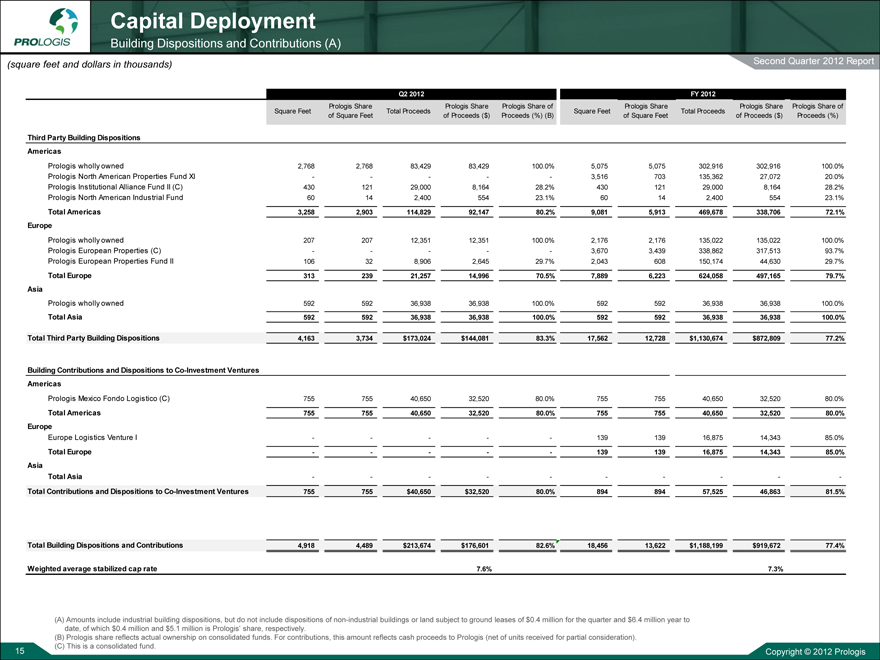

Capital Deployment

Building Dispositions and Contributions (A)

(square feet and dollars in thousands) Second Quarter 2012 Report

Q2 2012 FY 2012

Prologis Share Prologis Share Prologis Share of Prologis Share Prologis Share Prologis Share of

Square Feet Total Proceeds Square Feet Total Proceeds

of Square Feet of Proceeds ($) Proceeds (%) (B) of Square Feet of Proceeds ($) Proceeds (%)

Third Party Building Dispositions

Americas

Prologis wholly owned 2,768 2,768 83,429 83,429 100.0% 5,075 5,075 302,916 302,916 100.0%

Prologis North American Properties Fund XI - - - - - 3,516 703 135,362 27,072 20.0%

Prologis Institutional Alliance Fund II (C) 430 121 29,000 8,164 28.2% 430 121 29,000 8,164 28.2%

Prologis North American Industrial Fund 60 14 2,400 554 23.1% 60 14 2,400 554 23.1%

Total Americas 3,258 2,903 114,829 92,147 80.2% 9,081 5,913 469,678 338,706 72.1%

Europe

Prologis wholly owned 207 207 12,351 12,351 100.0% 2,176 2,176 135,022 135,022 100.0%

Prologis European Properties (C) - - - - - 3,670 3,439 338,862 317,513 93.7%

Prologis European Properties Fund II 106 32 8,906 2,645 29.7% 2,043 608 150,174 44,630 29.7%

Total Europe 313 239 21,257 14,996 70.5% 7,889 6,223 624,058 497,165 79.7%

Asia

Prologis wholly owned 592 592 36,938 36,938 100.0% 592 592 36,938 36,938 100.0%

Total Asia 592 592 36,938 36,938 100.0% 592 592 36,938 36,938 100.0%

Total Third Party Building Dispositions 4,163 3,734 $173,024 $144,081 83.3% 17,562 12,728 $1,130,674 $872,809 77.2%

Building Contributions and Dispositions to Co-Investment Ventures

Americas

Prologis Mexico Fondo Logistico (C) 755 755 40,650 32,520 80.0% 755 755 40,650 32,520 80.0%

Total Americas 755 755 40,650 32,520 80.0% 755 755 40,650 32,520 80.0%

Europe

Europe Logistics Venture I - - - - - 139 139 16,875 14,343 85.0%

Total Europe - - - - - 139 139 16,875 14,343 85.0%

Asia

Total Asia - - - - - - - - - -

Total Contributions and Dispositions to Co-Investment Ventures 755 755 $40,650 $32,520 80.0% 894 894 57,525 46,863 81.5%

Total Building Dispositions and Contributions 4,918 4,489 $213,674 $176,601 82.6% 18,456 13,622 $1,188,199 $919,672 77.4%

Weighted average stabilized cap rate 7.6% 7.3%

(A) Amounts include industrial building dispositions, but do not include dispositions of non-industrial buildings or land subject to ground leases of $0.4 million for the quarter and $6.4 million year to date, of which $0.4 million and $5.1 million is Prologis’ share, respectively.

(B) Prologis share reflects actual ownership on consolidated funds. For contributions, this amount reflects cash proceeds to Prologis (net of units received for partial consideration). (C) This is a consolidated fund.

Copyright © 2012 Prologis

15

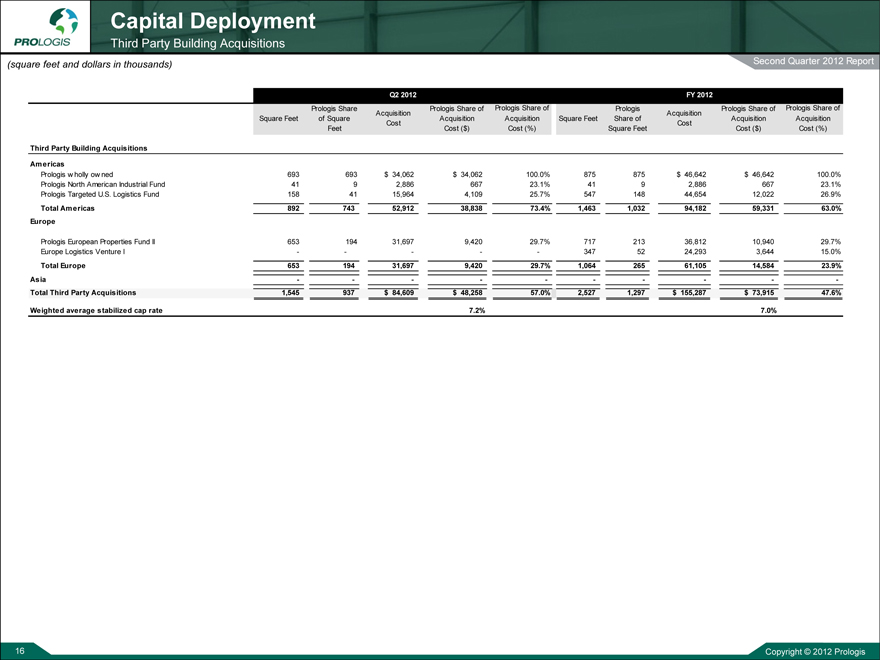

Capital Deployment

Third Party Building Acquisitions

(square feet and dollars in thousands)

Second Quarter 2012 Report

Q2 2012 FY 2012

Prologis Share Prologis Share of Prologis Share of Prologis Prologis Share of Prologis Share of

Acquisition Acquisition

Square Feet of Square Acquisition Acquisition Square Feet Share of Acquisition Acquisition

Cost Cost

Feet Cost ($) Cost (%) Square Feet Cost ($) Cost (%)

Third Party Building Acquisitions

Americas

Prologis wholly owned 693 693 $ 34,062 $ 34,062 100.0% 875 875 $ 46,642 $ 46,642 100.0%

Prologis North American Industrial Fund 41 9 2,886 667 23.1% 41 9 2,886 667 23.1%

Prologis Targeted U.S. Logistics Fund 158 41 15,964 4,109 25.7% 547 148 44,654 12,022 26.9%

Total Americas 892 743 52,912 38,838 73.4% 1,463 1,032 94,182 59,331 63.0%

Europe

Prologis European Properties Fund II 653 194 31,697 9,420 29.7% 717 213 36,812 10,940 29.7%

Europe Logistics Venture I—- ——- 347 52 24,293 3,644 15.0%

Total Europe 653 194 31,697 9,420 29.7% 1,064 265 61,105 14,584 23.9%

Asia—- ————- —-

Total Third Party Acquisitions 1,545 937 $ 84,609 $ 48,258 57.0% 2,527 1,297 $ 155,287 $ 73,915 47.6%

Weighted average stabilized cap rate 7.2% 7.0%

Copyright © 2012 Prologis

16

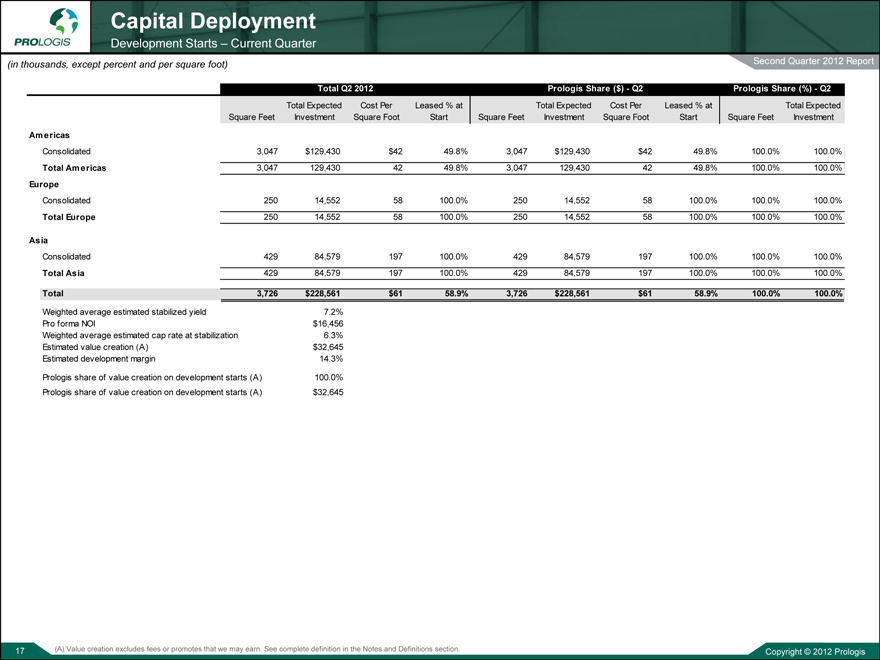

Capital Deployment

Development Starts – Current Quarter

Second Quarter 2012 Report

(in thousands, except percent and per square foot)

Total Q2 2012 Prologis Share ($)—Q2 Prologis Share (%)—Q2

Total Expected Cost Per Leased % at Total Expected Cost Per Leased % at Total Expected

Square Feet Investment Square Foot Start Square Feet Investment Square Foot Start Square Feet Investment

Americas

Consolidated 3,047 $129,430 $42 49.8% 3,047 $129,430 $42 49.8% 100.0% 100.0%

Total Americas 3,047 129,430 42 49.8% 3,047 129,430 42 49.8% 100.0% 100.0%

Europe

Consolidated 250 14,552 58 100.0% 250 14,552 58 100.0% 100.0% 100.0%

Total Europe 250 14,552 58 100.0% 250 14,552 58 100.0% 100.0% 100.0%

Asia

Consolidated 429 84,579 197 100.0% 429 84,579 197 100.0% 100.0% 100.0%

Total Asia 429 84,579 197 100.0% 429 84,579 197 100.0% 100.0% 100.0%

Total 3,726 $228,561 $61 58.9% 3,726 $228,561 $61 58.9% 100.0% 100.0%

Weighted average estimated stabilized yield 7.2%

Pro forma NOI $16,456

Weighted average estimated cap rate at stabilization 6.3%

Estimated value creation (A) $32,645

Estimated development margin 14.3%

Prologis share of value creation on development starts (A) 100.0%

Prologis share of value creation on development starts (A) $32,645

(A) Value creation excludes fees or promotes that we may earn. See complete definition in the Notes and Definitions section.

Copyright © 2012 Prologis

17

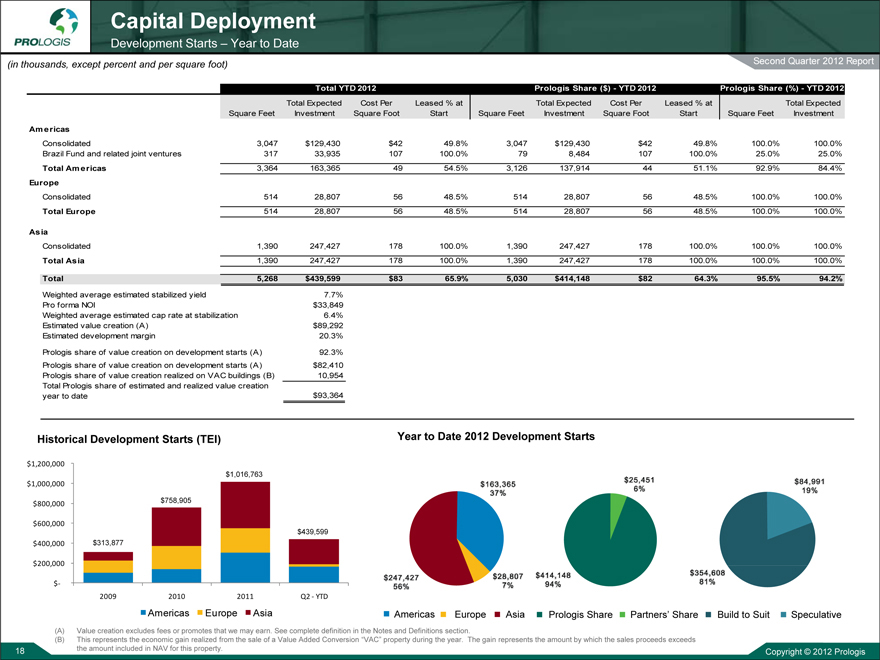

Capital Deployment

Development Starts – Year to Date

(in thousands, except percent and per square foot) Second Quarter 2012 Report

Total YTD 2012 Prologis Share ($) - YTD 2012 Prologis Share (%) - YTD 2012

Total Expected Cost Per Leased % at Total Expected Cost Per Leased % at Total Expected

Square Feet Investment Square Foot Start Square Feet Investment Square Foot Start Square Feet Investment

Americas

Consolidated 3,047 $129,430 $42 49.8% 3,047 $129,430 $42 49.8% 100.0% 100.0%

Brazil Fund and related joint ventures 317 33,935 107 100.0% 79 8,484 107 100.0% 25.0% 25.0%

Total Americas 3,364 163,365 49 54.5% 3,126 137,914 44 51.1% 92.9% 84.4%

Europe

Consolidated 514 28,807 56 48.5% 514 28,807 56 48.5% 100.0% 100.0%

Total Europe 514 28,807 56 48.5% 514 28,807 56 48.5% 100.0% 100.0%

Asia

Consolidated 1,390 247,427 178 100.0% 1,390 247,427 178 100.0% 100.0% 100.0%

Total Asia 1,390 247,427 178 100.0% 1,390 247,427 178 100.0% 100.0% 100.0%

Total 5,268 $439,599 $83 65.9% 5,030 $414,148 $82 64.3% 95.5% 94.2%

Weighted average estimated stabilized yield 7.7%

Pro forma NOI $33,849

Weighted average estimated cap rate at stabilization 6.4%

Estimated value creation (A) $89,292

Estimated development margin 20.3%

Prologis share of value creation on development starts (A) 92.3%

Prologis share of value creation on development starts (A) $82,410

Prologis share of value creation realized on VAC buildings (B) 10,954

Total Prologis share of estimated and realized value creation

year to date $93,364

Historical Development Starts (TEI) Year to Date 2012 Development Starts

$1,200,000

$1,016,763

$1,000,000

$800,000 $758,905

$600,000

$439,599

$400,000 $313,877

$200,000

$-

2009 2010 2011 Q2 - YTD

Americas Europe Asia Americas Europe Asia Prologis Share Partner’s Share Build to Suit Speculative

(A) Value creation excludes fees or promotes that we may earn. See complete definition in the Notes and Definitions section.

(B) This represents the economic gain realized from the sale of a Value Added Conversion “VAC” property during the year. The gain represents the amount by which the sales proceeds exceeds

the amount included in NAV for this property.

Copyright © 2012 Prologis

18

Capital Deployment

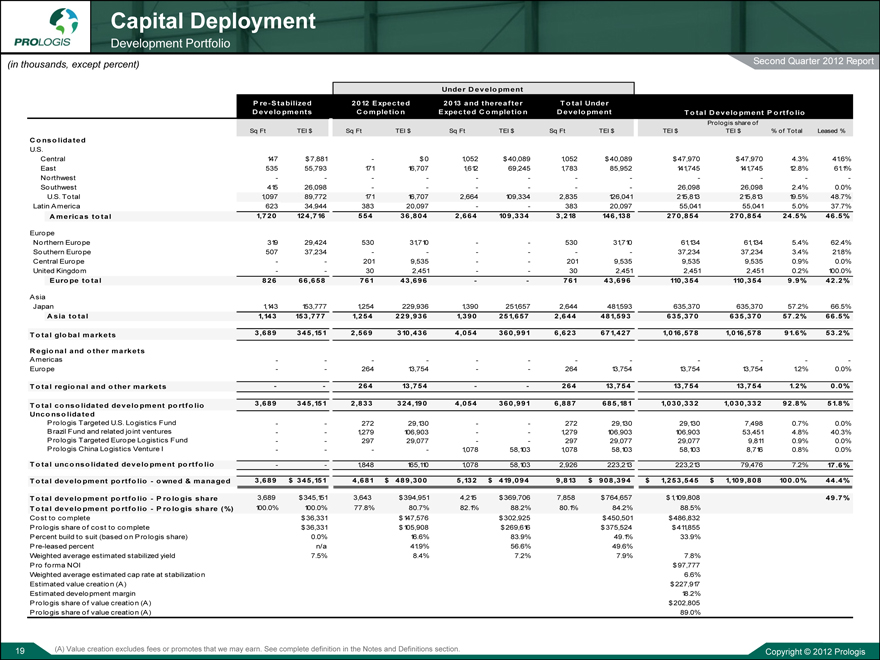

Development Portfolio

(in thousands, except percent) Second Quarter 2012 Report

Under D evelo pment

P re-Stabilized 2012 Expected 2013 and thereafter T o tal Under

D evelo pments C o mpletio n Expected C o mpletio n D evelo pment T o tal D evelo pment P o rtfo lio

Prologis share of

Sq Ft TEI $ Sq Ft TEI $ Sq Ft TEI $ Sq Ft TEI $ TEI $ TEI $ % of Total Leased %

C o nso lidated

U.S.

Central 147 $7,881 - $0 1,052 $40,089 1,052 $40,089 $47,970 $47,970 4.3% 41.6%

East 535 55,793 171 16,707 1,612 69,245 1,783 85,952 141,745 141,745 12.8% 61.1%

Northwest - - - - - - - - - - - -

Southwest 415 26,098 - - - - - - 26,098 26,098 2.4% 0.0%

U.S. Total 1,097 89,772 171 16,707 2,664 109,334 2,835 126,041 215,813 215,813 19.5% 48.7%

Latin America 623 34,944 383 20,097 - - 383 20,097 55,041 55,041 5.0% 37.7%

A mericas to tal 1,720 124,716 554 36,804 2,664 109,334 3,218 146,138 270,854 270,854 24.5% 46.5%

Europe

Northern Europe 319 29,424 530 31,710 - - 530 31,710 61,134 61,134 5.4% 62.4%

Southern Europe 507 37,234 - - - - - - 37,234 37,234 3.4% 21.8%

Central Europe - - 201 9,535 - - 201 9,535 9,535 9,535 0.9% 0.0%

United Kingdom - - 30 2,451 - - 30 2,451 2,451 2,451 0.2% 100.0%

Euro pe to tal 826 66,658 761 43,696 - - 761 43,696 110,354 110,354 9 .9% 42 .2%

Asia

Japan 1,143 153,777 1,254 229,936 1,390 251,657 2,644 481,593 635,370 635,370 57.2% 66.5%

A sia to tal 1,143 153,777 1,254 229,936 1,390 251,657 2,644 481,593 635,370 635,370 57.2% 66.5%

T o tal glo bal markets 3,689 345,151 2,569 310,436 4,054 360,991 6,623 671,427 1,016,578 1,016,578 91.6% 53.2%

R egio nal and o ther markets

Americas - - - - - - - - - - - -

Euro pe - - 264 13,754 - - 264 13,754 13,754 13,754 1.2% 0.0%

T o tal regio nal and o ther markets - - 264 13,754 - - 264 13,754 13,754 13,754 1.2% 0.0%

T o tal co nso lidated develo pment po rtfo lio 3,689 345,151 2,833 324,190 4,054 360,991 6,887 685,181 1,030,332 1,030,332 92.8% 51.8%

Unco nso lidated

Prologis Targeted U.S. Logistics Fund - - 272 29,130 - - 272 29,130 29,130 7,498 0.7% 0.0%

Brazil Fund and related joint ventures - - 1,279 106,903 - - 1,279 106,903 106,903 53,451 4.8% 40.3%

Prologis Targeted Europe Logistics Fund - - 297 29,077 - - 297 29,077 29,077 9,811 0.9% 0.0%

Prologis China Logistics Venture I - - - - 1,078 58,103 1,078 58,103 58,103 8,716 0.8% 0.0%

T o tal unco nso lidated develo pment po rtfo lio - - 1,848 165,110 1,078 58,103 2,926 223,213 223,213 79,476 7.2% 17.6%

T o tal develo pment po rtfo lio - o wned & managed 3,689 $ 345,151 4,681 $ 489,300 5,132 $ 419,094 9,813 $ 908,394 $ 1,253,545 $ 1,109,808 100.0% 44.4%

T o tal develo pment po rtfo lio - P ro lo gis share 3,689 $345,151 3,643 $394,951 4,215 $369,706 7,858 $764,657 $1,109,808 49.7%

T o tal develo pment po rtfo lio - P ro lo gis share (%) 100.0% 100.0% 77.8% 80.7% 82.1% 88.2% 80.1% 84.2% 88.5%

Cost to complete $36,331 $147,576 $302,925 $450,501 $486,832

Prologis share of cost to complete $36,331 $105,908 $269,616 $375,524 $411,855

Percent build to suit (based on Prologis share) 0.0% 16.6% 83.9% 49.1% 33.9%

Pre-leased percent n/a 41.9% 56.6% 49.6%

Weighted average estimated stabilized yield 7.5% 8.4% 7.2% 7.9% 7.8%

Pro forma NOI $97,777

Weighted average estimated cap rate at stabilization 6.6%

Estimated value creation (A) $227,917

Estimated development margin 18.2%

Prologis share of value creation (A) $202,805

Prologis share of value creation (A) 89.0%

19 (A) Value creation excludes fees or promotes that we may earn. See complete definition in the Notes and Definitions section. Copyright © 2012 Prologis

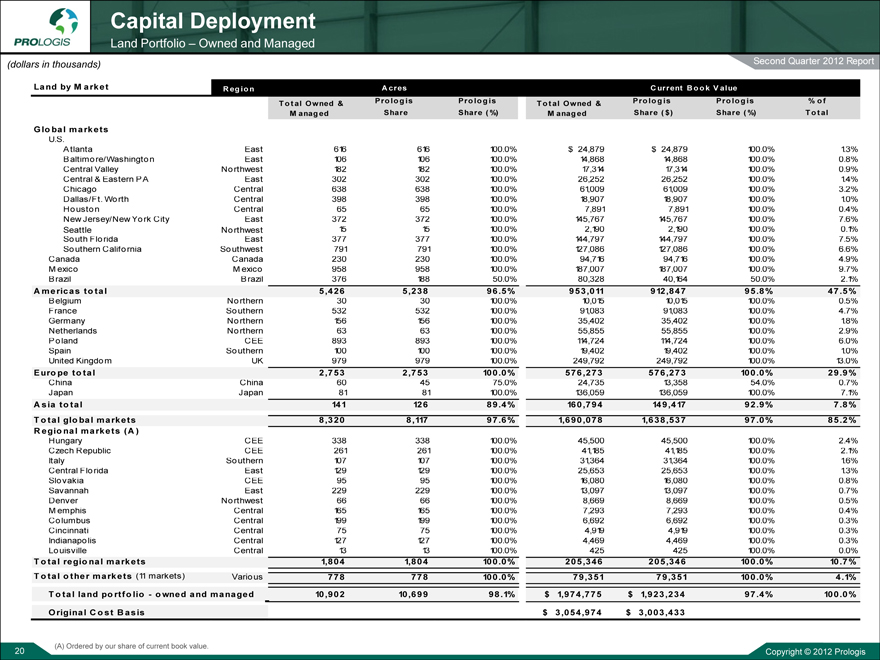

Capital Deployment

Land Portfolio – Owned and Managed

(dollars in thousands) Second Quarter 2012 Report

Land by M arket R egion A cres C urrent B o ok V alue

T ot al Owned & Prolo gis Prologis T ot al Owned & Prolo gis Prologis % of

M anaged Share Share ( %) M anaged Share ( $) Share ( %) T ot al

Glo bal markets

U.S.

Atlanta East 616 616 100.0% $ 24,879 $ 24,879 100.0% 1.3%

Baltimore/Washington East 106 106 100.0% 14,868 14,868 100.0% 0.8%

Central Valley Northwest 182 182 100.0% 17,314 17,314 100.0% 0.9%

Central & Eastern PA East 302 302 100.0% 26,252 26,252 100.0% 1.4%

Chicago Central 638 638 100.0% 6100961,009 6100961,009 100.0% 3.2%

Dallas/Ft. Worth Central 398 398 100.0% 18,907 18,907 100.0% 1.0%

Houston Central 65 65 100.0% 7,891 7,891 100.0% 0.4%

New Jersey/New York City East 372 372 100.0% 145,767 145,767 100.0% 7.6%

Seattle Northwest 15 15 100.0% 2,190 2,190 100.0% 0.1%

South Florida East 377 377 100.0% 144,797 144,797 100.0% 7.5%

Southern California Southwest 791 791 100.0% 127,086 127,086 100.0% 6.6%

Canada Canada 230 230 100.0% 94,716 94,716 100.0% 4.9%

M exico M exico 958 958 100.0% 187,007 187,007 100.0% 9.7%

Brazil Brazil 376 188 50.0% 80,328, 40,164, 50.0% 2.1%

A mericas to tal 5,426 5,238 96.5% 953,011 912,847 95.8% 47.5%

Belgium Northern 30 30 100.0% 10,015 10,015 100.0% 0.5%

France Southern 532 532 100.0% 91,083 91,083 100.0% 4.7%

Germany Northern 156 156 100.0% 35,402 35,402 100.0% 1.8%

Netherlands Northern 63 63 100.0% 55,855 55,855 100.0% 2.9%

Poland CEE 893 893 100.0% 114,724 114,724 100.0% 6.0%

Spain Southern 100 100 100.0% 19,402 19,402 100.0% 1.0%

United Kingdom UK 979 979 100.0% 249,792 249,792 100.0% 13.0%

Euro pe to tal 2,753 2,753 100.0% 576,273 576,273 100.0% 29.9%

China China 60 45 75.0% 24,735 13,358 54.0% 0.7%

Japan Japan 81 81 100.0% 136,059 136,059 100.0% 7.1%

A sia to tal 141 126 89.4% 160,794 149,417 92.9% 7.8%

T o tal glo bal markets 8,320 8,117 97.6% 1,690,078 1,638,537 97.0% 85.2%

R egio nal markets (A )

Hungary CEE 338 338 100.0% 45,500 45,500 100.0% 2.4%

Czech Republic CEE 261 261 100.0% 41,185 41,185 100.0% 2.1%

Italy Southern 107 107 100.0% 31,364 31,364 100.0% 1.6%

Central Florida East 129 129 100.0% 25,653 25,653 100.0% 13%1.3%

Slovakia CEE 95 95 100.0% 16,080 16,080 100.0% 0.8%

Savannah East 229 229 100.0% 13,097 13,097 100.0% 0.7%

Denver Northwest 66 66 100.0% 8,669 8,669 100.0% 0.5%

M emphis Central 165 165 100.0% 7,293 7,293 100.0% 0.4%

Columbus Central 199 199 100.0% 6,692 6,692 100.0% 0.3%

Cincinnati Central 75 75 100.0% 4,919 4,919 100.0% 0.3%

Indianapolis Central 127 127 100.0% 4,469 4,469 100.0% 0.3%

Louisville Central 13 13 100.0% 425 425 100.0% 0.0%

T o tal re gio nal markets 1,804 1,804 100.0% 205 ,346 205 ,346 100.0% 10.7%

T o tal o ther markets (11 markets) Various 778 778 100.0% 79,351 79,351 100.0% 4.1%

T o tal land po rtfo lio - o wned and managed 10,902 10,699 98.1% $ 1,974,775 $ 1,923,234 97.4% 100.0%

Original C o st B asis $ 3,054,974 $ 3,003,433

(A) Ordered by our share of current book value.

20 Copyright © 2012 Prologis

Capital Deployment

Land Portfolio – Summary and Roll Forward

Second Quarter 2012 Report

(dollars in thousands)

Investment at

Land Portfolio Summary Acres % of Total June 30, 2012 % of Total

Americas

Prologis wholly owned 6,712 61.6% $ 997,471 50.5%

Brazil Fund and related joint ventures 376 3.4% 80,328 4.1%

Total Americas 7,088 65.0% 1,077,799 54.6%

Europe

Prologis wholly owned 3,673 33.7% 736,182 37.3%

Asia

Prologis wholly owned 123 1.1% 147,409 7.5%

Prologis China Logistics Venture 1 18 0.2% 13,385 0.6%

Total Asia 141 1.3% 160,794 8.1%

Total land portfolio—owned and managed 10,902 100.0% $ 1,974,775 100.0%

Land Roll Forward—Owned and Managed Americas Europe Asia Total

As of March 31, 2012 $ 1,056,183 $ 740,840 $ 196,454 $ 1,993,477

Acquisitions 43,929 24,475 — 68,404

Dispositions (A) (3,444) (10,231) — (13,675)

Development starts (18,064) (2,104) (31,976) (52,144)

Infrastructure costs 22,087 1,967 2,683 26,737

Reclasses 7,548 —— 7,548

Effect of changes in foreign exchange rates and other (30,440) (18,765) (6,367) (55,572)

As of June 30, 2012 $ 1,077,799 $ 736,182 $ 160,794 $ 1,974,775

(A) Includes 58 acres that were sold for $14.2 million in proceeds.

Copyright © 2012 Prologis

21

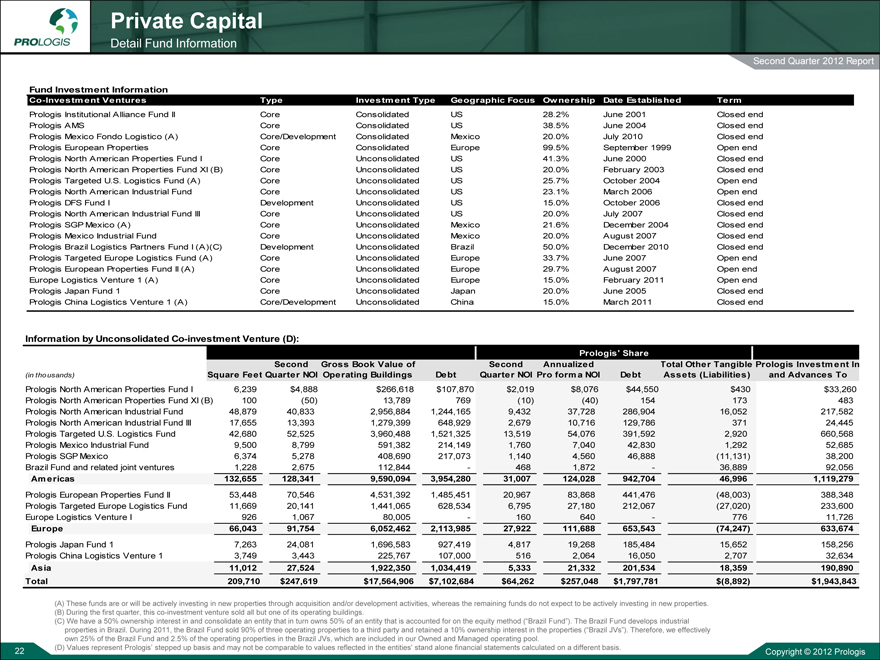

Private Capital

Detail Fund Information

Second Quarter 2012 Report

Fund Investment Information

Co-Investment Ventures Type Investment Type Geographic Focus Ownership Date Established Term

Prologis Institutional Alliance Fund II Core Consolidated US 28.2% June 2001 Closed end

Prologis AMS Core Consolidated US 38.5% June 2004 Closed end

Prologis Mexico Fondo Logistico (A) Core/Development Consolidated Mexico 20.0% July 2010 Closed end

Prologis European Properties Core Consolidated Europe 99.5% September 1999 Open end

Prologis North American Properties Fund I Core Unconsolidated US 41.3% June 2000 Closed end

Prologis North American Properties Fund XI (B) Core Unconsolidated US 20.0% February 2003 Closed end

Prologis Targeted U.S. Logistics Fund (A) Core Unconsolidated US 25.7% October 2004 Open end

Prologis North American Industrial Fund Core Unconsolidated US 23.1% March 2006 Open end

Prologis DFS Fund I Development Unconsolidated US 15.0% October 2006 Closed end

Prologis North American Industrial Fund III Core Unconsolidated US 20.0% July 2007 Closed end

Prologis SGP Mexico (A) Core Unconsolidated Mexico 21.6% December 2004 Closed end

Prologis Mexico Industrial Fund Core Unconsolidated Mexico 20.0% August 2007 Closed end

Prologis Brazil Logistics Partners Fund I (A)(C) Development Unconsolidated Brazil 50.0% December 2010 Closed end

Prologis Targeted Europe Logistics Fund (A) Core Unconsolidated Europe 33.7% June 2007 Open end

Prologis European Properties Fund II (A) Core Unconsolidated Europe 29.7% August 2007 Open end

Europe Logistics Venture 1 (A) Core Unconsolidated Europe 15.0% February 2011 Open end

Prologis Japan Fund 1 Core Unconsolidated Japan 20.0% June 2005 Closed end

Prologis China Logistics Venture 1 (A) Core/Development Unconsolidated China 15.0% March 2011 Closed end

Information by Unconsolidated Co-investment Venture (D):

Prologis’ Share

Second Gross Book Value of Second Annualized Total Other Tangible Prologis Investment In

(in thousands) Square Feet Quarter NOI Operating Buildings Debt Quarter NOI Pro forma NOI Debt Assets (Liabilities) and Advances To

Prologis North American Properties Fund I 6,239 $4,888 $266,618 $107,870 $2,019 $8,076 $44,550 $430 $33,260

Prologis North American Properties Fund XI (B) 100 (50) 13,789 769 (10) (40) 154 173 483

Prologis North American Industrial Fund 48,879 40,833 2,956,884 1,244,165 9,432 37,728 286,904 16,052 217,582

Prologis North American Industrial Fund III 17,655 13,393 1,279,399 648,929 2,679 10,716 129,786 371 24,445

Prologis Targeted U.S. Logistics Fund 42,680 52,525 3,960,488 1,521,325 13,519 54,076 391,592 2,920 660,568

Prologis Mexico Industrial Fund 9,500 8,799 591,382 214,149 1,760 7,040 42,830 1,292 52,685

Prologis SGP Mexico 6,374 5,278 408,690 217,073 1,140 4,560 46,888 (11,131) 38,200

Brazil Fund and related joint ventures 1,228 2,675 112,844—468 1,872 —36,889 92,056

Americas 132,655 128,341 9,590,094 3,954,280 31,007 124,028 942,704 46,996 1,119,279

Prologis European Properties Fund II 53,448 70,546 4,531,392 1,485,451 20,967 83,868 441,476 (48,003) 388,348

Prologis Targeted Europe Logistics Fund 11,669 20,141 1,441,065 628,534 6,795 27,180 212,067 (27,020) 233,600

Europe Logistics Venture I 926 1,067 80,005—160 640 —776 11,726

Europe 66,043 91,754 6,052,462 2,113,985 27,922 111,688 653,543 (74,247) 633,674

Prologis Japan Fund 1 7,263 24,081 1,696,583 927,419 4,817 19,268 185,484 15,652 158,256

Prologis China Logistics Venture 1 3,749 3,443 225,767 107,000 516 2,064 16,050 2,707 32,634

Asia 11,012 27,524 1,922,350 1,034,419 5,333 21,332 201,534 18,359 190,890

Total 209,710 $247,619 $17,564,906 $7,102,684 $64,262 $257,048 $1,797,781 $(8,892) $1,943,843

(A) These funds are or will be actively investing in new properties through acquisition and/or development activities, whereas the remaining funds do not expect to be actively investing in new properties. (B) During the first quarter, this co-investment venture sold all but one of its operating buildings.

(C) We have a 50% ownership interest in and consolidate an entity that in turn owns 50% of an entity that is accounted for on the equity method (“Brazil Fund”). The Brazil Fund develops industrial properties in Brazil. During 2011, the Brazil Fund sold 90% of three operating properties to a third party and retained a 10% ownership interest in the properties (“Brazil JVs”). Therefore, we effectively own 25% of the Brazil Fund and 2.5% of the operating properties in the Brazil JVs, which are included in our Owned and Managed operating pool.

(D) Values represent Prologis’ stepped up basis and may not be comparable to values reflected in the entities’ stand alone financial statements calculated on a different basis.

Copyright © 2012 Prologis

22

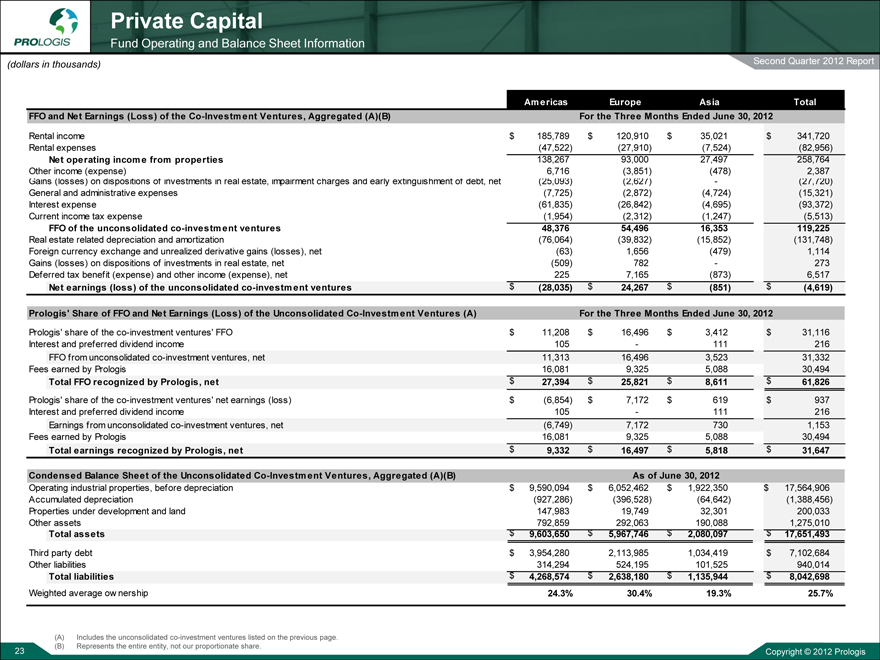

Private Capital

Fund Operating and Balance Sheet Information

(dollars in thousands) Second Quarter 2012 Report

Americas Europe Asia Total

FFO and Net Earnings (Loss) of the Co-Investment Ventures, Aggregated (A)(B) For the Three Months Ended June 30, 2012

Rental income $ 185,789 $ 120,910 $ 35,021 $ 341,720

Rental expenses (47,522) (27,910) (7,524) (82,956)

Net operating income from properties 138,267 93,000 27,497 258,764

Other income (expense) 6,716 (3,851) (478) 2,387

Gains (losses) on dispositions of investments in real estate, impairment charges and early extinguishment of debt, net (25,093) (2,627) - (27,720)

General and administrative expenses (7,725) (2,872) (4,724) (15,321)

Interest expense (61,835) (26,842) (4,695) (93,372)

Current income tax expense (1,954) (2,312) (1,247) (5,513)

FFO of the unconsolidated co-investment ventures 48,376 54,496 16,353 119,225

Real estate related depreciation and amortization (76,064) (39,832) (15,852) (131,748)

Foreign currency exchange and unrealized derivative gains (losses), net (63) 1,656 (479) 1,114

Gains (losses) on dispositions of investments in real estate, net (509) 782 - 273

Deferred tax benefit (expense) and other income (expense), net 225 7,165 (873) 6,517

Net earnings (loss) of the unconsolidated co-investment ventures $ (28,035) $ 24,267 $ (851) $ (4,619)

Prologis’ Share of FFO and Net Earnings (Loss) of the Unconsolidated Co-Investment Ventures (A) For the Three Months Ended June 30, 2012

Prologis’ share of the co-investment ventures’ FFO $ 11,208 $ 16,496 $ 3,412 $ 31,116

Interest and preferred dividend income 105 - 111 216

FFO from unconsolidated co-investment ventures, net 11,313 16,496 3,523 31,332

Fees earned by Prologis 16,081 9,325 5,088 30,494

Total FFO recognized by Prologis, net $ 27,394 $ 25,821 $ 8,611 $ 61,826

Prologis’ share of the co-investment ventures’ net earnings (loss) $ (6,854) $ 7,172 $ 619 $ 937

Interest and preferred dividend income 105 - 111 216

Earnings from unconsolidated co-investment ventures, net (6,749) 7,172 730 1,153

Fees earned by Prologis 16,081 9,325 5,088 30,494

Total earnings recognized by Prologis, net $ 9,332 $ 16,497 $ 5,818 $ 31,647

Condensed Balance Sheet of the Unconsolidated Co-Investment Ventures, Aggregated (A)(B) As of June 30, 2012

Operating industrial properties, before depreciation $ 9,590,094 $ 6,052,462 $ 1,922,350 $ 17,564,906

Accumulated depreciation (927,286) (396,528) (64,642) (1,388,456)

Properties under development and land 147,983 19,749 32,301 200,033

Other assets 792,859 292,063 190,088 1,275,010

Total assets $ 9,603,650 $ 5,967,746 $ 2,080,097 $ 17,651,493

Third party debt $ 3,954,280 2,113,985 1,034,419 $ 7,102,684

Other liabilities 314,294 524,195 101,525 940,014

Total liabilities $ 4,268,574 $ 2,638,180 $ 1,135,944 $ 8,042,698

Weighted average ow nership 24.3% 30.4% 19.3% 25.7%

(A) Includes the unconsolidated co-investment ventures listed on the previous page.

(B) Represents the entire entity, not our proportionate share.

23 Copyright © 2012 Prologis

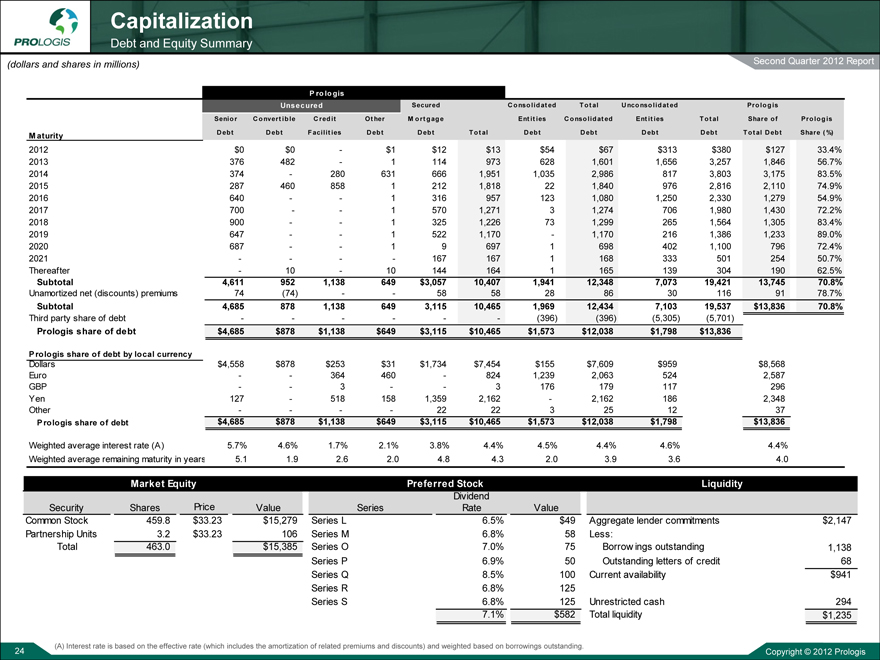

Capitalization

Debt and Equity Summary

(dollars and shares in millions) Second Quarter 2012 Report

P ro lo gis

Unsecured Secured C onsolidat ed Tot al U nconsolidat ed Prologis

Senior C onvert ible C redit Ot her M ort gage Ent it ies C onsolidat ed Ent it ies Tot al Share of Pro lo g is

M aturity D ebt D ebt Facilit ies D ebt D ebt Tot al D ebt D ebt D ebt D ebt Tot al D ebt Share ( %)

2012 $0 $0 - $1 $12 $13 $54 $67 $313 $380 $127 33.4%

2013 376 482 - 1 114 973 628 1,601 1,656 3,257 1,846 56.7%

2014 374 - 280 631 666 1,951 1,035 2,986 817 3,803 3,175 83.5%

2015 287 460 858 1 212 1,818 22 1,840 976 2,816 2,110 74.9%

2016 640 - - 1 316 957 123 1,080 1,250 2,330 1,279 54.9%

2017 700 - - 1 570 1,271 3 1,274 706 1,980 1,430 72.2%

2018 900 - - 1 325 1,226 73 1,299 265 1,564 1,305 83.4%

2019 647 - - 1 522 1,170 - 1,170 216 1,386 1,233 89.0%

2020 687 - - 1 9 697 1 698 402 1,100 796 72.4%

2021 - - - - 167 167 1 168 333 501 254 50.7%

Thereafter - 10 - 10 144 164 1 165 139 304 190 62.5%

Subtotal 4,611 952 1,138 649 $3,057 10,407 1,941 12,348 7,073 19,421 13,745 70.8%

Unamortized net (discounts) premiums 74 (74) - - 58 58 28 86 30 116 91 78.7%

Subtotal 4,685 878 1,138 649 3,115 10,465 1,969 12,434 7,103 19,537 $13,836 70.8%

Third party share of debt - - - - - - (396) (396) (5,305) (5,701)

Prologis share of debt $4,685 $878 $1,138 $649 $3,115 $10,465 $1,573 $12,038 $1,798 $13,836

Prologis share of debt by local currency

Dollars $4,558 $878 $253 $31 $1,734 $7,454 $155 $7,609 $959 $ 9,395 $8,568

Euro - - 364 460 - 824 1,239 2,063 524 2,887 2,587

GBP - - 3 - - 3 176 179 117 533 296

Yen 127 - 518 158 1,359 2,162 - 2,162 186 1,617 2,348

Other - - - - 22 22 3 25 12 35 37

Prologis share of debt $4,685 $878 $1,138 $649 $3,115 $10,465 $1,573 $12,038 $1,798 $13,836

Weighted average interest rate (A) 5.7% 4.6% 1.7% 2.1% 3.8% 4.4% 4.5% 4.4% 4.6% 5.0% 4.4%

Weighted average remaining maturity in years 5.1 1.9 2.6 2.0 4.8 4.3 2.0 3.9 3.6 4.1 4.0

Market Equity Preferred Stock Liquidity

Dividend

Security Shares Price Value Series Rate Value

Common Stock 459.8 $33.23 $15,279 Series L 6.5% $49 Aggregate lender commitments $2,147

Partnership Units 3.2 $33.23 106 Series M 6.8% 58 Less:

Total 463.0 $15,385 Series O 7.0% 75 Borrow ings outstanding 1,138

Series P 6.9% 50 Outstanding letters of credit 68

Series Q 8.5% 100 Current availability $941

Series R 6.8% 125

Series S 6.8% 125 Unrestricted cash 294

7.1% $582 Total liquidity $1,235

(A) Interest rate is based on the effective rate (which includes the amortization of related premiums and discounts) and weighted based on borrowings outstanding.

24 Copyright © 2012 Prologis

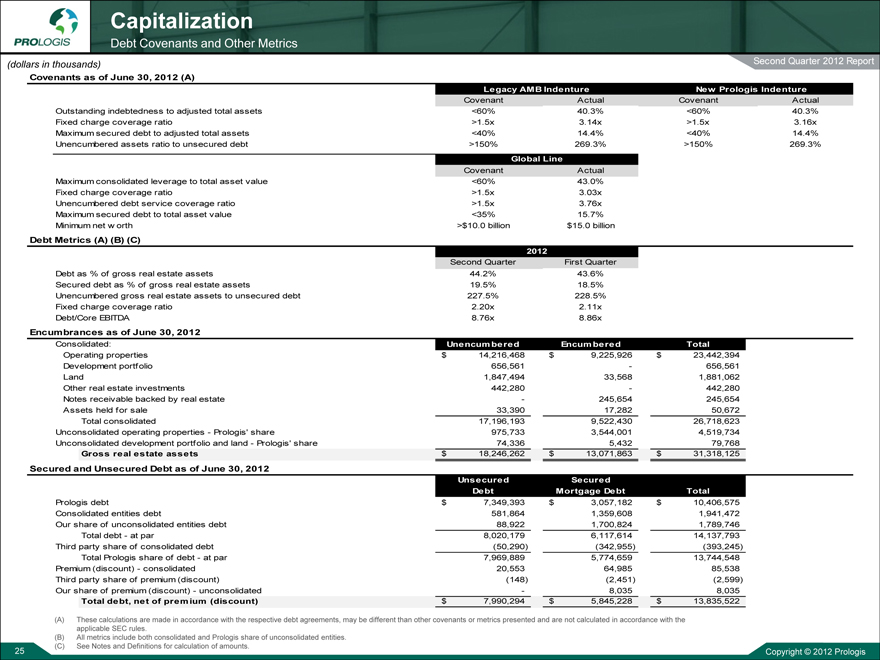

Capitalization

Debt Covenants and Other Metrics

(dollars in thousands) Second Quarter 2012 Report

Covenants as of June 30, 2012 (A)

Legacy AMB Indenture New Prologis Indenture

Covenant Actual Covenant Actual

Outstanding indebtedness to adjusted total assets <60% 40.3% <60% 40.3%

Fixed charge coverage ratio >1.5x 3.14x >1.5x 3.16x

Maximum secured debt to adjusted total assets <40% 14.4% <40% 14.4%

Unencumbered assets ratio to unsecured debt >150% 269.3% >150% 269.3%

Global Line

Covenant Actual

Maximum consolidated leverage to total asset value <60% 43.0%

Fixed charge coverage ratio >1.5x 3.03x

Unencumbered debt service coverage ratio >1.5x 3.76x

Maximum secured debt to total asset value <35% 15.7%

Minimum net w orth >$10.0 billion $15.0 billion

Debt Metrics (A) (B) (C)

2012

Second Quarter First Quarter

Debt as % of gross real estate assets 44.2% 43.6%

Secured debt as % of gross real estate assets 19.5% 18.5%

Unencumbered gross real estate assets to unsecured debt 227.5% 228.5%

Fixed charge coverage ratio 2.20x 2.11x

Debt/Core EBITDA 8.76x 8.86x

Encumbrances as of June 30, 2012

Consolidated: Unencumbered Encumbered Total

Operating properties $ 14,216,468 $ 9,225,926 $ 23,442,394

Development portfolio 656,561 - 656,561

Land 1,847,494 33,568 1,881,062

Other real estate investments 442,280 - 442,280

Notes receivable backed by real estate - 245,654 245,654

Assets held for sale 33,390 17,282 50,672

Total consolidated 17,196,193 9,522,430 26,718,623

Unconsolidated operating properties - Prologis’ share 975,733 3,544,001 4,519,734

Unconsolidated development portfolio and land - Prologis’ share 74,336 5,432 79,768

Gross real estate assets $ 18,246,262 $ 13,071,863 $ 31,318,125

Secured and Unsecured Debt as of June 30, 2012

Unsecured Secured

Debt Mortgage Debt Total

Prologis debt $ 7,349,393 $ 3,057,182 $ 10,406,575

Consolidated entities debt 581,864 1,359,608 1,941,472

Our share of unconsolidated entities debt 88,922 1,700,824 1,789,746

Total debt - at par 8,020,179 6,117,614 14,137,793

Third party share of consolidated debt (50,290) (342,955) (393,245)

Total Prologis share of debt - at par 7,969,889 5,774,659 13,744,548

Premium (discount) - consolidated 20,553 64,985 85,538

Third party share of premium (discount) (148) (2,451) (2,599)

Our share of premium (discount) - unconsolidated - 8,035 8,035

Total debt, net of premium (discount) $ 7,990,294 $ 5,845,228 $ 13,835,522

(A) These calculations are made in accordance with the respective debt agreements, may be different than other covenants or metrics presented and are not calculated in accordance with the

applicable SEC rules.

(B) All metrics include both consolidated and Prologis share of unconsolidated entities.

(C) See Notes and Definitions for calculation of amounts.

25 Copyright © 2012 Prologis

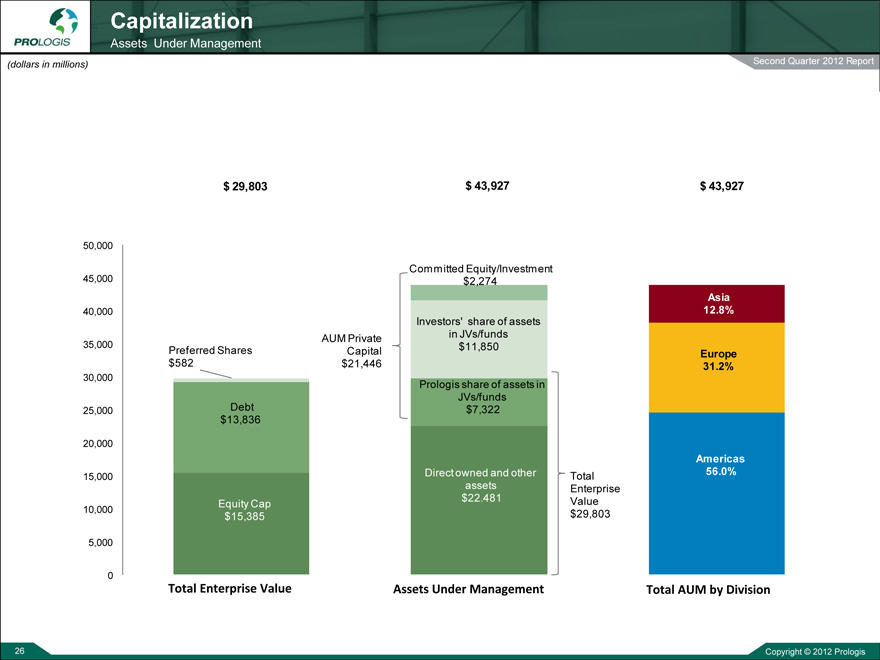

Capitalization

Assets Under Management

Second Quarter 2012 Report

(dollars in millions)

$ 29,803 $ 43,927 $ 43,927

50,000

Committed Equity/Investment

45,000 $2,274

Asia

40,000 12.8%

Investors’ share of assets

AUM Private in JVs/funds

35,000 Preferred Shares Capital $11,850 Europe

$582 $21,446 31.2%

30,000 Prologis share of assets in

JVs/funds

25,000 Debt $7,322

$13,836

20,000

Americas

15,000 Direct owned and other Total 56.0%

assets Enterprise

Equity Cap $22.481 Value

10,000 $15,385 $29,803

5,000

0

Total Enterprise Value Assets Under Management Total AUM by Division

Copyright © 2012 Prologis

26

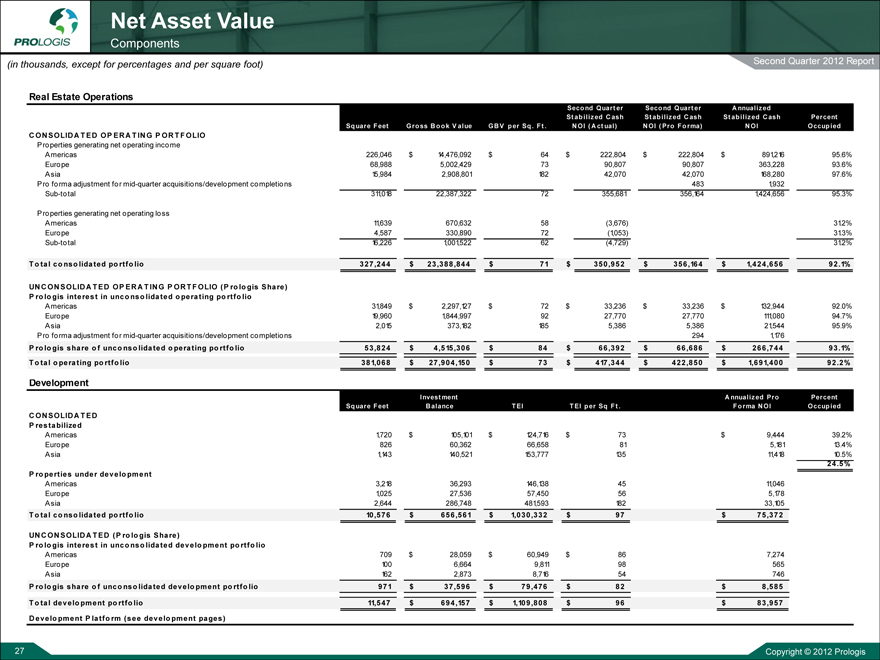

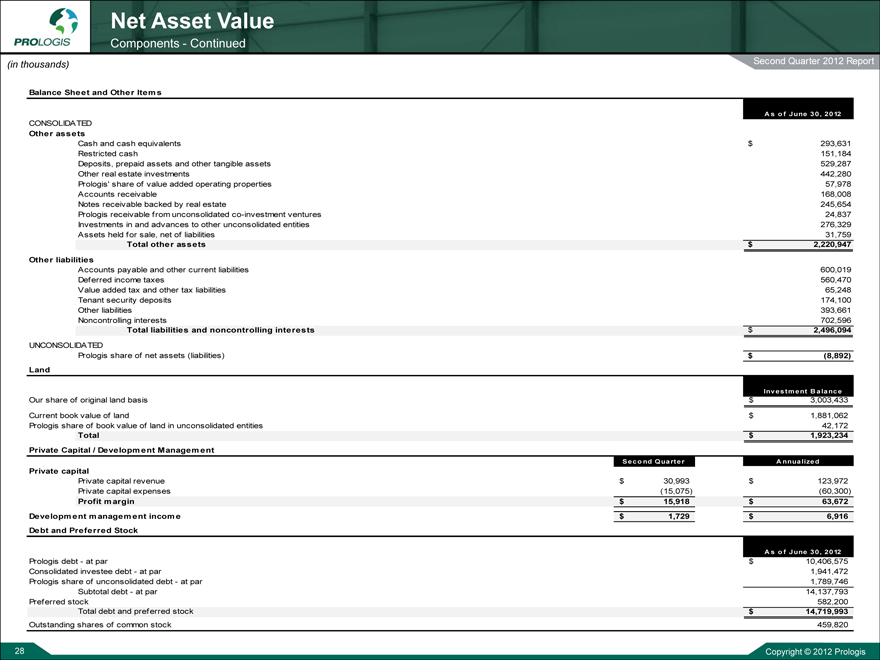

Net Asset Value

Components

(in thousands, except for percentages and per square foot) Second Quarter 2012 Report

Real Estate Operations

Seco nd Quart er Seco nd Quart er A nnualized

St ab ilized C ash St ab ilized C ash St abilized C ash Percent

Sq uare Feet Gro ss B o o k V alue GB V p er Sq . Ft . N OI ( A ct ual) N OI ( Pro Fo rma) N OI Occup ied

C ON SOLID A T ED OP ER A T IN G P OR T F OLIO

Properties generating net operating income

Americas 226,046 $ 14,476,092 $ 64 $ 222,804 $ 222,804 $ 891,216 95.6%

Europe 68,988 5,002,429 73 90,807 90,807 363,228 93.6%

Asia 15,984 2,908,801 182 42,070 42,070 168,280 97.6%

Pro forma adjustment for mid-quarter acquisitions/development completions 483 1,932

Sub-total 311,018 22,387,322 72 355,681 356,164 1,424,656 95.3%

Properties generating net operating loss

Americas 11,639 670,632 58 (3,676) 31.2%

Europe 4,587 330,890 72 (1,053) 31.3%

Sub-total 16,226 1,001,522 62 (4,729) 31.2%

T o tal co nso lidated po rtfo lio 327,244 $ 23,388,844 $ 71 $ 350,952 $ 356,164 $ 1,424,656 92.1%

UN C ON SOLID A T ED OP ER A T IN G P OR T F OLIO (P ro lo gis Share)

P ro lo gis interest in unco nso lidated o perating po rtfo lio

Americas 31,849 $ 2,297,127 $ 72 $ 33,236 $ 33,236 $ 132,944 92.0%

Europe 19,960 1,844,997 92 27,770 27,770 111,080 94.7%

Asia 2,015 373,182 185 5,386 5,386 21,544 95.9%

Pro forma adjustment for mid-quarter acquisitions/development completions 294 1,176

P ro lo gis share o f unco nso lidated o perating po rtfo lio 53,824 $ 4,515,306 $ 84 $ 66,392 $ 66,686 $ 266,744 93.1%

T o tal o perating po rtfo lio 381,068 $ 27,904,150 $ 73 $ 417,344 $ 422,850 $ 1,691,400 92.2%

Development

Invest ment A nnualized Pro Percent

Sq uare Feet B alance TEI T EI p er Sq F t . Fo rma N OI Occup ied

C ON SOLID A T ED

P restabilized

Americas 1,720 $ 105,101 $ 124,716 $ 73 $ 9,444 39.2%

Europe 826 60,362 66,658 81 5,181 13.4%

Asia 1,143 140,521 153,777 135 11,418 10.5%

24 .5%

P ro perties under develo pment

Americas 3,218 36,293 146,138 45 11,046

Europe 1,025 27,536 57,450 56 5,178

Asia 2,644 286,748 481,593 182 33,105